{{ 'now' | timezone: 'America/New_York' | date: '%b %d, %Y' }} |

|

|

Welcome back to a special Friday edition of What I’m Hearing+, your extra dose of entertainment

industry intelligence. Our streaming video analyst, Julia Alexander, is here today with her definitive take on how Warner Bros. and HBO Max will help Netflix shore up weaknesses and dominate the next phase of the streaming wars. (Hint: The competition is now YouTube and TikTok, not Disney or Paramount.) Plus, her reaction to the big Disney-OpenAI news…

Take it away, Julia…

Discussed in this issue: Sam Altman,

Sora, Bob Iger, Dr. Pimple Popper, Netflix, Ted Sarandos, Neal Mohan, Greg Peters, the Ellisons, SpongeBob, Jonathan Kanter, Mark Rober, and many more… |

|

|

| Julia Alexander

|

|

-

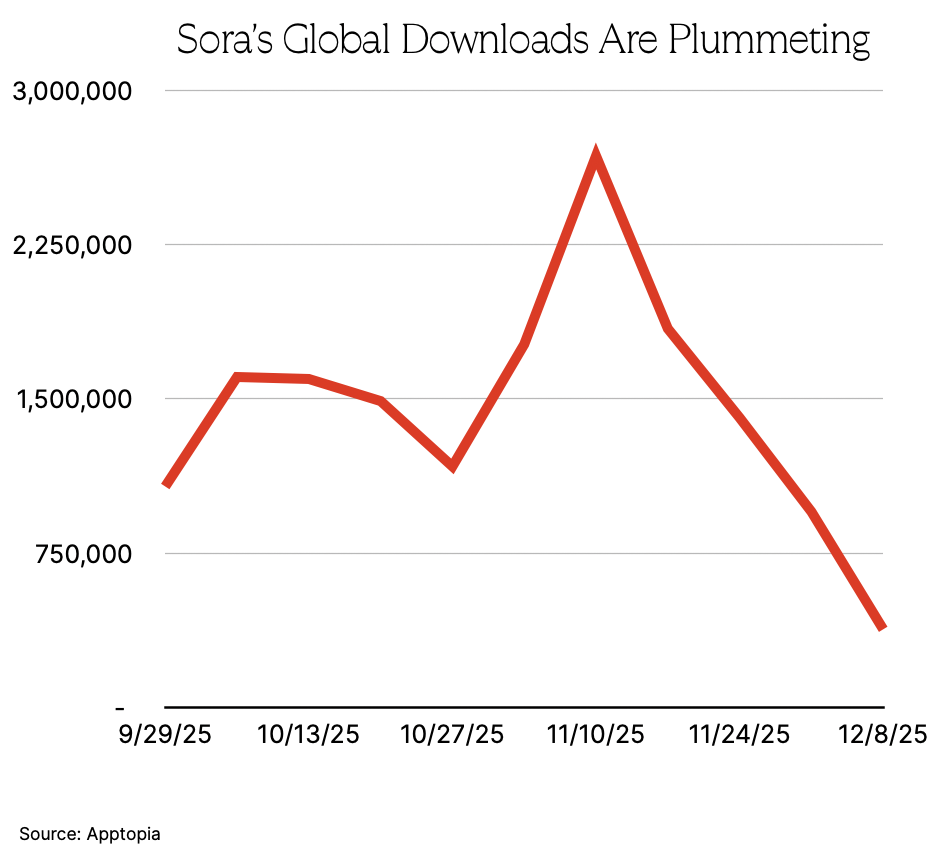

Iger’s Sora Strategy: Fear ripped through Hollywood in October when OpenAI updated Sora, its A.I. video generation app, initially with an opt-out copyright model—allowing users to spit out hyperrealistic clips of, say, SpongeBob as a D.J. or the Mario Bros. at a 12-step meeting. But it turns out that a feed of nothing but A.I. slop doesn’t have the same stickiness as TikTok or YouTube Shorts. Global Sora downloads have plummeted over the past few weeks, per App Annie,

potentially one of the many signals that led Sam Altman to reportedly pen a “code red” memo to OpenAI staff over concerns about losing market share to Google.

|

- Could

that change now that Disney has agreed to a three-year licensing agreement with OpenAI? The new deal will allow users to generate videos featuring more than 200 Disney characters—including icons from Star Wars, Marvel, and Pixar movies—which Matt wrote about last night. (The voices of actors associated with those characters

aren’t included in the deal.) In exchange, Disney is investing $1 billion into OpenAI—“schmuck insurance,” as one analyst put it—and placing itself on the cap table of one of the world’s fastest-growing companies. Disney simultaneously sent a cease-and-desist letter to Google, which might be an opening bid for another licensing deal.

Anyway, here’s my counterargument to those who believe this heralds the entertainment slop-ocalypse. The digital fan fiction that Disney is permitting will

create far more positive engagement for Disney+ than for Sora. Users may not want their feeds made up entirely of generative A.I. slop, but they might not mind a bit of slop populating the same app as The Simpsons and Percy Jackson, etcetera. And the truth is, shortform video creators are going to make these kinds of edits with copyrighted characters anyway. So Disney might as well capitalize on its intimate connection with fans. Given that the options are either

hoping the A.I. genie reenters the bottle or leveraging the technology to benefit your business, I suspect C.E.O. Bob Iger is on the right side of history.

|

|

|

Prior to its $83 billion deal to acquire the studio and HBO Max, the streamer had never

spent more than $700 million on an acquisition. But Netflix saw an opportunity to own, not license, a significant chunk of its content—and, perhaps more importantly, to block David Ellison from taking it away. |

|

|

For the longest time, Netflix co-C.E.O. Ted Sarandos could walk into his office off Sunset

Boulevard secure in the knowledge that a relatively simple strategy would keep the world’s largest streamer in first place: pairing high-quality original titles with an endless scroll of algorithmically optimized licensed content. That playbook, more or less, has made Netflix the envy of the industry and more than satisfied users despite price hikes and password-sharing crackdowns. And everyone in town knew it—which is why it was such a shocker when the company, which had never before

spent more than $700 million on an acquisition, suddenly bid $83 billion for the non-cable assets of Warner Bros. Discovery.

On some level, Netflix’s bid seems like an aggressive, winner-take-all strategy. Despite the pesky theatrical business that Sarandos has so often dismissed, Warners is filled with accretive assets—starting with its historic film and television library. The Netflix–Warner Bros. deal—which is expected to close in 2026 barring the outcome of the

Ellisons’ hostile bid saga—would create one of the largest libraries held by any major streamer. It’s a good library, too: Friends, Harry Potter, Batman, Game of Thrones… this isn’t the Discovery Channel junk like Dr. Pimple Popper, which is being spun off with Global Networks. |

|

|

A MESSAGE FROM OUR SPONSOR |

Stars Jeremy Allen White and Jeremy Strong and Director

Scott Cooper on the love story between Bruce Springsteen and Jon Landau, the guidance of Bruce and Jon while making the film, and staying true to “Nebraska.” [READ HERE] |

|

|

Then there are the cost savings. Licensed content accounts for an estimated 44 percent of Netflix viewing

hours, and about a quarter of that comes from Warners titles, according to Peter Supino of Wolfe Research. The prospect of adding HBO’s back catalog, in particular, is the stuff of content executive dreams: According to research firm Samba, 78 percent of user engagement on HBO Max in 2025 came from titles released in 2024 or earlier—the second-highest among the premium streamers. And Netflix is one of the few companies that can make such a library even more

valuable, thanks to its global scale and technology. With the Warners deal, Netflix will own that upside, rather than renting it, which is foundational to the company’s business model.

But Netflix also needs Warners more than most people care to think. After all, roughly half of its business is dependent on partners whose own objectives might change. If David Ellison gets his way, for instance, an emboldened and enhanced Paramount Skydance Warners

could reduce or completely remove its content from Netflix over time. In that case, Netflix would be forced to further invest in original content, which is riskier and more expensive. Meanwhile, Sarandos and co-C.E.O. Greg Peters are also warily—and justifiably—eyeing not just YouTube but also the proliferation of free, ad-supported TV services, which have increased viewer engagement by 43 percent between 2024 and 2025, according to Comscore. Tubi, for example, is one of the

fastest-growing services in the U.S., with a 2.2 percent share of all TV viewing time in October—about double that of HBO Max and Discovery+ combined—per Nielsen’s Gauge report.

Investors clearly seem uneasy with the $83 billion in enterprise value that Netflix has proffered to stay ahead of the competition. (And yes, that price could go higher if Ellison raises his hostile bid.) But Sarandos, Peters, and their biz-dev soldiers are asking themselves the same questions that YouTube’s

Neal Mohan and Ellison’s own team are asking: What happens if Netflix doesn’t get Warners? And what if the company can’t grow engagement on its own? Or what if YouTube and TikTok overtake Netflix in connected TV ad spend at the same time that Tubi and a combined Paramount-WBD start making inroads in the market? Netflix may have won the first round of the streaming wars, but the battle for our attention never ends. |

At the nucleus of the deal has been the assumption that Netflix would inevitably mash up its service with HBO

Max—a combo that, analysts believe, would control anywhere from 30 to 40 percent of the U.S. streaming market. In a note to subscribers after the deal was announced, Netflix said that the two services would continue operating separately. But that seemed like a Sure, Jan head fake amid intense regulatory scrutiny—much like Sarandos’s vow to keep putting Warner Bros. movies in theaters until, well, he decides not to. Indeed, the antitrust division of the D.O.J.—and the Ellisons—will

certainly scrutinize the monopolistic potential of this streaming marriage. (Former Biden administration antitrust chief Jonathan Kanter recently laid out the merits of the Ellison argument on The Town.)

But integrating Netflix and HBO Max might not be nearly as simple as the D.O.J., the Ellisons, WBD shareholders, and

the entertainment industry as a whole think it will. Despite being the fourth-largest global streamer, HBO Max is an imperfect product. It has higher-than-average churn, and WBD’s presale growth hacking was accomplished through more intermediation. Whereas people subscribe directly to Netflix, many access HBO Max as an add-on via a cable bundle or another service, like its deal with Disney+ and Hulu. That could pose a barrier to seamless integration.

The biggest challenge for

Netflix will be combining two distinct brands, tech platforms, and subscriber files. (Fortunately, both services already offer a similar tiered pricing structure.) Close to 4 million HBO Max customers were subscribed through Amazon Prime Video Channels as of November, according to Antenna. HBO Max is also available through a plethora of other digital aggregators that Netflix has ignored: The Roku Channel, YouTube TV, YouTube Primetime Channels, Philo, etcetera. In aggregate, these

customers become difficult to port over to Netflix, if they don’t already subscribe.

Meanwhile, there are an estimated 10.6 million U.S. subscribers with both HBO Max and Netflix, according to Antenna, which represents about 45.2 percent of HBO Max customers in the U.S., but only 15.3 percent of Netflix subscribers. With a little more than half of HBO Max’s U.S. base not subscribed to Netflix, per Antenna’s calculations, it could represent a strong growth opportunity. But given that

Netflix’s churn rate hovers at just around 2 percent, it’s possible that the HBO customers who don’t already have Netflix actually don’t want it.

Rather than force the integration on the consumer side, perhaps the best way to realize the true potential of a combined Netflix-WBD offering would come through the creation of a new super-app. After all, the market has clearly demonstrated a preference for cheaper, consolidated services. Customers are now spending $30 less on streaming

than in 2021 because they’re subscribed to fewer services overall, according to Park Research, with the average spend hovering around $60 a month. In Q1 2024, 20 percent of U.S. internet households reported paying for nine or more services, versus 29 percent in Q3 2023. The overall average number of streaming video service subscriptions per household has now dropped below five. |

|

|

A MESSAGE FROM OUR SPONSOR |

Stars Jeremy Allen White, Jeremy Strong, and Odessa Young,

Casting Director Francine Maisler, and Writer/Director/Producer Scott Cooper break down how the stellar ensemble came together, how they prepared for their roles, and what it was like having Bruce Springsteen on set. [WATCH NOW] |

|

|

Certainly, people are already trying to figure out how an HBO Max “add-on” to Netflix would look through a

bundled system. About one in five HBO Max subscribers are part of the Disney+/Hulu bundle, according to Antenna. And even if Sarandos and Peters are tempted to disengage from this deal and go it on their own, the data will instruct them otherwise. Roughly 80 percent of HBO Max/Disney+/Hulu bundle customers remained subscribed after three months. By contrast, HBO Max on its own had an 8 percent monthly churn rate in October.

Netflix is presumably modeling out the various benefits of

maintaining these HBO Max partnerships versus letting them expire in favor of one super-app. The potential outcomes are manifold, of course, and it may explain why Sarandos could credibly claim that the companies will be operated separately—at least for a time. But I suspect that Sarandos and Peters will consider a bundled product that contains a new premium tier with access to HBO—thereby having it on Netflix but marketed as “top shelf” entertainment and better monetizing the

programming. Similarly, I suspect it may also behoove them to explore a free top-of-funnel tier—an experimental access point into Netflix that generates more advertising revenue on a collection of licensed programming and some originals.

They may not have a choice any longer. Free television, whether driven by YouTube or platforms like Tubi, is driving more usage every month due to two diametrically opposed needs. YouTube is home to new content from creators that is produced at a

speed that Netflix can’t match. At the same time, free streamers like Tubi and Pluto TV are home to laid-back, nostalgia driven, niche targeted libraries. Netflix sits squat in the middle. To maintain its lead over the next few years, it needs a solution for both markets. |

On a macro level, Netflix has more than just the rival streamers on its mind: The company openly wants to

dominate all viewing worldwide. Netflix launched an entire games division, which has undergone significant revamping, and experimented with shortform video, largely unsuccessfully. Now, Netflix is working with YouTube creators like Ms. Rachel and Mark Rober and bringing over Ringer podcasts from Spotify in an attempt to recapture engagement that is shifting to user-generated platforms.

Sarandos may have once strutted into headquarters every day

with an air of confidence, but Netflix and its executives know the company isn’t just competing with Disney or Paramount any longer. (Of course, this is the argument that its lawyers at Skaaden will make to the D.O.J., too.) But trying to compete with YouTube, especially when playing by YouTube’s rules, is a losing proposition. As Peters noted at a conference this week, the combination of Netflix and Warners would take the merged company to just over 9 percent of TV viewing hours in the U.S., up from

8 percent today. Even then, he said, “We’re still behind YouTube at 13 percent.”

Peters wants to downplay any monopolist claims as the deal heads to regulatory review, but he’s also not wrong. Netflix has to find a way to insulate itself from YouTube’s dominance if it wants to remain in first place among premium S.V.O.D.s. Netflix’s perceived moat around its streaming business isn’t any guarantee in the exponentially larger video space. |

Thanks, Julia. I’ll see everyone on Monday.

Matt |

|

|

Need help? Review our FAQ page or contact us for assistance. For brand partnerships, email ads@puck.news. You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with {{customer.email}}. To stop receiving this newsletter and/or manage all your email preferences, click here. |

Puck is published by Heat Media LLC. 107 Greenwich St., New York, NY 10006 |

|

|

|