|

|

Welcome back to Wall Power, where we’ll attempt to put some rigor behind the results of last week’s outwardly disappointing (but possibly auspicious) back-to-back sales. I’m Marion Maneker, and I’ll be your guide.

Last week’s sales were seen as a bellwether event for reasons both geographical and historical. The major global auction centers, of course, are New York, Hong Kong, and London—where Sotheby’s, Christie’s, and Phillips first set up shop nearly 300 years ago. But certainly since Brexit, and maybe even before that, London’s stature as an international sales center has diminished. It’s no longer the gateway to Europe, and much of the art trading on the continent has migrated toward Paris.

Meanwhile, the auction houses have had outposts in Hong Kong since the 1990s, where sales activity steadily increased. After the global financial crisis, a pan-Asian market was firmly established. In recent years, Hong Kong has faced some challenges from Covid and the encroaching Mainland government. Nevertheless, all three auction houses are opening, or have opened, new headquarters in Hong Kong this year—which means they will eventually hold simultaneous sales. When those sales converge remains one of the enduring mysteries of the current market, but clues point to the fall and next spring.

With trading in London and Hong Kong presently in flux, New York’s dominant position as the industry’s capital has been temporarily amplified. Of course, that means last week’s sales will be scrutinized even more than usual. Today, using data provided to me by my friends at LiveArt, I will try to make sense of what happened.

But first…

- It’s all in the day sales: The day sales are the laboratory of the art market where buyers and sellers try out new trends that might expand upward to the evening sales. So far, these sales are telling us that the market hasn’t coalesced around new priorities yet. Of the five day sales, the Sotheby’s Contemporary Day auction had the highest total and the strongest hammer ratio, both with and without withdrawn lots. The sale had an average lot price of $274k, and totaled $78 million. Christie’s Contemporary Day sale totaled $75 million, with an average lot price of $317k. (Its hammer ratio was weaker both with and without withdrawn lots.)

Sotheby’s Modern Day sale performed alright on the top line, with $52 million in sales and an average lot value of $250k—but the hammer ratio was a disappointing .83 without withdrawn lots (.80 with those withdrawn lots included). Phillips’ Day sale was the smallest of the group, with a total of $23 million and an average lot value of $110k. The hammer ratio was also a weak .87, reflecting the quiet market for young primary market artists.

- The discount action: If you look at the top 10 lots by hammer ratio, which is a measure of the depth of bidding for specific lots, we can see that the most intense interest was directed at lots with estimates below $70,000. Navajo artist Emmi Whitehorse had two works bid to multiples of the estimate and were eventually sold for similar low-six-figures prices. The 67-year-old artist had work in this year’s Venice Biennale, where the main curated exhibition, Foreigners Everywhere, focused on Indigenous artists from across the world. Dan Colen’s Mother (Well), from his Disney-inspired series of paintings made in 2018, had the most dynamic bidding—rising to a $165,100 sale price over an estimate of $10,000. The seven other artists on the list range from early 20th century painters André Derain and Ossip Zadkine to the American Surrealist Gerome Kamrowski to Contemporary artists like Robert Rauschenberg, Neil Jenney, and Salvo. Rauschenberg’s Truckstop was the only one of his six offered works that saw strong bidding.

|

|

| Warhol, Basquiat & A $1.4 Billion Question |

| Exactly how rich are the rich feeling these days? Data from the May sales suggest some reasons to be cheerful—$35 million for Warhol, $28 million for Leonora Carrington, $22 million for Joan Mitchell—despite a 50 percent drop in auction house sales. |

|

|

|

| First, the bad news: There are many good reasons to fear that the U.S. elections in November will constrain what is already a frigid art market. Two years ago, of course, New York’s May sales cycle totaled $2.74 billion, with an average price per lot of $1.8 million. But by 2023, after the Covid-era orgy had subsided, the art market began a relentless contraction. This week, the May sales at Bonhams, Christie’s, Phillips, and Sotheby’s totaled $1.39 billion, down around 50 percent in two years. The average lot value was $925k. An additional 47 lots with an estimated value of $74.4 million were withdrawn to protect the lots for future sales.

The good news is that I think we’ve reached the bottom. Part of the complex interaction between market performance and future estimates is that sellers must take into account past performance when consigning. The withdrawn lots don’t show up in the market statistics, but everyone is aware of what didn’t sell and how the lots were priced. These numbers are likely to bring the estimate level down to a place where results can begin to trend upward.

It’s also important to consider the number of works that sell below the estimate level—you know, those situations when the consignor had to make a sacrifice to get cash. This year, more than a third of the lots were sold for compromise prices, and some 40 percent were sold within the estimates. (Only 25 percent were bid above the estimates.) That’s a very high percentage of works that didn’t make the estimate level—but I’ve seen worse. Otherwise, though, the market is pretty close to being in balance and setting itself up for a potential rise some time in the future.

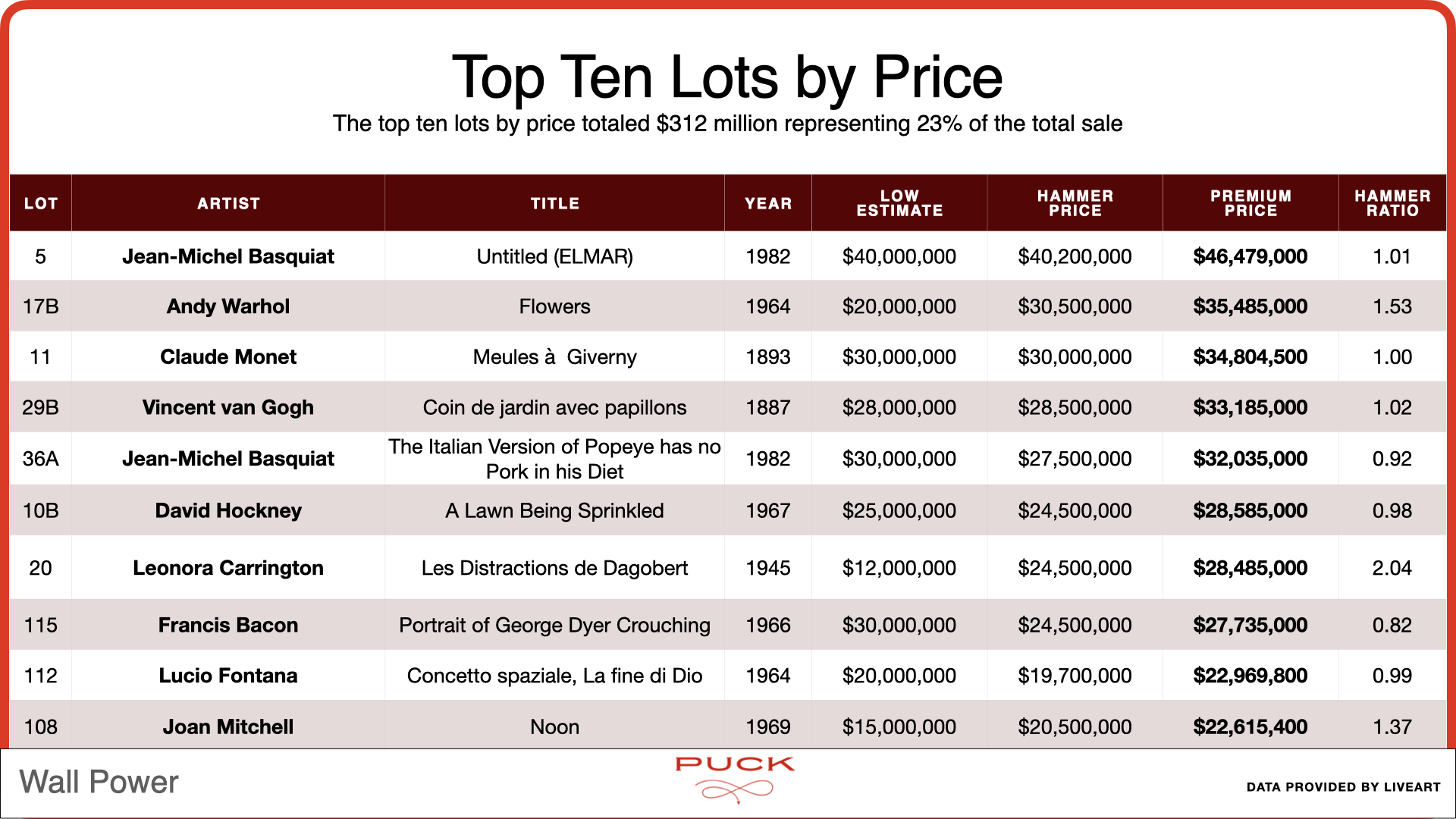

Another reason to be optimistic lies in the performance of the top 10 lots, which made $312 million and accounted for 23 percent of the week’s sales. Works by Jean-Michel Basquiat, Claude Monet, Vincent van Gogh, David Hockney, Francis Bacon, and Lucio Fontana all sold for the estimates or slightly below—a harbinger that the market is well priced. But paintings by Andy Warhol, Leonora Carrington, and Joan Mitchell all saw active bidding above the estimate level, pushing the selling prices into the $20 million range and above. That’s a hopeful leading indicator of room to grow at the top. |

|

|

| The value of the top lots was relatively constrained, representing prices between $22 million and $46 million. Eighty percent of the top lots were estimated between $20 million and $40 million, a narrow scope. Clearly, the big sellers are holding their fire, worried they won’t get good money for their best pieces or their collections. We know there are some estates that did not sell this season who will have to satisfy the taxman in the fall. One auction house executive told me months ago that those estates would wish they had sold this season. This person was assuming the chaos around the election—no matter the outcome—would prove a major distraction.

I’m not sure I agree. The market needs some major no-second-chance works to excite buyers. Trump will be a problem, but the biggest issue in art-buying is: How rich do rich people feel? Art spending tends to be strong when buyers feel like the money they spend will be easily replaced by gains in other markets or the profits they receive from their businesses. So far this year, markets are up significantly, but the enthusiasm hasn’t trickled down. |

| Warhol & Basquiat Questions |

|

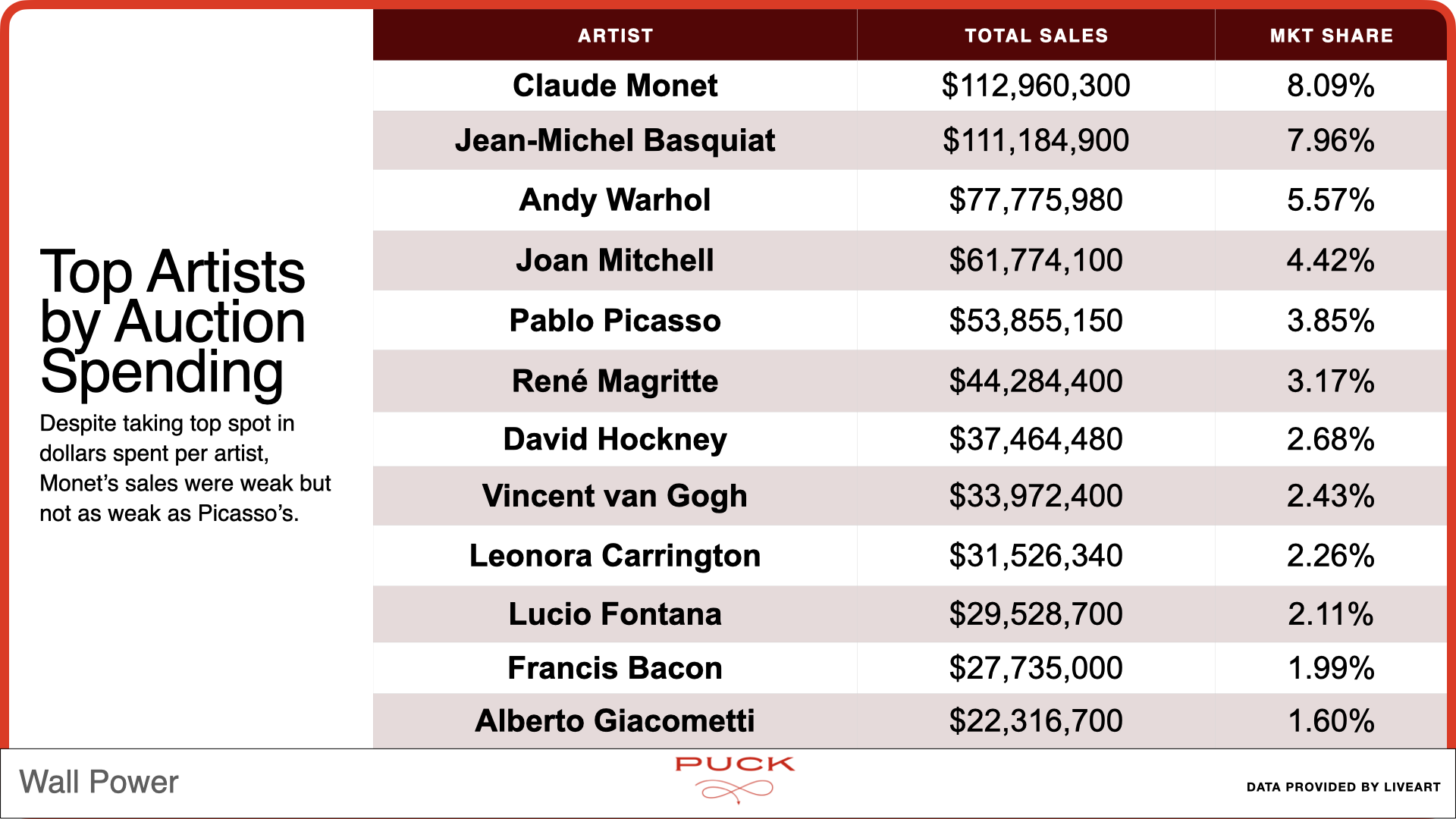

| In some cases, a single work accounts for the vast majority of the spending. It’s not uncommon to see Claude Monet hold the top spot, but the bidding on his works was anemic this year. The aggregate estimate of the 10 Monets on offer was $95.5 million. The hammer price for those 10 lots was $95.65 million, just $150,000 more. Six of the 10 lots were sold for prices below the estimate, and four were sold at prices at or slightly above. Alas, it seems that the majority of the works were overpriced. So let’s not look to Monet to save the future art market.

Basquiat, meanwhile, saw $111 million paid for 11 works. Only two of those works were bid above the estimate levels. Six of the 11 were sold for prices within the estimate range, and three were sold for prices below. One work was bought in and one was withdrawn, but both works were priced at half a million dollars, which is quite cheap for a Basquiat. The Basquiat market has often been quite thin, with a few strong sales but not much depth of demand. That seems to have changed in the last three years as more end users buy the artist’s work. With reports that the record-setting $110 million head painting was resold for $200 million privately, there’s good reason to believe the Basquiat market will continue to play a central role in the overall ecosystem.

Warhol’s work has been absent from the top of the art market for a number of years. The central question about that absence is whether Warhol has become less relevant culturally or if his work has become so valuable, with few owners willing to sell, that the market has gone quiet. Alex Rotter at Christie’s decided to test that proposition this season by securing one of Warhol’s very large, 82-inch square paintings of flowers. The 1964 painting had passed through the hands of several important dealers and collectors, like Leo Castelli, Thomas Ammann, and Frederick Weisman. The painting was purchased in 1990 during a lull in the Warhol market after his death. Estimated at $20 million, an enormous return even at that number, the work was bid above $30 million.

But that was only one of 48 works by Warhol offered in these sales. There was an additional collaboration with Basquiat that sold for a record price of $19.3 million. Four of the 48 were bought in or withdrawn; eight were sold at prices below the estimates; 10 were sold within the estimates, and 16 were bid well above. Almost all of these lots were small 1983 works from a series of paintings inspired by toys. Taken together, Warhol’s hammer ratio for this sales cycle is a very positive 1.19. |

|

|

| Many will cheer seeing Joan Mitchell so high in the market share table, but the truth of the matter is that Mitchell has always been an artist of the first rank in market terms. Even with the strong market share, there was too much Mitchell on the market. A good case can be made that the art advisor who insisted on placing four works by Mitchell from the same collection in Sotheby’s Evening sale may have served their own interests over the longer-term interests of the consignor. Only one Mitchell sold below estimates and one was bought in. The remaining 9 lots sold within the estimates (six) or above the estimate range (three). The overall hammer ratio was .96, suggesting the market has been suppressed by too many works on offer. Nevertheless, three Mitchells have sold for more than $20 million in the last six months. That’s a new price level for the artist.

Normally a mainstay of the Modern market, there was little work by Pablo Picasso on offer last week that could be considered high-quality material. Of the 32 works offered, 28 sold. Sixteen of those works sold below the estimates, for an overall hammer ratio of .65—shocking for Picasso. One sales cycle is hardly determinative to a market as immense and important as the Picasso market, but this is the first time I can recall seeing such weak results for the artist.

René Magritte continues his new role as a market bulwark. A dozen works by the artist were sold, with a third getting bid above estimates and only two works selling below the estimate level. The overall hammer ratio for the artists was 1.16, suggesting continuing strength, even if few major works were on offer and the highest price achieved was just above $18 million. There’s no direct causal relationship, but it seems hard to believe that the Mexican and female Surrealists who performed so well this season would be seeing the same market prominence without the broader success of Magritte for the last several years. |

|

|

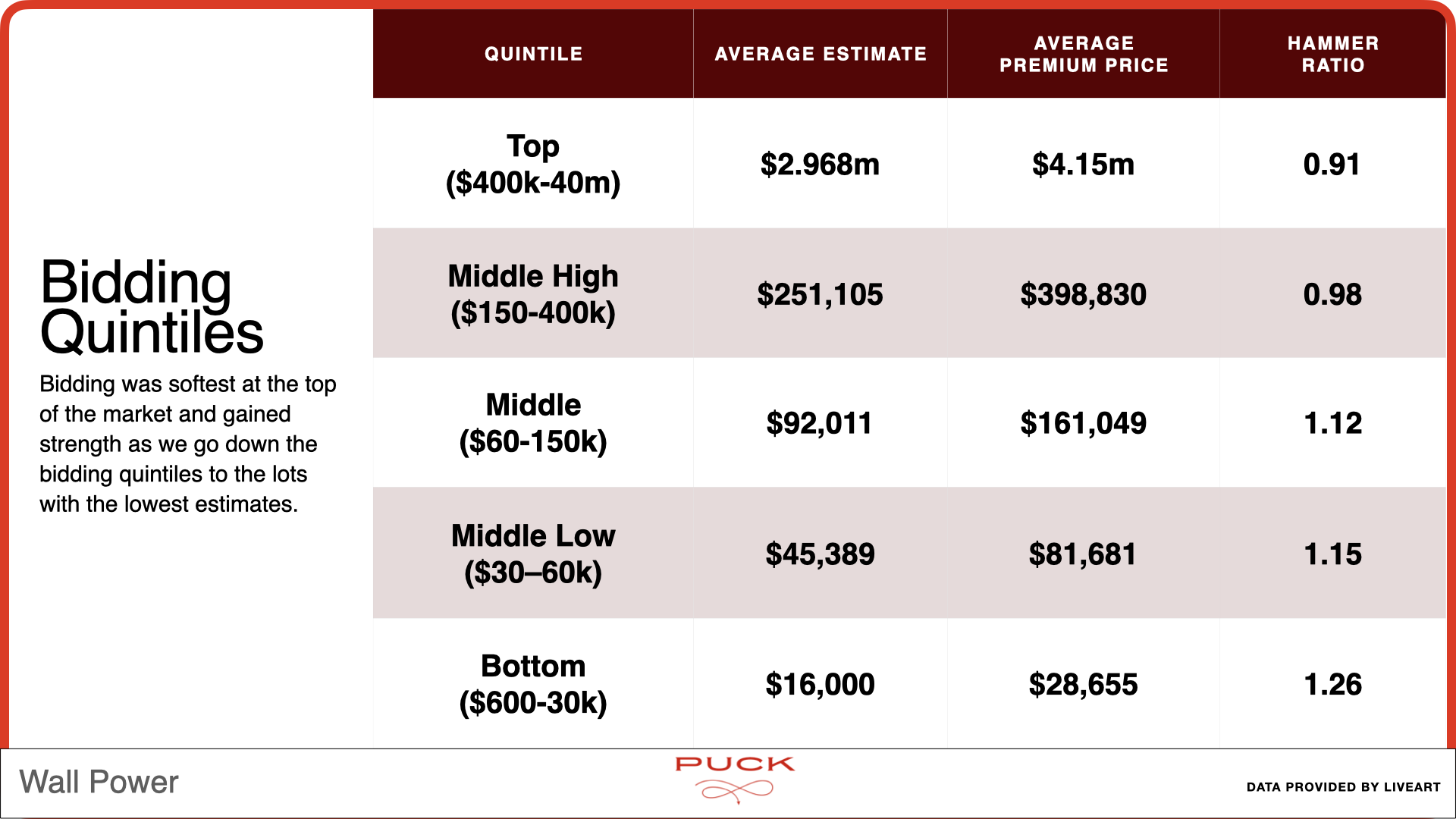

| One of the hardest questions to answer in the art market is where buyers are most active. I’ve written on a number of occasions that we have been in a value-seeking market since the beginning of 2023. This table of the bidding quintiles supports that thesis. What I’ve done here is taken all 1,858 lots offered this season, including withdrawn lots, and arranged them from highest to lowest. Then I divided those lots into quintiles. You can see that the top quintile of works, estimated between $40 million and $400,000 with an average estimate of just under $3 million, had a hammer ratio of .91. The works that sold in that quintile had an average premium price of just more than $4 million. So that market is weak. |

|

|

| The next quintile comprises classic, middle-market works valued between $400,000 and $150,000. These are established works by artists with proven markets mostly. The average estimate was a quarter of a million dollars and the hammer ratio was just under par. The works that sold had an average premium price of nearly $400,000.

In the middle are works priced at $60,000 to $150,000. These lots can have more risk involved. They had an average estimate of $92,011 and a hammer ratio of 1.12, which is solid. Buying one of these works meant spending an average of $161,049.

Taking a further step down, the market gets surprisingly stronger with works estimated between $30,000 and $60,000, which are selling at a 1.15 hammer ratio. You’ll spend, on average, $81,681 to buy these works. Finally, the lowest tier of works, from $30,000 to a mere $600, with an average estimate of $16,000 are red-hot, with a 1.26 hammer ratio. These works will cost $28,655, on average.

In real-world terms, this means art advisors, dealers, and collectors are willing to bid more for cheaper, more speculative works (or simply art works that end users will want to own and, presumably, cherish) than they want to shell out for art work they believe to be fully priced. And that’s the reason I’m positive on the market. The numbers are coming down, but buyers haven’t abandoned the market. They’ve just shifted to a different sector of the market where that money is, frankly, less visible. A passion for art remains, but it is a more sober and restrained passion—and that’s a good thing. |

|

|

|

| FOUR STORIES WE’RE TALKING ABOUT |

|

| Khan’s Fashion War |

| Will the F.T.C throw a monkey wrench in the Tapestry-Capri merger? |

| ERIQ GARDNER |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Need help? Review our FAQs

page or contact

us for assistance. For brand partnerships, email ads@puck.news.

|

|

You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with . To stop receiving this newsletter and/or manage all your email preferences, click here.

|

|

Puck is published by Heat Media LLC. 227 W 17th St New York, NY 10011.

|

|

|

|