|

| Welcome to What I’m Hearing+, en route back from Beacon, one of my favorite towns in the Hudson Valley and home to an incredible art fair. The only members of our friend group who enjoyed it more were the pups excited to run around a proper backyard and not a Brooklyn apartment.

This week, a close look at the strategic thinking behind Hulu’s real value to Disney, beyond the inevitable headline number.

But first…

- Consolidation Clues: I’m often asked about future consolidation across the streaming industry, and what might inevitably force rivals to cooperate. The latest data point: David Zaslav’s decision to license 12 recent DC films to Netflix, a cash-grab gambit that my partner Matt Belloni shrewdly analyzed in the latest What I’m Hearing. As I mentioned a few weeks ago, Netflix is re-entering its 2013 era with these sorts of savvy licensing plays.

This is simplifying it immensely, but media companies generally consolidate for three reasons: 1) to increase their subscriber base; 2) to acquire complementary programming that can extend the lifetime value of a customer; and 3) to turn a competitive threat into an advantage in the market. Of course, in the past year, since Wall Street signaled that it was more interested in profitability than growth, even the largest companies have begun thinking about these issues differently. Scale will always be important, but efficiency is now paramount, too.

To cite an illustrative hypothetical that also wouldn’t happen for a zillion other reasons, Apple would never acquire HBO from Warner Bros. Discovery for its Apple TV+ service because the audiences overlap too much. Sure, you could increase price, etcetera, but it would be a lot smarter to buy a complementary asset like CBS. (Not saying this would happen either, for a multitude of reasons, but Paramount owner Shari Redstone might at least consider sending banker Aryeh Bourkoff to that meeting.)

For the time being, I expect to see more deals like the one between Warner Discovery and AMC Networks, which saw a number of AMC+ original series stream on Max for a limited time and at no extra cost to Max subscribers. From what I hear, both parties feel the partnership has worked out well. And in a future where certain networks end up becoming pure content suppliers, finding the right distribution partner will be the key to increasing brand power and perceived value.

|

|

| Iger’s Real Hulu Price Tag |

| Now that Disney is finally acquiring the final third of Hulu from Comcast, the overall valuation of the asset—and what Bob Iger ends up paying for it—may be less material than the investment required to maintain it. |

|

|

|

| The quasi-news announcement last week that Disney will fully acquire Hulu—as has been obvious for months—has prompted far more consequential questions about the business. Foremost among them, of course, regards the price that Bob Iger will pay Comcast for the remaining one-third of the asset that Disney doesn’t already own. Surely, Hulu is worth more than the $27.5 billion floor valuation that both parties agreed to in 2019. But how much more?

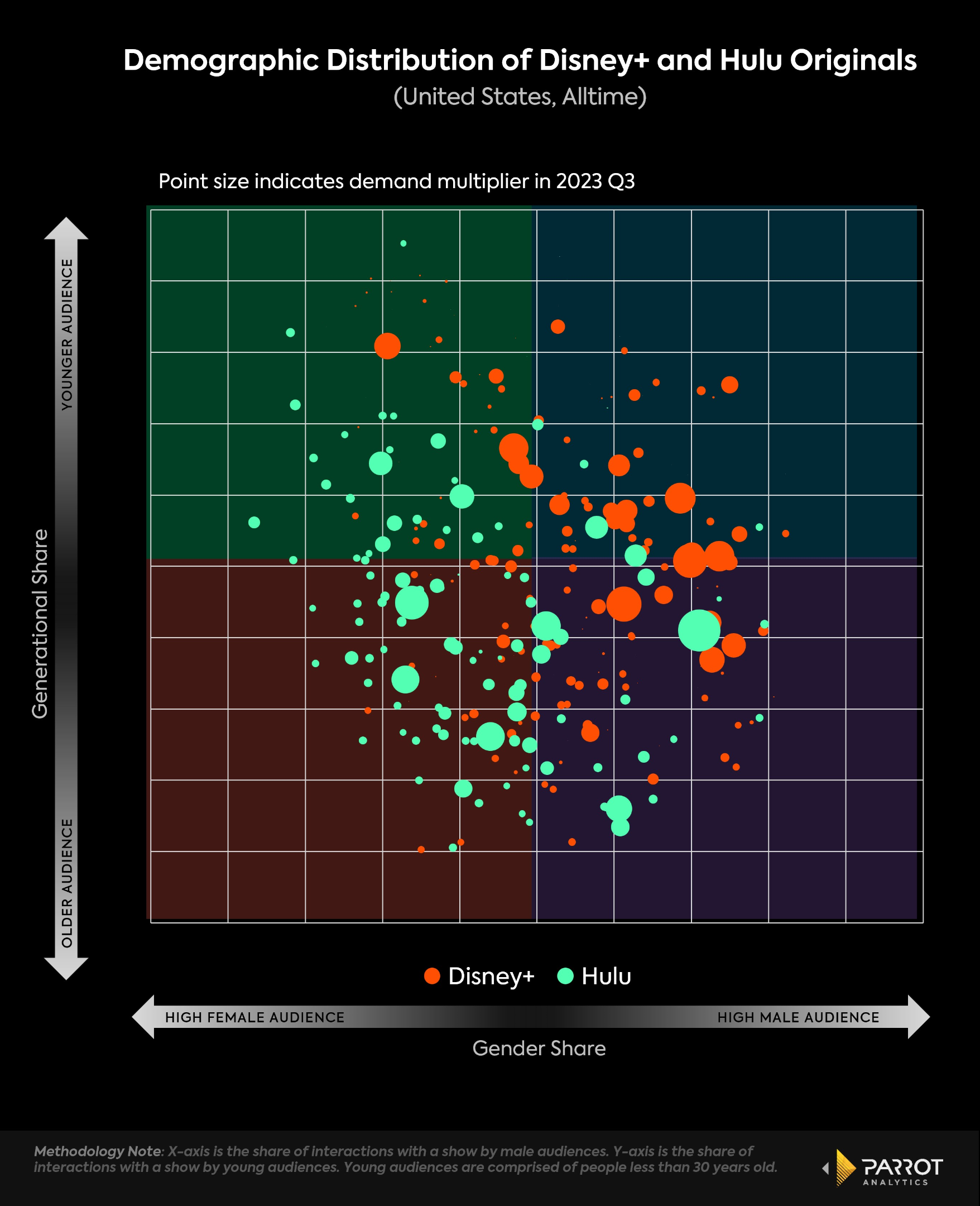

Bankers for Disney and Comcast will have their own formulas, with a third bank set to enter the negotiations if their numbers diverge by more than 10 percent. But I’m interested in the broader and potentially more important question of Hulu’s value to Disney, which faces complex decisions about what to do with the streamer once it’s fully under Iger’s control. We already have some idea of Disney’s plans, like to create a unified Disney+/Hulu app. The combined platform would reach about 90 million subscribers in the U.S., maintaining the largest share of audience attention domestically. Hulu and Disney+ also own 15.2 percent and 9.4 percent, respectively, of catalog demand share (overall share of audience attention for all titles on a platform, including movies and TV series), according to Parrot Analytics. Combined, they would reach nearly one quarter, which leapfrogs Max’s 16 percent.

Increased synergies lie ahead for Disney, but what do those entail? To begin, an expected 20 percent increase in engagement between Disney+ and Hulu subscribers domestically, according to an analysis by Parrot, where I work as director of strategy. Furthermore, integrating key Hulu originals and additional library content into Disney+ could protect around $500 million in at-risk churn revenue. When considering the complementary audience demos of both platforms, the combined entity could yield an additional $750 million in advertising revenue. |

|

|

| Hulu will also support Disney’s advertising ambitions. Nearly 60 percent of new Hulu subscribers this year are on the ad-supported tier, according to research firm Antenna, and Hulu + Live TV is a top six MVPD. Hulu is one of the most frequented services among adults aged 18-34, according to media analyst Evan Shapiro, and it maintains around 3.5 percent of monthly viewership share domestically, according to Nielsen. It has added subscribers each quarter since 2019, and although that growth has slowed immensely in the past few quarters, it still has some of the highest revenue per user of all premium services. Add in a reported $40 CPM for advertisers, and it’s a pretty good business.

In the end, though, both the cost and value of Hulu cannot truly be measured in the acquisition price. The minimum $9 billion that Disney eventually spends to fully own and operate the entity—and some analysts think the final price could be much higher—will likely represent a minority of the investment it will make to maintain the service over the coming years, especially as it competes with a Netflix management team running a near identical strategy with a very different cash position. |

|

|

| In the ever-evolving streaming business, DNA is often destiny. Netflix began as a DVD distributor with the noble mission of replacing the video store, eventually via the Internet. Despite its obsessions with auteurs and expensive showrunners, the platform has always been focused on engaging a broad swath of audience segments, whether via original or licensed fare. (In fact, a recent study from Bloomberg revealed the relatively small role its originals play in audience penetration.) Max, for its part, relaunched this year as a stepchild intended to use HBO’s prestige content and Discovery’s addictive lowbrow fare, along with the levers of licensing, to help service Warner Bros. Discovery’s enormous debt burden.

Hulu started as a linear TV hedge against a streaming future—a useful aggregator to watch last night’s shows. As a result, Hulu was late to follow Netflix and Prime Video into the original content game. The platform has caught up a bit, to be sure—and to great acclaim with The Handmaid’s Tale and Only Murders in the Building, among others—but its original orientation creates a multifaceted challenge for Iger, all coalescing around the reality that Disney needs a steady stream of content to support its D.T.C. ambitions.

First, Disney must continue investing in general entertainment, an area Iger previously dismissed as being “non-differentiated,” with the hopes that a few series will break through the noise. Second, Hulu is reliant on content from Disney brands, some of which Iger famously put up for sale this summer. Content from top Disney studios plus Hulu originals made up just under 40 percent of Hulu demand in Q3, according to Parrot. In time, how will Disney approach content from its linear networks like ABC and Freeform?

Third, there is the Comcast of it all. Once C.E.O. Brian Roberts sells its stake, is there any incentive to continue licensing next-day programming to Hulu? Its NBCUniversal has already pulled back exclusives like Saturday Night Live. There is a monetary benefit in licensing to Hulu, sure, but NBCU needs to bolster Peacock. Not to mention the $9 billion+ that Comcast could invest in content that Disney may no longer be able to bid on, from general entertainment to I.P. to sports rights.

This isn’t a small issue. NBCU’s content recorded the second-largest percentage of demand share for Hulu’s catalog behind the Disney-owned studios in Q3, according to Parrot. And 70 percent of Hulu’s catalog demand comes from broadcast and cable series. Top shows from NBCU include Law & Order: SVU and Will & Grace. Only 13 percent of demand comes from Hulu originals, the second lowest behind Max (11 percent). Peacock sees 75 percent of its total demand come from broadcast and cable series, and NBCU owns the vast majority of those titles.

If NBCU were to pull its series from Hulu, Disney would need to find additional titles to make up for the lack of demand. And it would have to do so after essentially halving its balance sheet to fully acquire Hulu, while Netflix is projecting $6.5 billion in free cash flow and embarking on its own strategy as an aggregator.

Netflix, meanwhile, has returned to its roots as a prolific licensee, and its recent earnings letter touted its still-unrivaled ability to give older catalog content a zeitgeist moment. Other companies, like Warner Bros. Discovery, are happy to license nearly everything and anything to generate revenue—and Netflix has become the default partner. So if Netflix bolsters itself as the core aggregator, at a time when Amazon is looking to become the predominant sports player in streaming, then what is Hulu’s role?

The best thing Hulu can become under Disney is a net. It can catch audiences who are ready to go elsewhere for their next watch but don’t because Hulu is integrated into Disney+ (or vice versa)—they’re willing to check out what’s already open on their screen. I often say that most viewers are lazy, and I always mean it as a compliment. People don’t want to seek out content—especially younger viewers who are being sought out by content on apps like TikTok.

Hulu, as it exists now as a stand-alone app, may be an afterthought because it’s not in a Disney+ user’s direct line of sight. But if an integrated Hulu inside Disney+ can convince more people to stick around for a bit longer each night—or to open the app a few more times throughout the week—then it will have done its job. Is that worth $9 billion? Not immediately. Not even in the short term. But if it creates an extra protective layer in defending against a wave of canceling subscribers looking for their entertainment elsewhere, it’ll set up Disney’s streaming business for long-term success.

Perhaps executives can take a lesson from former WarnerMedia and Hulu C.E.O. Jason Kilar’s playbook and find a way to make Hulu the new collaborative platform for partners looking to license content so Netflix doesn’t emerge the victor… again. We’re in a churn mitigation moment, where every step of the viewing process needs to be easier and more enjoyable. Today, that’s not the case with Hulu and Disney+. In a few months, however, that’s the entire value proposition. |

|

|

|

| FOUR STORIES WE’RE TALKING ABOUT |

|

|

|

|

|

|

|

|

|

Need help? Review our FAQs

page or contact

us for assistance. For brand partnerships, email ads@puck.news.

|

|

You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with . To stop receiving this newsletter and/or manage all your email preferences, click here.

|

|

Puck is published by Heat Media LLC. 227 W 17th St New York, NY 10011.

|

|

|

|