|

|

Welcome back to What I’m Hearing+ as I gear up to spend my annual week in Chicago for the country’s best Emo music celebration, Riot Fest.

This week, as the strikes continue, and the window to resume productions this year begins to close, a look at how different streamers are importing international content, and what’s actually working (and what isn’t).

But first…

- The People’s Streamer: A few quick notes on Max’s new Daily Top 10, the latest effort by a streamer to improve transparency around what customers are watching and, perhaps more importantly, bring a sense of community to what is often a solitary experience. The Max ranking isn’t particularly innovative, of course: Netflix launched its own Top 10 back in 2020. But it is especially illuminating to see what people are actually watching on the platform after Warner Bros. Discovery C.E.O. David Zaslav united the highbrow HBO with the more… populist fare of Discovery.

To wit: This past Saturday, I was in the mood to watch Blade (it’s September, which is basically October, so it’s monster season in my house) and threw on Max. Within the Top 10 Series tab, there weren’t any prestigious HBO titles. Instead, I saw a spinoff of the popular Cartoon Network show Adventure Time; football docuseries Hard Knocks, ahead of the Jets’ home opener; A Discovery of Witches, from AMC+; sitcom Young Sheldon; and DC animated series Harley Quinn. (The only Discovery show was a new 90 Day Fiance spinoff, which was in 10th place.)

If your response to that lineup is “that seems perfectly average,” you’d be correct! That’s the point. Many in the industry assume that HBO is still the heart of Max, and its core value proposition. But Max isn’t a niche offering; it was designed to scale, and that means variety—crucial for families and reducing churn—is paramount. Indeed, HBO’s role in the Max bundle is actually similar to its strategic position in the old cable ecosystem: a premium addition to a mostly populist-minded offering, creating a halo effect that supports customer acquisition and price elasticity.

While consumer behavior has changed somewhat in the streaming era, the underlying logic is mostly the same. Max succeeds among certain high-value demos because of its association with prestige entertainment—it still has HBO and Turner Classic Movies! But the new Top 10 lists reaffirm that the future of Max, like Netflix, actually isn’t “gourmet cheeseburgers,” as Bela Bajaria famously noted in reference to hybrid premium-commercial hits like Bridgerton. Instead, it’s going to be a lot of sloppy joes.

|

|

| Lost in Translation |

| As Hollywood engages in its grueling labor war, and production grinds to a halt, studios and streamers are turning to a workaround: internationally-produced scripted and unscripted series. Will it work? |

|

|

|

| It’s a great time to be a Canadian or British entertainment company. With the dual SAG-AFTRA and WGA strikes showing no signs of resolution, everyone from Netflix to The CW is anxiously looking to fill gaps in their content calendars, with a potential programming black hole appearing in spring 2024. This anxiety has made internationally-produced scripted and unscripted series—which are not affected by work stoppages—exceptionally attractive, not only as a driver of customer engagement, but also as a way to keep their respective platforms and channels feeling fresh.

This workaround seems logical, and a potential life boat during a once-in-a-generation dual strike. It’s also reflective of larger abiding trends in the industry. Looking at Netflix’s original scripted titles debuting in September, it appears less than 20 percent are U.S.-based productions, as spotted by All Your Screens. (This isn’t a perfect example since so much English-language content is produced on foreign soil. But it’s still a fascinating illustrative example.) Additional data from Whip Media shows that just under 40 percent of “new Netflix shows in development are in a language other than English,” according to Hollywood Reporter. Whip Media also found that the share of non-U.S. content circulating via U.S. distributors doubled between 2018 and 2021 (8 percent to more than 16 percent respectively).

In fact, the growing share of foreign content may preview whether the streamers’ current workaround will work. And the data is… interesting. According to current viewing habits, leaning on foreign content is essentially a gamble.

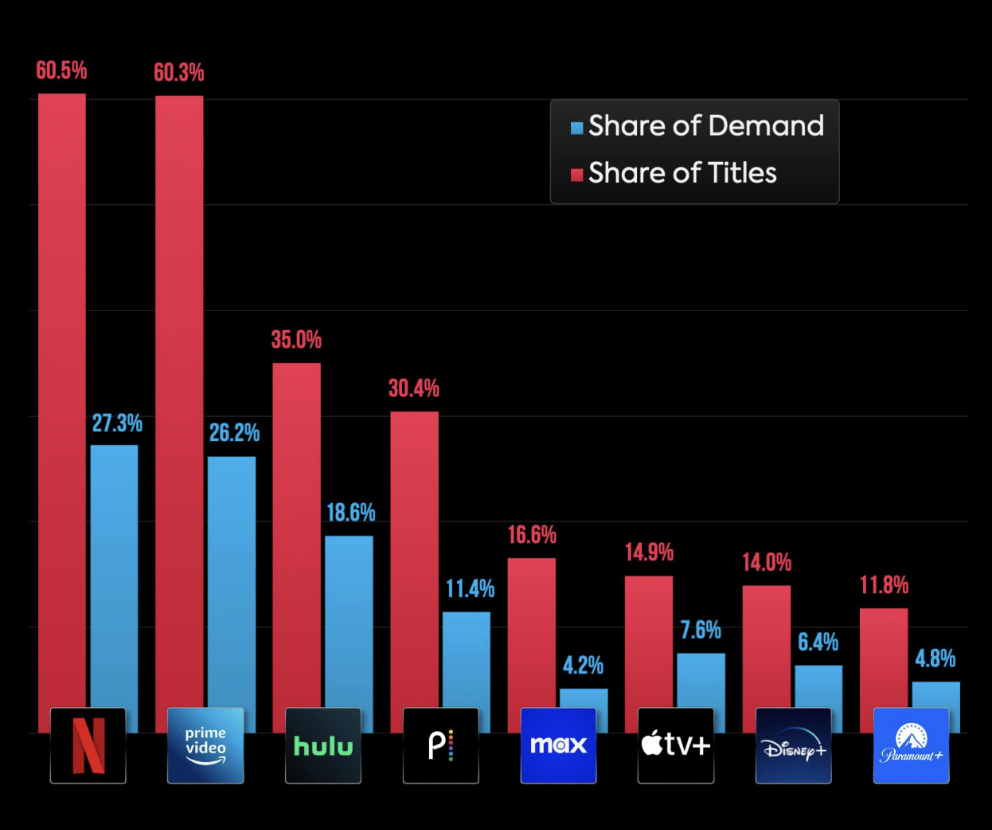

Right now, every streaming platform in the U.S. has a larger supply of international content than the level of demand for it, according to Parrot Analytics, where I work as director of strategy. Netflix, a truly international media company, unsurprisingly scores highest on both metrics: its catalog is 60.5 percent international titles, and demand for that content represents 27.3 percent of all demand. Amazon Prime Video, which is similar to Netflix in its content investment strategy, has a content catalog made up of 60.3 percent international titles, with 26.2 percent demand. |

|

| The chart above illustrates Netflix and Amazon’s running head start. This makes sense, of course: both have spent years urgently investing in regional content for local audiences, battling to become not just global entertainment behemoths, but the dominant player in every country in which they operate. They’ve positioned themselves not simply as exporters and importers of content, but also creators and distributors, while their competitors—Warner Bros. Discovery, NBCUniversal, and Paramount, for example—have been satisfied licensing their series to regional distributors, or simply to Netflix and Amazon, themselves, for cash. Recall that one of the central tenets of Netflix’s content strategy has been to create global hits (meaning hits in each country Netflix operates in) that also may travel internationally: two bites, one apple.

But how are these international shows actually performing in the U.S.? Most consumers still primarily want to watch content that reflects their own culture and is conveyed in their own language. (This is why Squid Game was such an anomaly.) While demand for non-English speaking entertainment in the U.S. jumped by 50 percent between March 2019 and April 2023, the overall demand remains relatively low, at just above 12 percent. Squid Game, Attack on Titan, Spanish-language telenovelas, and Israeli hits like Fauda are certainly finding new audiences in the U.S., but the foreign genre generally isn’t as popular as English language series. |

|

|

| Looking closer at Parrot’s data, we see the vast majority of demand for non-U.S. titles comes from the U.K., Japan, Canada, France, and Argentina. Many Japanese titles are anime, while the U.K. and Canada are English-speaking territories. (Initiatives like Hulu’s anime-heavy programming speak to streamers’ efforts to use foreign-language animated series to steal eyeballs from competitors including Max and YouTube.) Among these international titles, Japanese, Korean, and Spanish-language content accounted for the top three highest audience demand shares in the U.S. between January 2020 and January 2023, followed by Hindi in fourth.

Considering that Spanish is the most widely spoken non-English language in the U.S., it’s unsurprising that Spanish content represents a top percentage share of international series. Indians represent the second highest immigrant group after Mexican people, according to D.C. think tank Migration Policy Institute, which also explains why Hindi continues to see growth amongst content share figures. Korean might be a little more difficult to understand from a U.S. population perspective, but it does get easier when looking at one specific platform: YouTube.

But having a surplus of international content, even if demand share is relatively low when compared to domestic shows, is still beneficial to Netflix and Amazon: offering a wide array of titles gives the impression of more value to consumers, even if people don’t actually watch those titles. (Plus, they’re investing in these shows, regardless.) Consider that Hulu has less than half of the relative supply of international titles as Netflix and Amazon—and doesn’t need as much investment because it’s domestic-focused—but the demand share is nearly in-line with the demand share of Netflix and Amazon, despite its smaller investment. |

|

|

| Netflix is often credited with popularizing Korean dramas in the U.S., but YouTube, with its virtually non-existent barrier to entry, may be the platform most responsible for globalizing culture. On YouTube, there’s no subscription fee and the potential of discovering an artist or scene from a series is much higher. This is due to metadata tagging—which allows viewers to track individual talents, groups, and genres as well as specific titles—not to mention YouTube’s vast and profitable creator ecosystem.

YouTube is also particularly good at capturing and channeling network effects, such as a popular creator recommending a K-pop act to their five million subscribers. (Netflix benefits from social platforms, but isn’t one itself.) A similar phenomenon is evident with Japanese programming, like anime, where the audience and fandom are almost entirely online. Gaku Narita, the executive director of original content for Japan at Disney, acknowledged in 2020 that anime traveled well among a growing digital consumer audience, calling it a “borderless form of entertainment,” according to THR.

YouTube, in some ways, almost serves as a top-of-funnel for the SVOD players. The more that new aspects of culture are made available to audiences with limited friction, the more streaming platforms will benefit from their investment in foreign markets. Netflix, for example, is betting that its investments in Japan, Korea, and India will improve customer lifetime value and allow the company to increase pricing. Executives pay particular attention to larger cultural shifts—like the explosion of interest in K-pop or Latin American music in the U.S.—to guide their investments in local projects that might find a wider audience globally.

More audiences are willing to consume foreign content with each growing year. But even with increased globalization, and with younger audiences more willing to watch video content with subtitles—nearly 60 percent of Gen Z and 52 percent of Millennials watch video with captions, according to a recent survey from YPulse—the numbers don’t lie. Most viewers in most countries would rather watch series and films that are in their own language, and reflect their own cultures. Even as supply share and demand share increase, they aren’t making a significant impact on overall viewership.

Still, there are strategic advantages to being a content importer versus an exporter. For Netflix and Amazon, which aren’t tied to licensing-based or Pay TV distribution models, investments in local content are crucial to maximizing global reach. For WBD or NBCUniversal or Paramount, however, it’s better to be an exporter of beloved series and films. Of course, it’s difficult to predict long-term consumer behavior or cultural trends when technology, which alters both, is radically changing each year. But trying to catch up to Netflix is what got most of these companies into a jam in the first place. It’s time to learn from those mistakes and lean into what they do well instead of investing billions of dollars into something that might work—especially when it very well may not. |

|

|

|

| FOUR STORIES WE’RE TALKING ABOUT |

|

|

|

|

|

|

|

|

|

Need help? Review our FAQs

page or contact

us for assistance. For brand partnerships, email ads@puck.news.

|

|

You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with . To stop receiving this newsletter and/or manage all your email preferences, click here.

|

|

Puck is published by Heat Media LLC. 227 W 17th St New York, NY 10011.

|

|

|

|