|

|

Greetings from Cannes, France, where I’m speaking at the MIPCOM television conference, and welcome back to What I’m Hearing+, my weekly dispatch focused on the streaming industry and the analytics behind it all. If this email was forwarded to you, click here to subscribe.

Tonight, some observations on Netflix’s surprising earnings report—and why adding an advertising tier will change more than just its revenue model.

But first…

|

|

|

- Peacock’s ‘Halloween’ Bet: NBCUniversal stuck to the day-and-date release strategy for Halloween Ends, and is now touting the film as the most-watched title in a two day period on Peacock. This kind of anecdata is almost useless, but consider that SambaTV reported 1.2 million households tuned into the 2021 installment, Halloween Kills, within its first 48 hours, so we can presume that Ends exceeded that. The performance may have cut into the film’s theatrical box office revenue, which missed expectations by a range of $5-10 million.

That said, it’s still a win for NBCU. At $40 million domestic, Ends is at least a sign the industry is figuring out a hybrid future. It is also a potential lifeline for Peacock, which is struggling to find subscribers but has seen jumps when box office hits, like Jurassic World: Dominion or Minions: The Rise of Gru, are released. Not every movie should go day-and-date (I would argue most shouldn’t, and some movies, like Bros, may find a bigger audience at home), but finding a way to bring people to Peacock without too much theatrical cannibalization is core to growing the next emerging business while also supporting a key current one.

- G4TV’s inevitable demise: Comcast is shutting down G4TV less than a year after re-launching the gaming-centric network, with 45 employees out. Any layoffs are difficult, but frankly, it’s not surprising that consumer demand wasn’t there. G4TV faced a similar battle to what late night is experiencing: in a world dominated by YouTube and Twitch megastars who garner followings by explicitly not being tied to a giant network, trying to make G4 work on linear TV alongside digital channels was a massive challenge. You can’t drive the nostalgia train while hoping that audiences will change their viewing habits and jump on—especially at a network vying for the attention of an incredibly online-first crowd.

|

|

| The New Netflix Age Has Arrived |

| Netflix naysayers suggest that the forthcoming ad-supported tier will cheapen the brand, lead subscribers to downgrade, and lower the ARPU. But it’s actually an opportunity for the company to accelerate its pivot to its own O&O sitcoms, procedurals, and other content that its users already crave and its future ad partners lust over. |

|

|

|

| If the entire streaming video industry has felt jittery of late, that’s in large part because the company that effectively created that very business had hit a rough patch. Yes, Netflix, as you may have heard, has been facing something of an identity crisis ever since Wall Street lost faith in the streamer’s ability to spend its way to infinite growth, causing its stock to sell off by more than 70 percent before beginning to recover. That rebound accelerated with today’s third quarter earnings report—Netflix added 2.4 million new subscribers, although only about 100,000 in the U.S., and grew annual revenue by nearly 6 percent despite macroeconomic conditions—causing the stock to pop some 35 percent after trading hours.

It was a much needed confidence booster (not fantastic, but not terrible) for Netflix after losing close to 1 million subscribers globally in Q2 (more than 1.3 million subs churned in its most profitable region, the U.S. and Canada). It also marks a new attempt to shift the narrative in Hollywood’s streaming landscape. Notably, Netflix informed shareholders that it would stop providing guidance for its number of paid subscribers as Wall Street shifts its attention to revenue. So while total paid memberships will still be reported, Netflix isn’t going to try to guide those expectations. It’s all about revenue now. Or, at least, that’s the idea.

That’s a convenient narrative shift for Netflix, given that it’s one of the few streamers that make real money—$1.4 billion in net profit on nearly $8 billion in revenue last quarter. Indeed, today’s earnings report goes out of the way to note that “all of these competitors are losing money on streaming, with aggregate annual direct operating losses this year alone that could be well in excess of $10 billion.” Makes sense—why set up questions about slow subscriber growth in key markets when direct-to-consumer revenue is the story everyone on Wall Street is chasing, and Netflix has the clear advantage?

Of course, the biggest tectonic shift is still to come. In a few weeks, Netflix will finally launch its new $6.99 advertising-supported tier, providing a lower-cost option for millions of potential customers and opening a potentially lucrative new revenue stream that Netflix had long resisted. Today’s earnings report notes that shareholders shouldn’t expect to see material effects in Q4. But the core innovation here, and the key signal to the Street, is Netflix’s change in mindset, from pursuing exponential growth to a more sustainable P&L.

Sustainability, after all, is the watchword of the New Netflix: sustainable demand for new original content, sustainable subscriber growth, sustainable churn, and sustainable revenue based on a sustainable level of investment. This is the groundwork that Netflix has been trying to lay down this past quarter, ahead of the launch of its new advertising tier. Can they pull it off? Sure, investors are suddenly hopeful again, but there are some legitimate concerns that Netflix needs to address, too, as well as some seriously underappreciated opportunities ahead. |

|

|

| While Netflix likely hasn’t hit its final subscriber ceiling in the U.S. and Canada, future growth will most likely remain incremental at best. A large percentage of those homes (about 80 percent) that want Netflix already have it or engage with its content via piracy, according to Pivotal Research Group. But that still leaves some 6.5 million to 8 million potential new subscribers that Netflix could attract in the UCAN region in 2023 with its hybrid advertising product, according to some analysts. The annual revenue per user from an ad-supported tier could eventually be higher than the ad-free tier, depending on adoption, usage, and advertising CPM. Former Disney Streaming head Kevin Mayer, for example, previously noted that ARPU from Hulu’s ad-supported tier was higher than the ad-free tier when he was overseeing the division. And presumably it’s potentially easier for Netflix to build an ad business atop a stable subscriber business than it has been for traditional ad-supported media companies to enter streaming.

Of course, it remains to be seen whether adoption of Netflix’s ad tier mostly comes from new users, who had been on the fence about subscribing and who Netflix is blatantly targeting, or current users looking to downgrade their monthly fee during a time of increased competition and growing inflation. Netflix’s ad tier could lead to more internal cannibalization, meaning that instead of attracting 10 percent of potential customers in UCAN, current customers could simply downgrade to the ad tier. The company isn’t too concerned about current customers dropping to the ad-tier, Netflix’s C.O.O., Greg Peters, said on the company’s earnings call, arguing that customers on non-ad supported tiers are “sticky” Still, this isn’t an idle concern for Netflix: More than 45 percent of current customers, especially those who are new to the service, or who belong to an older demographic, will at least consider switching to the ad tier, according to a recent survey from SambaTV and HarrisX.

There’s also the current economic headwinds facing advertising itself. Ad spend has grown 8.3 percent so far this year, according to analysts, but that number is expected to drop in 2023 amid a global slowdown (a fun earnings game is to take a shot every time “macroeconomic conditions” gets mentioned). If internal subscriber cannibalization does occur, and advertising spend slows too, that could spell trouble for Netflix over the next year or so. Advertisers and competitors are already raising their eyebrows at $60 per thousand impressions (CPM), according to multiple reports, which would make Netflix one of the most expensive streaming services to advertise on. (Hulu has seen ads run between the $30 and $40 CPM rate, for a direct comparison.) If that happened alongside subscriber cannibalization, it could negatively impact Netflix’s ARPU in the short term without enough subscriber growth occurring organically.

Then there are the non-data points. Some analysts have expressed concerns that ads will cheapen the brand (hmm…) or the product (a more worthwhile concern). Executives at rival companies with ad-supported tiers also wonder whether Netflix is equipped to deal with the concerns from both buyers and customers—it’s not just about ensuring that a commercial placement makes sense, but knowing what advertisers want, and don’t want, and tucking everyone in. Just talk to anyone in media or tech (hello, YouTube) to understand how much this business, not unlike talent management, requires relationships and white-glove treatment. Other questions, including whether ads will impact the type of content being made, have also come up. While there are plenty of red flags that Netflix bears have noted since the first announcement of the company’s plans, there are also some potential breaks to the upside that would increase usage, subscriber retention, and revenue. |

|

|

| Back in 2018, near the peak of its dominance, Netflix finally acknowledged the existence of its so-called “taste clusters”—a sophisticated, data-driven new way of categorizing audience micro-communities. Cluster 290, for example, was reportedly composed of people who liked Black Mirror, Lost, and Groundhog Day—the secret sauce, in other words, fueling Netflix’s content recommendation engine. This theoretically made targeting easier. Series dedicated to reaching those taste clusters could be developed and accelerated into the market.

This strategy is supposedly effective for high-engagement subscribers and high risk churn customers. And given Netflix’s aptitude for identifying target clusters, which are appealing to both consumers and brand partners, it is reasonable to wonder whether Netflix can start to truly succeed in areas that traditional television has thrived. Last summer, Matt Belloni argued persuasively that Netflix was focused, at least in part, on becoming the next CBS. Now it might be closer than ever. Even C.E.O. Ted Sarandos noted on the company’s earnings call that Netflix isn’t just focused on prestige drama series, but creating pop culture entertainment across a variety of genres to appeal to all customers, current and potential.

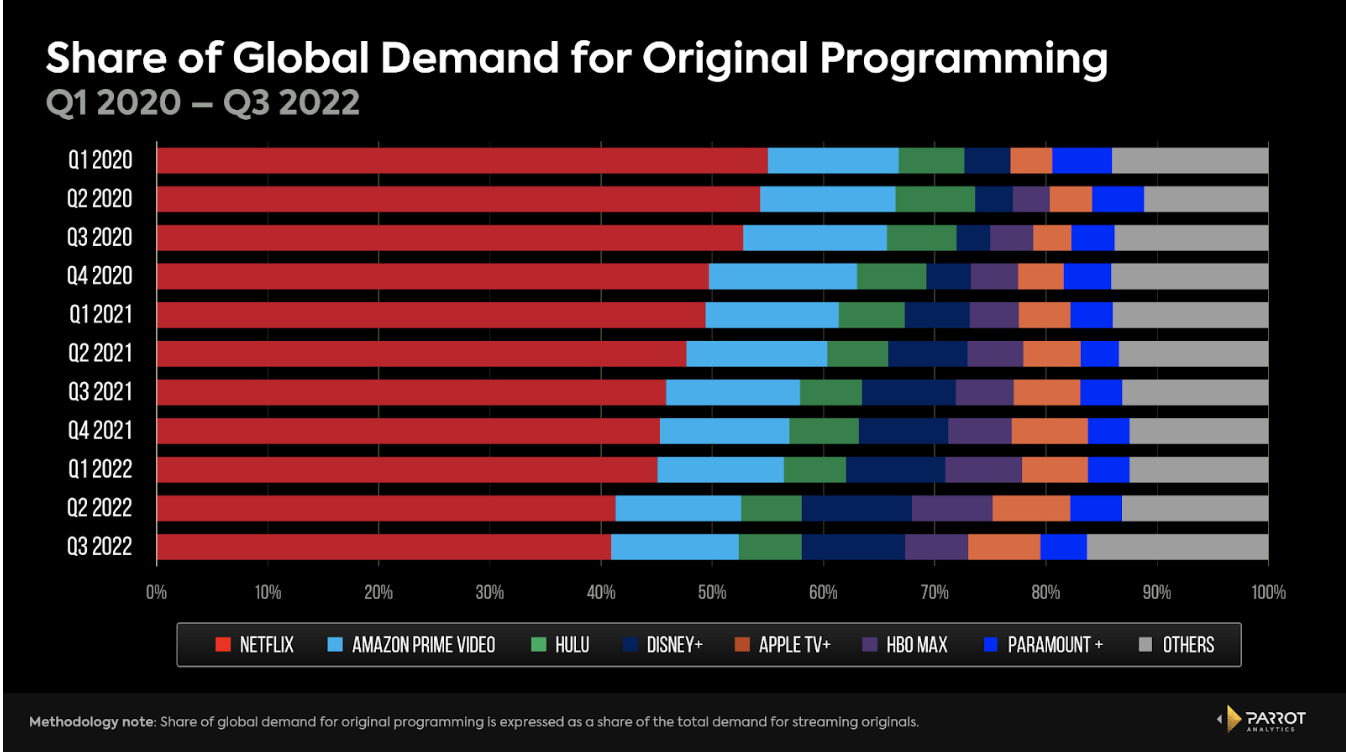

It’s a shift away from a period when Netflix tried to define itself through thoughtful, edgy, expensive originals. But that’s not the strategy that is going to lead to sustainable growth, especially as reports of decreasing return rates from customers begin to emerge. Despite today’s expectations-beating earnings report, the streamer also hit a new record low for the 10th consecutive quarter in global streaming originals demand share, according to Parrot Analytics, where I work as strategy director. Subscriber growth in Latin America has stalled this past year, while Europe and the Middle East has slowed over the last three quarters. It was just one year ago that Netflix led these competitors in global demand share by more than 5 percent; now it’s two points behind. |

|

|

| Sure, Netflix has seen a slight rebound in the U.S. when it comes to that demand market share, which is good, but that’s largely thanks to the incredible success of Stranger Things and Dahmer. Netflix released 1,026 episodes in Q3, according to MoffettNathanson. To compare, Amazon Prime Video released just under 225. For every Stranger Things or Dahmer on Netflix there’s a dozen shows you haven’t heard of getting canceled after one season, and without supportive revenue in the form of advertising (coming soon!), the cost of those shows is unsustainable based on Netflix’s current subscriber churn. |

|

|

| In 2015, New Yorker writer Emily Nussbaum published a piece on the state of advertising in television. She and television creators including Matthew Weiner (Mad Men) and Sam Esmail (Mr. Robot) argued that TV and advertising were two codependent peas in a pod (my langage, not theirs). TV couldn’t exist without ads, and advertisers loved the creativity of television. I would add that it’s because of advertising that certain types of shows still flourish. Procedurals and sitcoms, for example, are broadcast staples. CBS airs a plethora of cop shows with built-in act breaks for ads. The same goes for ABC and sitcoms like Modern Family and Blackish, which could sustain their runs because of the mix of audience demand and advertisers wanting to reach those audiences. It’s easier to argue for spinning out franchises when there are built-in fans and built-in advertiser interest. At the heart of every business-side network conversation are the inevitable questions: “Can I sell this?” and “How long can I sell it?”

Right now, a lot of those network hits are thriving on streaming. One of the most watched shows on Netflix week-after-week in the U.S. was Criminal Minds, according to Nielsen. The show topped Nielsen’s 2021 streaming list (acquired titles). Also on those weekly charts: Grey’s Anatomy, NCIS, and Supernatural. Eventually, these shows will be reclaimed from Netflix by their birth parent media companies, as they build their own streamers. The great weaning is here. Years ago, Bob Iger began pulling Disney content from Netflix as he worked on Disney+. Now everyone else is catching up. Nothing is guaranteed in the new streaming landscape. Criminal Minds left Netflix for a brief period earlier this year, and with a new Criminal Minds series heading to Paramount+, Paramount isn’t going to want to share its top series—even at an inflated cost.

Netflix executives have spoken about not wanting to rely on licensed content as much—in fact, the company just recently surpassed 50 percent originals across its entire U.S. catalog, as I noted last month. But there’s clearly still strong demand for these types of shows: Lucifer (Fox) was a Top 10 in-demand show for Netflix globally in 2021, according to Parrot Analytics data, and Manifest (NBC) became an overnight sensation on the platform. Netflix’s head of drama, Jinny Howe, told Deadline back in August that Netflix is “really, really interested in an NCIS” or a Law and Order: SVU, noting that these are series that “we as fans have loved over the years and would be excited to explore at Netflix.” It helps that those are shows that advertisers love, too. To truly replace the long-running series that subscribers value, after all, Netflix needs time to build out its own slate. Advertising can help keep the company alive during that period. |

|

|

|

| FOUR STORIES WE'RE TALKING ABOUT |

|

| Biden’s Blessing |

| Will Team Biden throw its juice behind a Silicon Valley-inflected outside political group? |

| TEDDY SCHLEIFER & TARA PALMERI |

|

|

| The E.S.G. Era |

| This shareholder proxy season, aggrieved investors are more vociferous than usual. |

| ERIQ GARDNER |

|

|

| Putin’s Waterboy |

| Peter and Julia dissect Musk’s Putin fixation. |

| PETER HAMBY & JULIA IOFFE |

|

|

|

|

|

|

|

|

| You received this message because you signed up to receive emails from Puck

Was this email forwarded to you?

Sign up for Puck here

Sent to

Unsubscribe

Interested in exploring our newsletter offerings?

Manage your preferences

Puck is published by Heat Media LLC

227 W 17th St

New York, NY 10011

For support, just reply to this e-mail

For brand partnerships, email ads@puck.news |

|

|