|

|

Welcome back to In The Room.

|

|

Tonight, David Zaslav’s tortured restructuring effort has turned Hollywood, Wall Street and the press against him—as evidenced most recently by the Times Magazine’s triple-bylined opus. Is there still a grand strategy at play? Plus, more Condé questions.

|

|

|

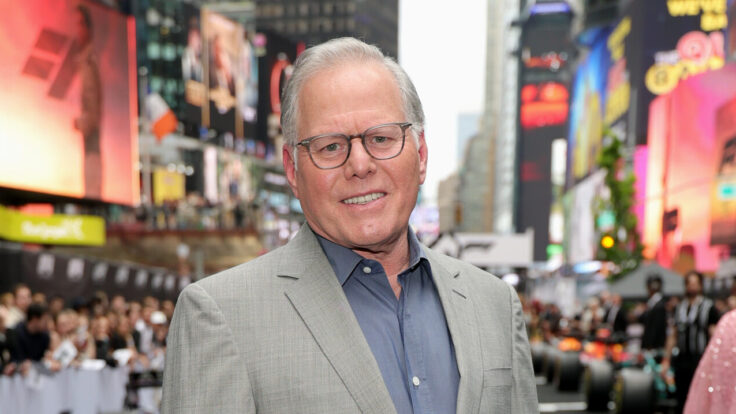

| Chief executives like to philosophize—it’s one of the ways that the art of corporate governance, strategic investment, and financial sponge-wringing ascends to a higher art form. David Zaslav, for instance, occasionally likens his leadership of Warner Bros. Discovery to the painting of an enormous fresco. In private conversations with friends, he uses this analogy to emphasize the massive time and effort required to combine two disparate legacy media assets, restructure the business, and generate cash flow, and also to dismiss what he sees as the myopia of his critics. In Zaz’s telling, his detractors in Hollywood, the press, and on Wall Street are too worried about the inevitable plaster falling on the floor—layoffs, Batgirl, the TCM cuts, etcetera—to recognize the efficient, cash-flow-positive economic masterpiece (in support of Barbie and White Lotus, among others) that he is creating above them.

A year and a half in, of course, the critics are now starting to wonder how well this so-called turnaround artist knows how to paint. WBD remains saddled with a colossal $43 billion net debt load, its stock is down nearly 57 percent since the merger, and, fairly or unfairly, Zaslav has become a convenient caricature for the various pitfalls of legacy media businesses. The New York Times Magazine’s new, triple-bylined opus on Zaslav, which arrived on Wednesday, portrays Zaz as a ruthless cost-cutter and “out-of-touch and overpaid corporate C.E.O.” who fundamentally misjudged the demands and sensitivities of modern Hollywood. In short, there’s a lot of plaster.

Undeniably, Zaslav has exhausted his goodwill with many in Hollywood, save for a close circle of well-heeled media veterans quoted in the Times piece, and even they—Barry Diller, Ken Lerer, etcetera—seem to recognize the scale of his public relations predicament. And of course, there is no one Zaz has alienated more than his shareholders. Last week’s earnings report, which sent WBD stock plummeting by 19 percent, showcased the utter lack of faith everyone seems to have in Zaz’s ability to turn economic efficiency into shareholder value. Or, put another way, Zaz has demonstrated proficiency and discipline with P&L maintenance, but he has yet to boost the EBITDA.

Some fraction of the ill will is undoubtedly due to matters of style. Zaslav is a Jack Welch understudy masquerading as a modern-day Jack Warner, and the quixotic attempt to hide his true, vest-clad, cable cowboy self under the trappings of Hollywood moguldom was never going to pass the sniff test—especially not while he was laying off thousands and cutting creative projects for tax breaks. And he obviously made a lot of unforced errors along the way, from buying Robert Evans’ house and gifting employees vests amid the layoffs, to co-hosting a lavish party at Hôtel du Cap while Hollywood’s screenwriters were on the picket lines. (The Times insightfully notes that, set against the backdrop of the strikes, “the party was more redolent of the Ancien Régime than of golden-age Hollywood.”)

In any event, it’s also true that critics of Zaslav’s ruthless cost-cutting effort miss a larger point (and one, too, that the Times Magazine editors, with their Wesleyan pedigrees, also seemed to miss). Hollywood businesses were in desperate need of restructuring when he took over, tolerating excesses (onerous first-look deals, inefficient financial decision-making, etcetera) they could no longer afford. And they were certainly ill-equipped, or even in denial, about how drastically the industry was going to change—and shrink—in the era of TikTok, Amazon, and rising interest rates. Zaz came in and called bullshit on the way business was done, made brutally unpopular decisions, and oriented the business around healthy cash flow and not “relationships.” (Speaking of which, the Times on Wednesday also published a rather amusing sidebar about Zaz’s “shattered friendships” with fired CNN executives and talent that reads like a Licht-ian revenge fantasy.)

In retrospect, it was inevitable that Hollywood would come to loathe someone whose core competency was economic efficiency, appeasing Wall Street, and running a studio and series of networks from Park Avenue South. But the industry’s mistake was to expect a savior in the first place. Zaslav’s love of old Hollywood may be genuine, but it’s not nearly as strong as his Welchian, up-or-out devotion to the fresco of the balance sheet. |

|

|

| The question for shareholders, of course, is whether Zaz is still working on a masterpiece up there, and how long the scaffolding will hold. My partner Bill Cohan is among the most bullish on Zaz’s prospects. As he noted a few days ago, WBD has been debt-saddled, overleveraged, and plagued by the broader challenge of the linear-to-streaming pivot since its very inception. “The good news,” Bill writes, is that “Zaz & Co. are paying down that debt”—$12 billion so far—and generating “over $5 billion in free cash flow.” I will concede I’m not quite as optimistic, and understand the sentiment of now-former WBD shareholders (increasingly vocal in my inbox) who refuse to accept the depreciation of their shares as the prerequisite to some grandmaster plan.

Whatever the case, the plan, such as it is, will inevitably involve further consolidation. On the most recent earnings call, Zaz said WBD was trying to position itself as an acquirer rather than a distressed asset, and as I reported last month, he may have Shari Redstone’s Paramount Global in his sights. (People around him have been quietly murmuring this for some time as the company—a frankenconglomerate that remains one limb short—examines its optionality.)

After that, the dream of a combined WBD-NBCU could still come to fruition. Alternatively, he could offload WBD to another buyer (Diller posits Saudi Arabia—no joke). In any event, Zaz is 63, already sniffing billionaire status, and addicted to economic alchemy. On some level, WBD is a financial play that simply hasn’t worked out yet. He came to Hollywood to make money, not friends. Let’s see if it works. |

| A Very Condé Nast Thanksgiving |

|

| Earlier this week, for the second time this month, members of the Condé Nast union went to C.E.O. Roger Lynch’s office to again demand that the company reach an agreement with the collective bargaining entity before implementing the recently announced layoffs that will eliminate 270 positions, or 5 percent of the workforce. Some chanted “Roger Grinch” and bore a sign displaying the moniker.

The first time around, they’d found his office empty, as my colleague Lauren Sherman reported last week. Alas, this time around Lynch was similarly absent, in Los Angeles for GQ’s annual Men of the Year event, after which I’m told he’s off to China. (Such are the perks of being a global company.)

Needless to say, this is an uncomfortable conversation for Lynch. As I noted recently, this latest round of cuts—intended to address what I’m now told is a meaningful eight-figure revenue miss, due to declines in digital video and display advertising—is only the latest in an interminable lingchi ritual that Lynch has been performing on Condé pretty much since he took the top job in 2019. Despite pledging to grow Condé’s consumer business, Lynch never diversified the revenue structure beyond continuing the ill-fated foray into video. CNE, the company’s production arm, shuttered last month. As a result, he’s been forced to downsize more and more every year. (Condé comms chief Danielle Carrig told me the company “is on track to grow revenue for the third consecutive year. We’ve been break-even to EBITDA positive for the last several years and are meeting all our targets this year.”)

Lynch’s arrival, as I’ve noted before, was heralded as an air freshener. At last, Condé Nast had hired an outsider who could bring a calculated financial discipline to its shores. No longer would the C.E.O. be flying off to Milan and Paris for meetings that turned into cultural excursions and romps. But Lynch either arrived too late in the business cycle, or he never delivered the brilliant strategy to place atop his cost-cutting regime. Many inside the building know that the old days are unrecoverable, but they wish that they were at least recognizable.

Presumably, Condé could have avoided this fate. In retrospect, one of the most obvious ideas would have been to stop investing in all the lesser titles—Self, Teen Vogue, Allure—and go all-in on transforming the most prominent brands, including Vogue, Vanity Fair and The New Yorker, for the digital era and beyond. This idea had been floated as early as a decade ago, but met firm resistance for reasons that were never quite as firmly articulated. (Instead, the company bought Pitchfork and an events business, Pop2Life, whose very dreadful name says it all…)

Back then, Condé Nast was an ego factory, which made any sort of corporate restructuring complicated. These days, however, especially after the departure of Edward Enninful, it’s Anna Wintour’s company. Lynch, on some level, is merely doing his job—making the painful but necessary cuts that will keep his brands, in whatever state, afloat for the next generation. But it’s hard to take in this moment and not wonder what Si Newhouse, constantly roaming the hallways of 350 Madison or 4 Times Square in his olive sweatshirt, would have made of the specter of a union storming the C.E.O.’s office in protest of layoffs. Back then, of course, many people would have sacrificed a useful body part to be the editor of a top Condé title. These days, it’s increasingly hard to remember who most of them are. |

|

|

|

| FOUR STORIES WE’RE TALKING ABOUT |

|

|

|

|

|

|

|

|

Need help? Review our FAQs

page or contact

us for assistance. For brand partnerships, email ads@puck.news.

|

|

You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with . To stop receiving this newsletter and/or manage all your email preferences, click here.

|

|

Puck is published by Heat Media LLC. 227 W 17th St New York, NY 10011.

|

|

|

|