Welcome back to What I’m Hearing+, a very special, post-Disney-earnings edition starring data

analyst Julia Alexander. ESPN’s long-awaited digital platform… the NFL jumping into bed with Disney… and a swan song for the Hulu app—today’s investor call with Bob Iger & Co. produced an unusual amount of streaming news, so Julia is here to break down what it means. Plus an intriguing new YouTube survey, and yet another new streamer launch.

Go for it, Julia…

But first…

|

|

|

|

Julia Alexander |

|

- Say “Howdy” to another

streamer (!!): Almost immediately after Roku announced it will launch a stand-alone, ad-free streaming service for $3 per month, I got a text from a prominent analyst. First, he asked, what’s the deal with that name? (Look, we’re living through a dark era of corporate nomenclature—from Quibi to Fubo to Venu to Versant—but Howdy is particularly appalling.) Second, and more importantly, why is any company launching a new streamer in 2025? Will people really pay for titles like

Mad Max: Fury Road or Weeds, given that the former is on Netflix, and the latter is free on Tubi and Roku’s own Roku Channel?I kinda get what Roku chief Anthony Wood is trying to do: Howdy’s price is low enough to potentially compete with free, ad-supported TV platforms, and it’s comparable to renting a single movie from Apple TV+ or Prime Video. FAST platforms are also one of the, uh, fastest-growing TV segments, per Nielsen, and Roku

may be able to convince some of those subscribers to upgrade to an ad-free experience. My data-informed intuition, however, is that we’ll be waving So long to Howdy in a few years.

- Who’s watching YouTube on TV?: Barb, the U.K. equivalent of Nielsen, has begun tracking viewership of the top 200 YouTube channels on TV sets in the region, and the results are… interesting. Perhaps unsurprisingly, kid-friendly channels dominate the top 20,

which also includes channels operated by traditional entertainment studios, such as Universal and Sony.But very few creators made the cut (or creators that don’t cater to children). MrBeast is on the list, but Jimmy Donaldson reached an average of just 319,000 U.K. viewers per week on TV sets—far below what Donaldson’s YouTube views (3.3 billion in the past 30 days, per Social Blade—but that’s global, obviously) might suggest. It’s a stark reminder that global vanity metrics don’t translate to even local TV–level reach. (Nielsen does not currently release equivalent data for the U.S.)

Anyway, the Barb numbers somewhat undercut the oft-repeated narrative that YouTube is TV—or at least that people are watching YouTube on TV sets. Not great news as YouTube endeavors to bite off a larger share of the global

television advertising pie, even if the majority of Google’s money is coming from its digital ad business.

|

|

|

If Disney can successfully combine Disney+, Hulu, and ESPN into one app

while leaning into bundling, the company’s future may begin to resemble its rich pay TV past.

|

|

|

Among the biggest and least surprising news to emerge from today’s Disney earnings call was that

Hulu—the final third of which was finally acquired from Comcast in June for about $9 billion—will be “fully integrated” into Disney+ in the fall of 2026. The combined platforms will have a total of just under 110 million domestic subscribers, pairing destination programming (Marvel, Star Wars, Pixar) with the lean-back library fare (Family Guy, Bob’s Burgers) that keeps people watching. ESPN, which is launching August 21, will also be accessible inside the app to users paying

for the full bundle ($35.99/month with ads, or $44.99/month without them). For the first time, it’ll all be available under one roof.

Disney has been headed in this direction, of course, especially as streamers have shifted from emphasizing subscriber count to maximizing profitability. Disney+, after all, has been losing altitude for some time. The service didn’t add any new subscribers this quarter, viewership of Marvel and Star Wars properties has mostly declined over the past

five years, and the average number of D+ originals appearing in Nielsen’s weekly top 10 has dropped by more than half since 2021, per the Entertainment Strategy Guy. But Hulu has been on a tear, doubling its appearances in Nielsen’s top 10 over the same period, and growing subscribers every quarter since Disney entered the streaming race. The service now has more

than 51 million domestic subscribers (and more than 55 million including Hulu + Live TV subscribers).

|

|

|

A MESSAGE FROM OUR SPONSOR

|

Outstanding Reality Competition Program

Outstanding

Host For A Reality Or Reality Competition Program – Alan Cumming

“The tone is as delightful as ever… It’s more like immersive theater than reality TV”

|

“Traitors is taking reality competition to stylishly outrageous new levels”

|

For more on The Traitors, visit PeacockFYC.com

|

|

|

Putting the two services together doesn’t create a Netflix killer, obviously, but it does forge a shared

library with enough content to keep people opening the app every day—a key metric as Disney focuses on its premium advertising business. It also allows the parent company to extract the desired synergies. As MoffettNathanson’s Robert Fishman wrote back in July, fully integrating the two companies could save Disney as much as $3 billion by eliminating various redundancies (including many employees, alas).

Even if Disney appears to be managing growth expectations

for the ESPN app, Bristol’s programming is also poised to be a cornerstone of the new super-app strategy. C.E.O. Bob Iger spent most of today’s earnings call discussing ESPN’s NFL deal, which will give it access to RedZone and three additional games. (The NFL will also take a 10 percent stake in ESPN, as my partner John Ourand has long previewed.) But the real unlock for Disney will come in the form of a multilayered bundling strategy. If executed properly, the

combined app should allow Iger & Co. to demand higher premium advertising rates based on increased engagement; improve Disney’s leverage for bundling arrangements with non-Disney-owned streamers; and raise prices without worrying about huge churn.

|

A super app would also allow Disney to provide more content to streaming audiences who are frustrated by the

number of options while simultaneously providing more scale. If increasing engagement and reducing churn are the main reasons to combine apps, then a big part of the underlying financial reasoning is advertising potential. It’s no surprise that in an effort to create a one-touch access point for customers, Disney is also trying to simplify its approach to direct-to-consumer advertising.

More than 60 percent of subscribers to both Disney+ and Hulu are on the ad-supported tier, per Antenna.

Rita Ferro, Disney’s advertising chief, has already sold Disney+ and Hulu spots together, but having one super app would leverage far more efficiencies… and a lot more inventory. Disney can maximize its commercial revenue by collecting more data on customers within a single app, allowing for better targeting and offering advertisers a broader audience to reach. (D+ doesn’t allow ads on content for young children, but let’s see if that policy is relaxed in this YouTube–dominated

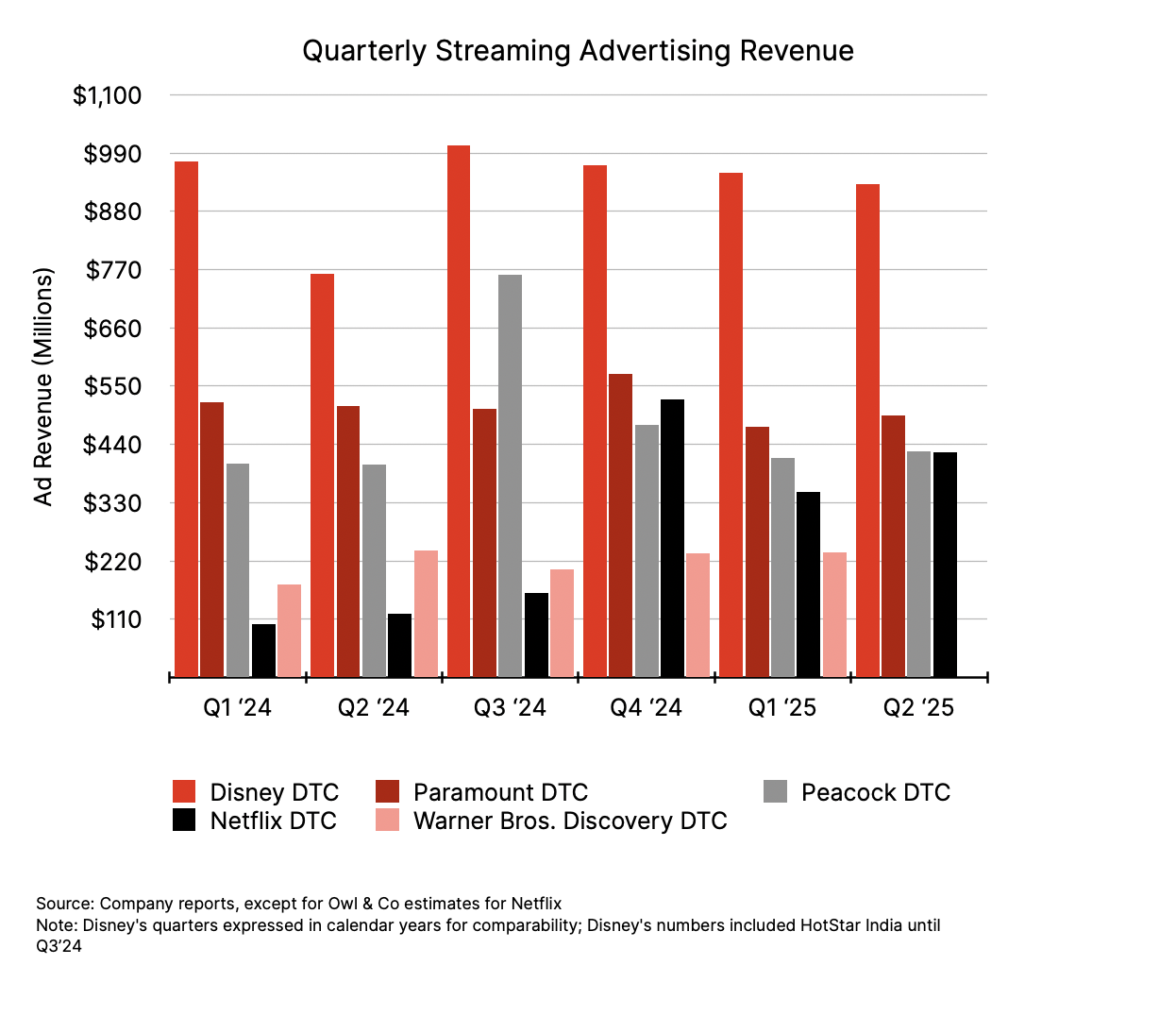

age.) And Ferro may soon be able to bundle ESPN inventory, too. Remember, the casual fan watching Monday Night Football on Disney+ is different from the diehard sports gambler watching via the ESPN app, and both are different from the older viewer watching via a cable subscription. Advertising, as executives have made clear, is the fastest-growing part of the business. ( Owl & Co.’s Hernan Lopez looked at just how strong Disney’s D.T.C. ad business is compared to other

platforms, as seen in the chart below.)

|

Earlier today, Iger boasted about the potential synergies. When the company introduced more Hulu programming

to Disney+, “we saw engagement increasing.” The “full integration” of Hulu, he predicted, would drive up engagement even further. Right now, Disney+ subscribers with the Hulu bundle can engage with Hulu content, but once the Hulu app is sunset, and those subscribers are moved over, it’ll create more than just additive engagement. But Disney has long struggled to improve discovery across platforms—an issue that has been exacerbated by various technological and product design challenges. Think

about how many Disney streaming products there are: D+, Hulu, ESPN+, the forthcoming ESPN app, and eventually Fubo? Having so many destinations is inefficient. Disney needs just the right number of access points to differentiated content. Hulu + Live TV, for example, provides access to content Disney doesn’t own, but Disney collects data. Iger acknowledged that they “also know that it’s still a work in progress, and we have a lot more work to do.” (Disclosure: I previously worked at Disney.)

|

|

|

A MESSAGE FROM OUR SPONSOR

|

Outstanding Reality Competition Program

Outstanding

Host For A Reality Or Reality Competition Program – Alan Cumming

“The tone is as delightful as ever… It’s more like immersive theater than reality TV”

|

“Traitors is taking reality competition to stylishly outrageous new levels”

|

For more on The Traitors, visit PeacockFYC.com

|

|

|

If the super app strategy succeeds, however, Disney should gain more pricing power—i.e., the ability

to introduce additional price increases without worrying about significant churn. Disney+ and Hulu already have below-average churn rates (4 percent) as of June, per Antenna, just behind Netflix (2 percent churn). Not bad. But the easiest way to grow revenue and improve operating margins is with more ad sales and incremental price increases. When Netflix hiked prices earlier this year, churn remained minimal. And even though its engagement in the U.S. also remained mostly stagnant, Netflix is

approaching a 9 percent share of total TV time in the U.S., far ahead of the combined Disney streaming offering. The lesson for Iger: If people feel like they’re getting even more value, they won’t cancel even if you charge more.

|

In any case, it was refreshing to hear Iger acknowledge that much of Disney’s future streaming success will

come from increased bundling—which is code for efficient spending and strategic partnerships in the post-streaming wars era. He confirmed that Disney executives have talked to other companies about bundling sports offerings (R.I.P. Spulu, I mean Venu), but he had nothing to add beyond that. Indeed, as Ourand has reported, Fox, Paramount, and NBCUniversal don’t want their fans watching their content on a platform owned by Disney and ESPN. (Venu, after all, was a joint venture.) Disney

was excited to announce its new deal with the NFL, plus a new WWE pact, but this wasn’t the outcome ESPN chairman Jimmy Pitaro presumably wanted a year ago when he set out on this streaming voyage across ESPN and Venu, and seeking a slate of transformational partnerships.

But this may be a temporary problem. Leverage is everything, and Disney

has proven it can be central to another streamer’s growth. To wit: The Disney+ and HBO Max bundle is working well for both companies. The bundle drove 2.2 million new Disney+ subscribers, per Antenna, and more than a fifth of signups for Max in the fourth quarter of 2024 came from the arrangement. (Disney+ and Hulu saw 14 percent and 15 percent of their new signups come from the bundle, respectively.) Bundling and discounting, among other churn-mitigating tactics, are particularly important as

consumers become more price sensitive. A recent report from Ernst & Young suggests that 68 percent of customers were motivated to sign up for a new platform because of attractive pricing, far more than the 35 percent who were motivated by exclusive content.

Although executives including Comcast’s Brian Roberts and Fox’s Lachlan Murdoch have played down their reliance on streaming as the sole growth driver for their companies, pointing to a more

synergistic strategy that allows streaming to capture different audiences without sacrificing linear viewers, at some point, broadcast and cable audiences will dwindle to the point where streaming has to make up for those lost profits. Everyone has learned that investing too much in streaming isn’t the right way, but that leaves bundling as the only remaining option.

If Disney can bundle its way to holding its own against Netflix and YouTube, it may find itself the envy of even

Ted Sarandos. This is a lofty goal, but if the company’s streaming future is creating a central hub around its core assets and finding partners to bundle with, that future may end up looking something like its lucrative cable past.

|

Thanks, Julia. See everyone tomorrow.

Matt

|

|

|

Need help? Review our FAQ page or contact us for assistance. For brand partnerships, email ads@puck.news.

You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with {{customer.email}}. To stop receiving this newsletter and/or manage all your email preferences, click here.

|

Puck is published by Heat Media LLC. 107 Greenwich St, New York, NY 10006

|

|

|

|