Welcome back to another preview of our special Wednesday offering, starring data analyst Julia Alexander. By the end of July, this email will be for Inner Circle members only, so upgrade here.

Tonight, heading into the annual Cannes Lion advertising boondoggle—sorry, celebration of creativity—Julia tackles the topic of ads on Netflix, specifically the great migration happening from the O.G. ad-free service to the increasingly popular (read: less expensive) ad-supported tier. Yes, she’s got charts and graphs galore. Plus, her thoughts on the long-awaited valuation of Hulu, and what Disney might do next with its $9 billion acquisition. And one of Gunnar Wiedenfels’ first looming challenges at Warner Discovery’s TV spinoff.

|

|

|

|

A MESSAGE FROM OUR SPONSOR

|

|

“Rian Johnson and Natasha Lyonne's murder mystery is a gift for TV lovers everywhere"

|

|

“A magnetic performance from Natasha Lyonne, clever writing, and a laundry list of comedic guest stars”

|

|

“Season 2 of might be the most purely enjoyable show on TV”

|

[WATCH] Natasha Lyonne talks ‘Poker Face’ S2

Natasha Lyonne joins TODAY to talk about the second season of her hit Emmy Award-winning series “Poker Face” where she plays Charlie Cale, an ex-casino worker-turned-detective who happens to be a human lie detector.

|

|

For more on POKER FACE, visit PeacockFYC.com

|

|

|

|

Julia Alexander |

|

- Cable: Not dead yet!: Reports of the multichannel TV bundle’s demise may be a bit premature. A new McKinsey survey finds 75 percent of remaining U.S. cable subscribers haven’t seriously considered canceling in the past six months. McKinsey isn’t known for its sense of humor, but the report

happens to include the terribly obvious and unintentionally hilarious statistic that 94 percent of the Baby Boomer demo (born 1946-1964) aren’t thinking of cutting the cord anytime soon. Somebody is watching all those life insurance, gutter guard, and plaque psoriasis ads.That’s a bit of good news for Mark Lazarus and Gunnar Wiedenfels as they steward the profitable but declining TV assets to be spun out of NBCUniversal and Warner Bros. Discovery, respectively. We may not know what the short-term floor for cable is just yet, but we’re getting close, and it looks like those entities that remain in the traditional pay TV system—about 48 million homes—are significantly less likely to churn than many expected.

- Hulu’s real value: Disney finally owns all of Hulu, and Bob Iger got it for far less than both Comcast’s Brian Roberts and most analysts assumed.

If you recall, back in 2023, the two sides agreed that Disney would pay a floor price of $8.61 billion for the third of Hulu that Comcast controlled, but they couldn’t agree on a final valuation. Disney said that was plenty; Comcast wanted $5 billion more. On Monday, they revealed that an arbitrator awarded Comcast $439 million more, for a total of just over $9 billion.There are two ways to look at that final number. First, perhaps Hulu simply wasn’t as valuable as many originally thought—a reality underscored by the market caps of WBD ($26 billion) and Paramount (around $9 billion), although neither is a perfect comp for all the obvious reasons. Second, Hulu’s strategic value to Disney is hard to quantify. After all, its real untapped value is in providing a one-stop platform for all of Disney’s streaming options—a hub for browsing when you’re not sure what to watch.

Iger appeared on CNBC earlier this week, and confirmed that his team is “focused on doing what we intended to do once we gain full control of this, and that’s basically to put these apps together seamlessly.” I’ve long thought Disney+ should have been a tile within Hulu, a portal to the company’s highest-value I.P., integrated among other general entertainment. Iger, in his interview, suggested Disney will go in the opposite direction, “turning Hulu into a more global brand as part of the Disney+ offering.” Still, uniformity is everything at Disney: Expect far more Disney+ and ESPN content on its own platform, too.

Also, now that the deal has closed, Iger can finally invest in the Hulu tech stack, which has been somewhat neglected for years, without driving up the value of a product he was trying to buy. Hulu can now safely go from being a piece of Disney’s business to the center of its audience development plan. (Disclosure: I worked within Disney Streaming until recently.)

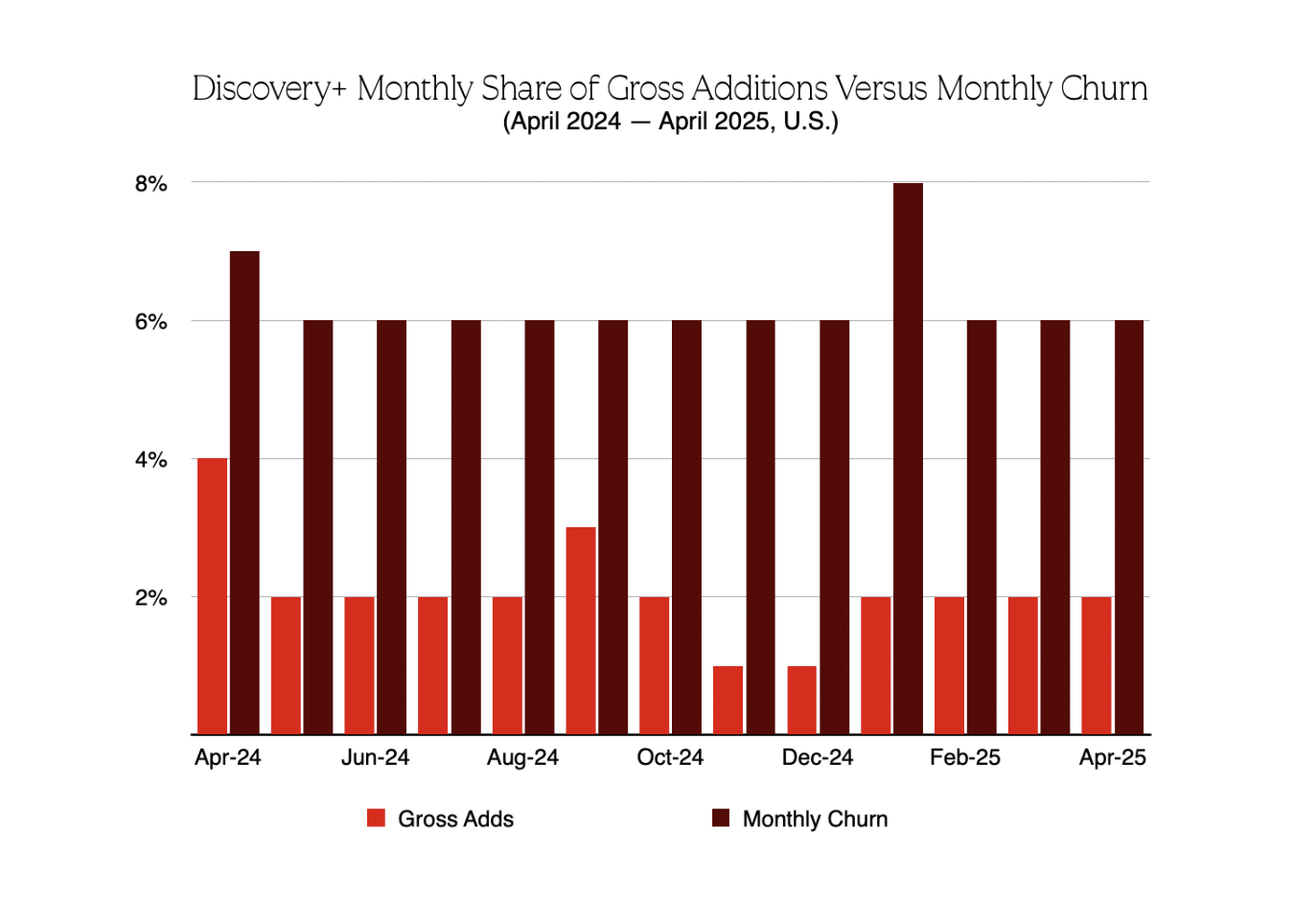

- The Discovery+ of it all: Amid all the obsessive coverage of WBD’s corporate divorce and what it might mean for HBO Max, far less attention has been paid to Discovery+, the small streamer that will sit within Wiedenfels’ Global Networks, alongside the declining linear TV assets. The numbers don’t lie: Warner Bros. Discovery doesn’t break out Discovery+ subscribers on their own, instead looping them into the larger D.T.C. numbers. But reporting from Antenna shows it has seen a consistent slowdown in sub growth since April of last year, with its monthly share of new U.S. subscriptions falling from 4 percent to 2 percent, and being outpaced by churn.The number of new monthly signups in April sat at just under 320,000—less than half the number picked up by Starz. Perhaps even more concerning, a new analysis from McKinsey shows that subscribers to niche streamers are more than twice as likely to churn as those who subscribe to more general-entertainment services.

|

- If there’s anything we know about Gunnar, though, it’s that he’s a financial shark, so I’ll be curious to see what he does with Discovery+. Lean into it to generate as much additional ad revenue as possible while slicing overhead with more layoffs? Or shutter it entirely?

|

|

|

|

The leading streaming service is trying to crack the advertising code without cannibalizing its own 300 million-strong subscriber base. It’s kind of, sort of, working.

|

|

|

I was at the annual StreamTV conference in Denver this week, and nearly every conversation I had coalesced around the age-old topic of advertising, which is suddenly very much back in vogue. There are only so many streamers that people are willing to pay for, so the momentum these days largely favors free or heavily ad-supported platforms—like YouTube, which is eating premium media’s lunch.

In November 2022, Netflix famously introduced its ad-supported tier, which now reaches more than 94 million monthly active users: 125 percent growth year-over-year, as of May. But everyone in the industry is still poring over the data, trying to get a handle on the risks of cannibalization of the ad-free subscriber base and the potential upside—the moment when, or if, the revenue per sub for less-expensive advertising tiers might actually surpass the ad-free options.

Back in late ’22, co-C.E.O.s Ted Sarandos and Greg Peters told nervous shareholders that the risk of cannibalization was minimal—they didn’t believe legions of ad-free subscribers would simply opt into the less-expensive ad tiers. Peters pointed to various benefits of the more premium tier, like 4K streaming, as “sticky points.” For what it’s worth, I wasn’t entirely sure I believed them, but I was excited to observe the experiment.

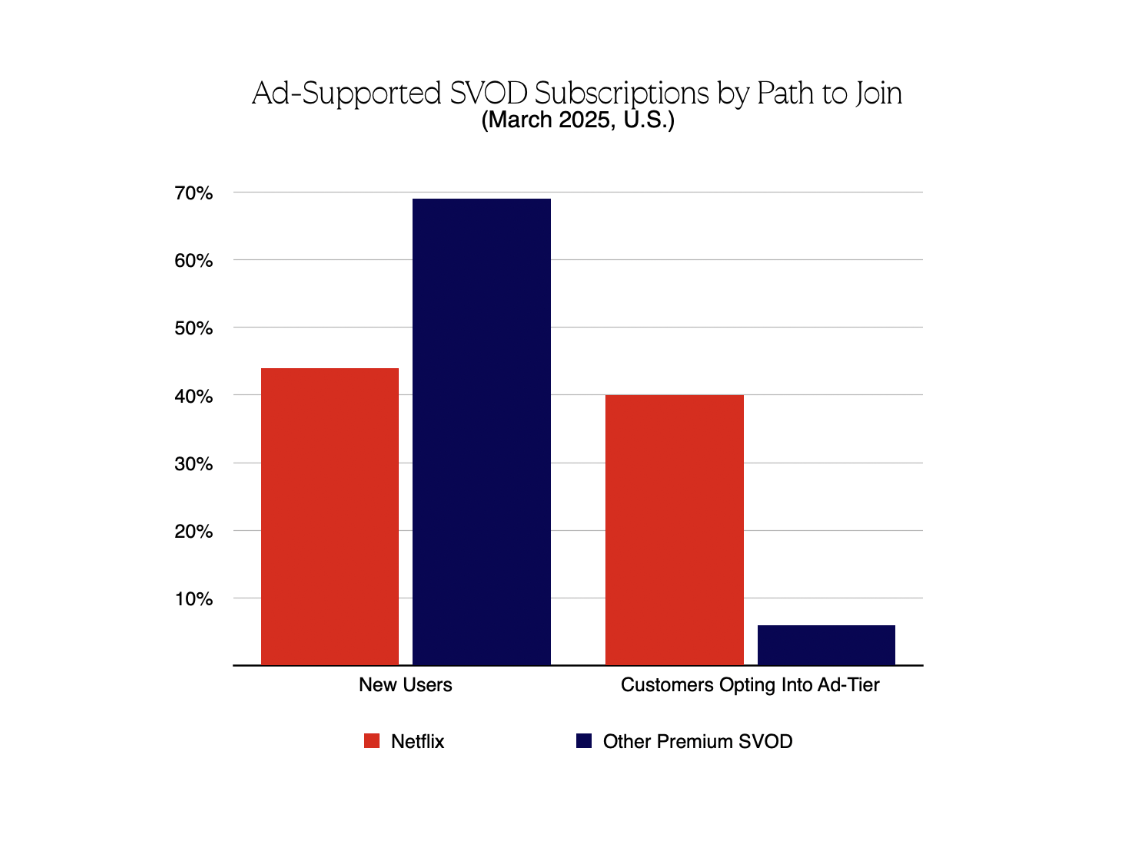

Now, though, a clearer picture of Netflix’s transition from a pure sub-driven business to a hybrid model is coming into view. According to new data from Antenna, in March 2025, 40 percent of customers on the ad-supported tier had switched over from paying full freight, nearly equal to the 44 percent who entered as new users. (About 16 percent of ad-tier customers were win-backs—lapsed subscribers who signed back up.) By comparison, at other streamers, nearly seven in 10 people on the ad tier are new users. Peters may have not anticipated people’s willingness to watch ads for a cheaper price, despite the oversaturation of streaming offerings in the U.S. At Netflix, it seems, a great migration is already underway—and that’s not necessarily a bad thing. In fact, it seems to be precisely what Netflix wants.

|

When Netflix first launched its ad tier, its average revenue per user immediately dropped in the U.S. and Canada, even as total subscribers grew. It took until the fourth quarter of 2023 for that ARPU to meaningfully increase. And that was only after Netflix instituted a price increase. At the time, the changes appeared to work. An analysis from advertising expert Eric Seufert suggested that ARPU from Netflix’s standard ad-supported tier was indeed higher than the ad-free option.

|

|

|

|

A MESSAGE FROM OUR SPONSOR

|

|

“A top-notch thriller, with dazzling action sequences and smart storytelling”

“It’s mesmerizing to watch Eddie Redmayne methodically go to work”

|

|

“Exhilarating. So relentlessly good.”

|

|

- The Wall Street Journal

|

|

For more on THE DAY OF THE JACKAL, visit PeacockFYC.com

|

|

|

But that was before global ad market growth slowed. In the summer of 2024, Netflix started lowering its CPMs. That July, the company also moved to discontinue its basic plan—its cheapest ad-free plan—which prompted many users to opt into an ad-supported tier. This was a “catalyst event,” Rameez Tase, Antenna’s co-founder and president, told me, “requiring subscribers of that plan to opt into a different plan in order to maintain access to the service.” The strategy appeared twofold. Netflix wanted to use its ad tier to attract new customers, and better monetize its existing price-sensitive subscribers via ads. The Antenna numbers suggest that it is effectively achieving both aims.

This past quarter, Netflix stopped reporting subscriber additions, and no longer discloses ARPU, which makes it difficult to assess where things stand. But Netflix executives have acknowledged in the past that its ad

tier produces more aggregate ARPU than its standard package, and we can observe supporting trends using other data points. This year, Netflix’s ad tier is expected to drive more than $3 billion in revenue, according to research firm Omdia. In April, The Wall Street Journal reported that Netflix hopes to earn $9 billion in global ad sales by 2030. The company also jumped from representing just 1 percent of all ad-tier subs in the U.S., in Q1 2023, to 15 percent two years later, per Antenna.

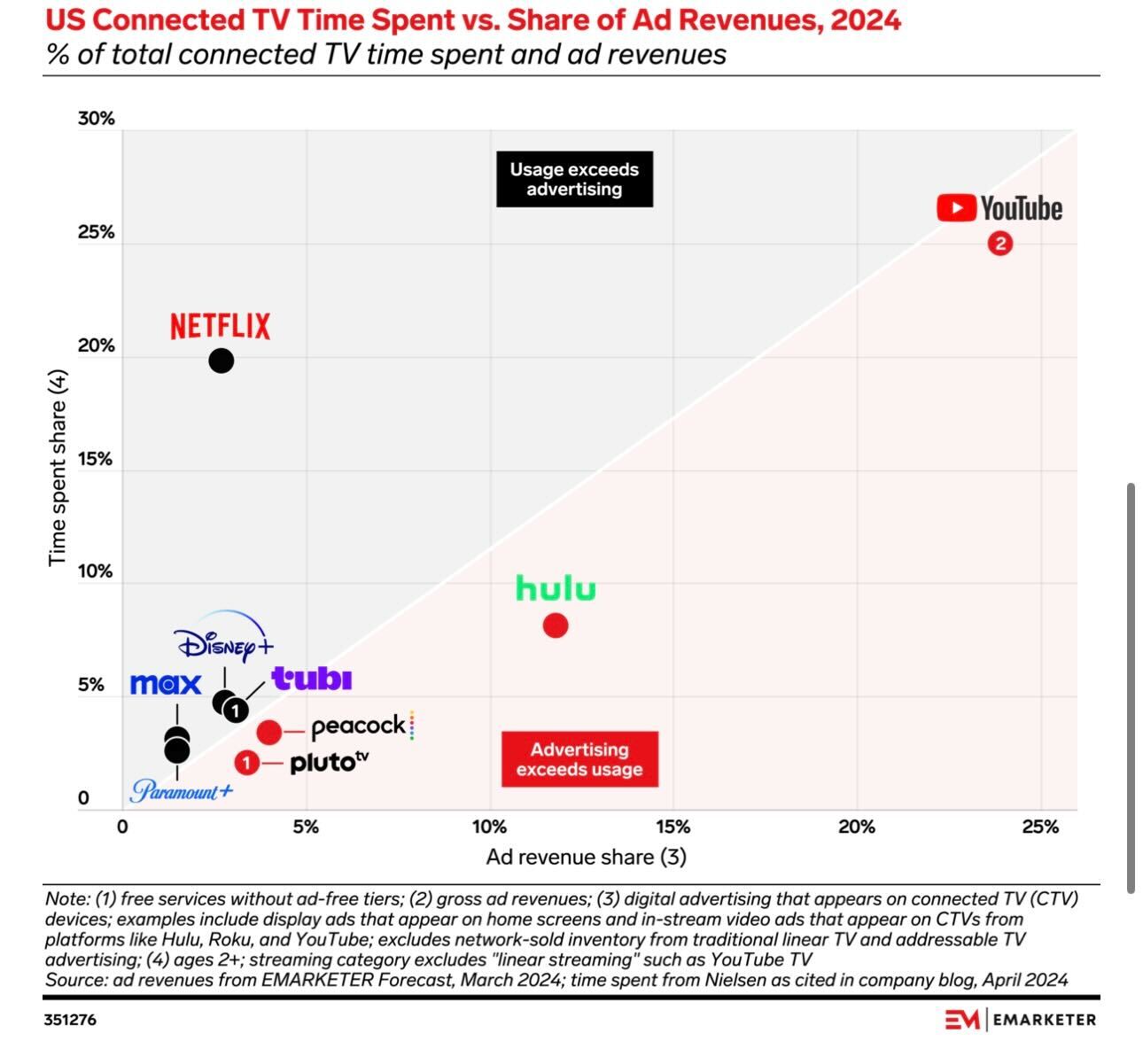

Of course, Netflix executives know it’s a slow build. Peters admitted on an earnings call last year that “ads won’t be a primary driver of revenue in 2025, because we’re still scaling that audience and that inventory faster than our ability to monetize it.” Netflix is trying to speed up that process by developing its own ad tech—similar to the investment made by Disney, YouTube, and NBCUniversal—which should remove some “activation hurdles” for advertisers and thereby increase overall sales. In the meantime, according to a 2024 analysis from eMarketer, Netflix’s share of connected TV time exceeds its share of ad revenues—the opposite is true of Peacock, Hulu, and YouTube—which suggests that the business is just scratching the surface of its potential.

|

|

Advertising is mission critical to Netflix’s next stage of growth, and the company will need to continually ensure that its higher percentage of trade-in customers—that is, tier-switchers among existing subscribers—doesn’t drag down overall revenue. But if those trade-in customers start to represent higher revenue customers, it’s a net win for Netflix across the board.

Netflix doesn’t own the streaming advertising space by any means—Amazon Prime Video leapfrogged Netflix by rolling every Prime Video subscriber into its ad tier as a default, rather than an option—but the company does a better job than others of making its platform, not merely the titles on it, totally necessary. After years of investing heavily in the best algorithmic recommendations, A/B testing user interface strategies, and collecting enormous amounts of user data, Netflix’s tech lead now seems nearly insurmountable, which will facilitate its transition. Too many legacy companies refuse to acknowledge that their content isn’t the sole differentiator. But in an app-ruled world, it’s all about instilling a reason to open it every single day. If they can do that, then they may see their churn rates slow and advertising tiers pick up.

|

|

Thanks, Julia. I’ll be back tomorrow.

Matt

|

|

|

|

Puck founding partner Matt Belloni takes you inside the business of Hollywood, using exclusive reporting and insight to explain the backstories on everything from Marvel movies to the streaming wars.

|

|

|

|

A professional-grade rundown on the business of sports from John Ourand, the industry’s preeminent journalist, covering the leagues, players, agencies, media deals, and the egos fueling it all.

|

|

|

Need help? Review our FAQ page or contact us for assistance. For brand partnerships, email ads@puck.news.

You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with . To stop receiving this newsletter and/or manage all your email preferences, click here.

|

|

Puck is published by Heat Media LLC. 107 Greenwich St, New York, NY 10006

|

|

|

|

_01JXDZEFNY653ZA3DREZT8Z49Z.jpg "The Day Of The Jackal - Peacock")

_01JXDZECH2V994M9YTVPXTD81H.jpg "The Day Of The Jackal - Peacock")