{{ 'now' | timezone: 'America/New_York' | date: '%b %d, %Y' }} |

|

|

Welcome back to an extra-special bonus edition of What I’m Hearing+, fresh from today’s

West Coast media event in the Paramount commissary with David Ellison and his new leadership team. I’ll save my notes on the highly choreographed affair for tomorrow’s WIH Proper, except to say the cookies were delicious and it was nice to see fellow Puck-sters Dylan Byers and Kim Masters not on Zoom. Dylan really has great hair.

Tonight, Julia Alexander is back with an analysis of the latest Peacock numbers and its

peculiar (and, let’s be honest, perilous) place in the streaming landscape.

Take it away, Julia… |

|

|

A MESSAGE FROM OUR SPONSOR |

|

|

| Julia Alexander

|

|

- How big is Prime Video,

really?: It’s hard to quantify Amazon Prime Video’s true audience—Prime doesn’t break out a number separately from its broader membership, so it’s impossible to discern who’s there for the latest John Cena action-comedy and who’s shopping for cheap toilet paper. But Kagan, S&P Global’s intelligence firm, estimates in a new report that Prime Video has roughly 90 million subs in the U.S.—which likely puts it slightly ahead of Netflix, which had 90 million

subs in the U.S. and Canada before it stopped reporting those numbers earlier this year. Most interestingly, about 4.3 million of these subscribers are not Prime customers. Some people are just there for Heads of State.

Another fun finding from Kagan: There are roughly 85.1 million subs on Prime Video’s ad tier in the U.S., which means that 95 percent of its domestic users are seeing ads. This makes sense, since Prime Video charges an extra $3 to opt out of ads.

For context, Netflix has 94 million monthly active users on its ad tier globally, out of about 300 million total subscribers; the worldwide ad-viewing proportion of its audience is only about 30 percent. - Disney’s big Webtoon move: If there’s a mantra driving Disney’s corporate strategy over the past five years, it’s meeting audiences where they are. To wit: The company built a digital theme park within Fortnite,

and reimagined ESPN as a betting- and fantasy-driven app. Yesterday, Disney announced a partnership with Webtoon to bring 100 character-driven comics to the popular web comics app. Daniel Fink, Disney’s head of digital innovation for consumer products, told Variety that it’s one of the largest

publishing partnerships they’ve ever done.

Webtoon, which went public in the U.S. last year, doesn’t get much attention, even though Webtoon Studios, which includes Wattpad Studios, has produced several top-performing Netflix shows (All of Us Are Dead, Hellbound) and a feature (The Kissing Booth). More importantly for Disney, Webtoon reaches 155 million monthly active users, and is especially popular in Korea and Japan—territories where Disney is trying to grow

its streaming service. Expect to see more of these deals as studios aggressively look for audiences beyond their owned-and-operated channels.

|

|

|

And now, on to the main event… |

|

|

Peacock isn’t just unprofitable—it’s the only major U.S. streamer

without a vision for a future beyond sports. Alas, a platform can’t live on the NBA and Love Island alone, and the Philadelphia brain trust will have to get creative (and raise prices) if they want to compete. |

|

|

Surely, something has to change at Peacock, the last of the major streaming services to still be

unprofitable. Yes, Paramount+ just barely crossed that milestone, and will probably start losing money again once that $7.7 billion UFC deal hits the P&L. But at least David Ellison appears to have a vision for where the newly merged Paramount-Skydance Corporation is headed in streaming. Over at Disney, ESPN chief Jimmy Pitaro

is striking deals with the NFL, and C.E.O. Bob Iger is folding Hulu into a Disney+ super app. Warner Bros. Discovery C.E.O. David Zaslav, who’s in the midst of spatchcocking his company, appears open to M&A.

Comcast boss Brian Roberts is also charting a new course by spinning out the company’s linear assets (minus NBC and Bravo) as Versant. And yes, Peacock is seeing some momentum, doubling its share of subscriber additions

between May and June, per Antenna. There’s no question as to why: A big part of those June additions likely came from one show. Love Island is a massive hit—it was Nielsen’s most streamed show last week, and is Peacock’s most watched original title. Not to mention there are positive signs on the advertising front, with Peacock driving more than a third of NBCUniversal’s ad volume this year, according to Roberts, up 20 percent from the year before.

And yet, it’s not clear what’s

next for Peacock after the Versant separation. Nothing—not the Olympics, not the NFL, not even Love Island—has been able to increase Peacock’s share of total TV viewing time beyond 2 percent in the U.S., which is well behind Disney’s combined near 5 percent, Netflix’s 8.3 percent, and YouTube’s 12.8 percent, according to Nielsen. Earlier this year, NBCU signed a $2.45 billion-a-year deal with the NBA to broadcast games for the next 11 years, after data suggested that people who signed

up for Peacock to watch January’s NFL playoff game stuck around to watch other content afterward. But it’s a big and otherwise unproven bet. Peacock’s churn rate currently runs 2 percentage points above the national average. |

|

|

A MESSAGE FROM OUR SPONSOR |

|

|

If there’s a path to profitability for Peacock, it probably starts with extracting more revenue from its

existing sports-watching audience (and finding more Love Island–adjacent hits, without overspending). Last month, NBCU announced a price hike of $36 a year for both the ad-tier Premium (now $11 a month) and the limited-ads Premium Plus (now $17 a month), which is more expensive than Paramount+, comparable to HBO Max, and still cheaper than bundles like the ad-free version of Disney+ and Hulu ($20 a month). Arguably, this is an overdue correction for a product that will soon have

the NFL, Premier League soccer, college football, and those newly acquired NBA games starting this fall. Indeed, Peacock has long been underpriced relative to what it delivers.

But the real test will arrive in Q4, when consumers finally weigh the streamer’s new pricing against its expanded portfolio. If Roberts whiffs with his huge, decade-long, multibillion-dollar NBA deal, Peacock could find itself in the uncomfortable position of overpaying for temporary sports rights that

don’t generate long-term brand value. Is there still room to increase Peacock’s 41 million subscriber base—which has grown steadily during the last few years, thanks to the NFL, but has slowed recently—with the addition of the NBA? Or will price-sensitive consumers, tempted by the new ESPN/Fox bundle (available in October for $40 a month), decide their money is better spent elsewhere? |

Sports fans are less price-sensitive than other streaming subscribers. This cohort spends an average of about

$111 a month on streaming services, according to research firm Parks Associates, nearly twice what non-sports fans spend. Around 40 percent of identified sports fans are also streaming-only customers.

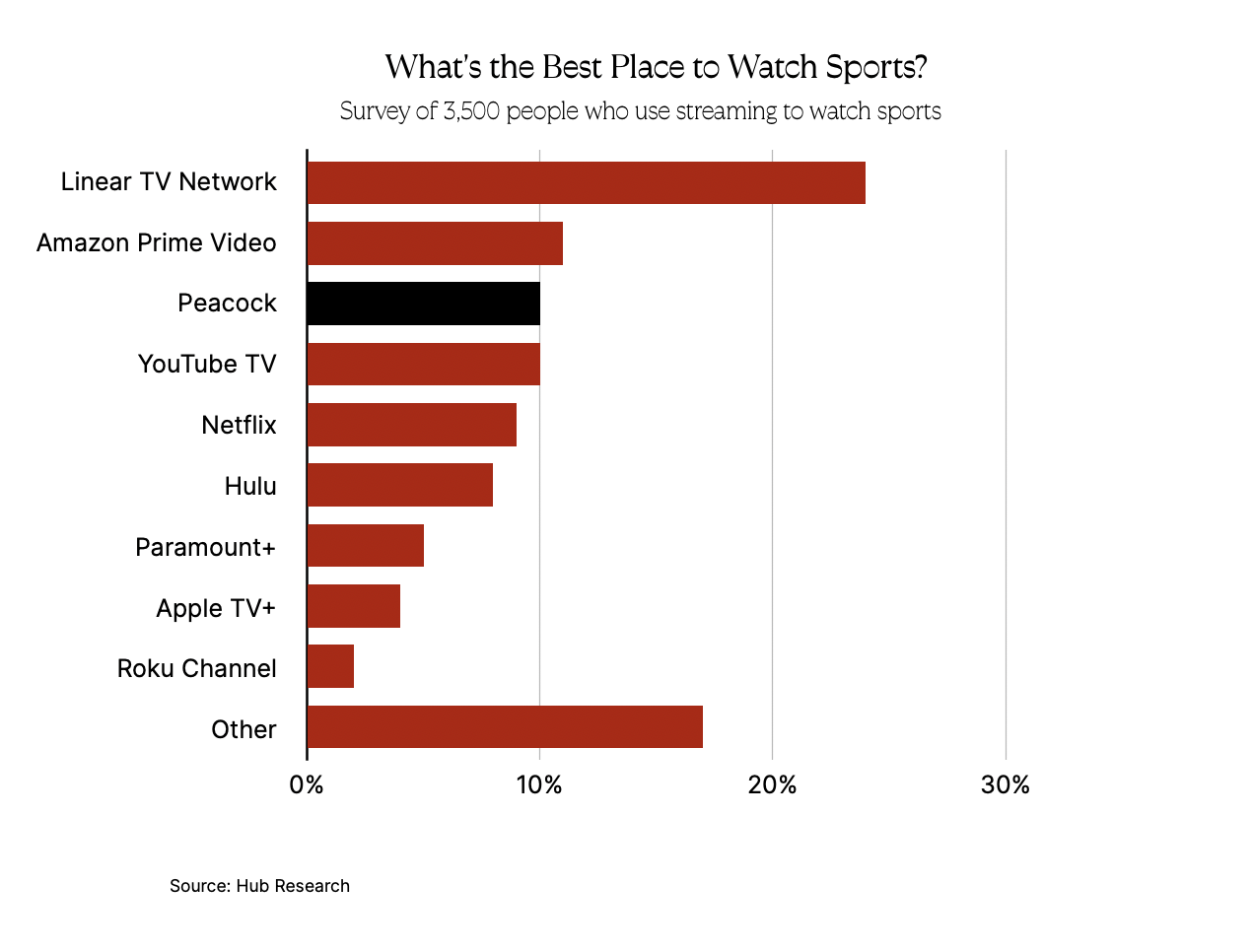

No matter where you look, the data underscores why Comcast has invested in this segment and in the NBA. A Kagan report found that the NBA was second only to the NFL, excluding the Olympics, among sports that most interest streaming-first fans. Meanwhile, according to a Hub

Entertainment Research survey from last August, Peacock ranked second among streaming platforms as the best place to watch games, just behind Amazon Prime Video.

Still, Peacock will need to thoughtfully manage consumer expectations if it’s going to keep charging more. The streamer’s recent price increases were substantial, nearly 40 percent in the case of the Premium tier. At the same time, NBCU is moving some library content off of Peacock’s free and Select tiers, incentivizing users to upgrade for full

access to films and Peacock originals. Much of the sought-after sports content, Peacock’s big draw, is now exclusive to Premium tiers. NBCU executives are betting the approach will boost revenue overall, as the NBA season flows into a winter lineup that will include the Super Bowl, the Winter Olympics, and the World Cup. Even if Peacock continues to slowly ratchet up prices to, say, $20 a month, the Premium Plus offering would still be more attractive than the forthcoming stand-alone ESPN app

($30 a month) and on par with Fox One ($20). At least, that’s the idea. |

Of course, for Peacock to go toe-to-toe with other streamers, it needs a more diversified strategy than just

sports rights and price hikes. Even with crucial assets like the NFL and a potential growth gold mine in Premier League soccer rights, Peacock isn’t engaging audiences at the frequency required to draw in advertisers who want to appear against non-sports content. In June, Peacock secured a 1.5 percent share of TV time in the U.S., behind every other major streamer except HBO Max. Netflix, Disney+, and Hulu have far less “must-watch” big-ticket programming, but nevertheless manage to surpass

Peacock each month.

To take more market share, Peacock needs to build the right complementary programming. Over at Paramount, for instance, Ellison seems to have a clear psychographic profile of the audience he’s building, combining UFC fans with Taylor Sheridan devotees, South Park bros, CBS crime procedural addicts, etcetera. Sure, Peacock has its own investment thesis: In short, to offer a little bit of something for everyone—football and basketball

for Dad, Bravo for Mom, and Minions for the kids. The problem isn’t the diversity of content; it’s the ability to break through when it’s getting outspent. Netflix spends billions more than NBCU on content every quarter, and that means there is literally something for everyone, even if it’s not always as good as the premium I.P. flowing into Peacock.

NBCU ought to be thinking more strategically about bundling, too. As I

wrote last week, the recent Disney+ and HBO Max bundle drove 2.2 million new subscribers by the end of 2024, per Antenna, with high retention. That’s why Disney and Fox are partnering, and why Paramount+ and HBO Max are considering similar moves. Certainly, Peacock’s sports rights would make it an attractive partner, especially for HBO Max as it pulls back on growth

tactics and focuses on its premium I.P.

Indeed, an HBO Max/Peacock bundle would bring sports to HBO Max, and more premium entertainment to Peacock. Not to mention that such a bundle offers the potential for extraordinary rewards with no major investment on Roberts’ or Zaslav’s part. And it might allow them to really dig into each other’s businesses—the first step, perhaps, to a more lasting partnership. |

A partnership could also, of course, serve as a prelude to a merger, whether a full acquisition or joint

venture. One insider recently told my colleague Kim Masters that Roberts might want Warner Bros. Discovery properties to prop up the Universal theme parks business, which is a growing segment of Comcast’s revenue. But if the rumors are true that Ellison has his eyes on Warner Bros., time may be running out for Roberts to make a

move. He needs to strike a deal that works for him, rather than just whatever becomes unavoidable down the road. |

Thanks, Julia. See everyone tomorrow.

Matt |

|

|

Puck founding partner Matt Belloni takes you inside the business of Hollywood, using exclusive reporting and insight to explain

the backstories on everything from Marvel movies to the streaming wars. |

|

|

A professional-grade rundown on the business of sports from John Ourand, the industry’s preeminent journalist, covering the

leagues, players, agencies, media deals, and the egos fueling it all. |

|

|

Need help? Review our FAQ page or contact us for assistance. For brand partnerships, email ads@puck.news. You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with {{customer.email}}. To stop receiving this newsletter and/or manage all your email preferences, click here. |

Puck is published by Heat Media LLC. 107 Greenwich St, New York, NY 10006 |

|

|

|