|

|

Welcome back to Wall Power, your twice-weekly analysis of the art market. I’m Marion Maneker.

Last week in New York, more than $1.3 billion in art changed hands at Bonhams, Christie’s, Phillips, and Sotheby’s. More to the point, reference prices were set for hundreds of artists—figures the art market will use to guide private sales over the next six months, until we do this all over again in May.

Before we get into the nitty-gritty of the market data and auction anecdotes, my topline take is that it’s now clear we bottomed out in May. Even though the November sales are 5 percent lower in total volume, data from ARTDAI and Christie’s suggest that the market is improving. Estimates are down to the level that makes works attractive to buyers. I’ll get into the details below.

But first…

- A.I. comes to Art Basel: This morning, Art Basel announced its rebooted Microsoft A.I.-powered app, which you can download now, just in time for its Miami fair. The two big new features are Art Basel Companion, which “offers personalized recommendations about where to go and what to see at the show based on user preferences,” according to the fair’s release, and Art Basel Lens, which allows users to scan art works to learn more about the artist and gallery. Art Basel Lens is being launched as a pilot in the Nova (emerging art) and Survey (rediscovered historical work) sections of the fair.

There are some commercial applications here, too. Under the proprietorship of James Murdoch, Art Basel has a skybox strategy where they’re hoping to maximize the value of their most elite clientele. The new app will allow the fair to sell “exclusive partner benefits” for V.I.P.s within the app environment.

Anyway, I haven’t tried the app yet, but the A.I. is being trained only on data that Art Basel already uses for its website and existing applications. In other words, if you point the app at a painting in the Nova or Survey sections, you’ll get some information on the painting and gallery, but it won’t be very different from what the gallery will provide you in person—and conversation, after all, is the reason you go to an art fair. My advice is to ask for help at the gallery.

|

|

|

- Lower estimates lead to higher prices: Before the auctions last week, I told you that the new art market calculus revolves around lowering estimates in order to get higher prices. Remember, the art market has a psychology of mistrust, and it is often easier to pay more if you see that others are willing to fork over close to the same price. A perfect illustration of this phenomenon emerged during Christie’s various-owners sale of modern art. A small work on paper by Pablo Picasso, estimated at $1 million, came up for sale almost unnoticed. Suddenly, a volley of bids flew across the sale room. I was counting bidders, including Larry Gagosian at $2 million, vying for the work, which hammered at $2.2 million. The buyer paid $2.7 million with fees.

My WhatsApp blew up as the auctioneer wrote down the winner’s paddle number. A European collector commented, “This Picasso has been on the market for years asking $2.5 million.” Now, nine bidders wanted it. “Shows you what a low estimate can do.”

- Prices don’t have to go down to fall behind: Several important artists have seen their markets slow to a crawl. For collectors of a certain age, Cy Twombly is a must-have artist. The right work, like this one at Sotheby’s, can still sell for nearly $4 million, but his market peaked about a decade ago. That doesn’t mean collectors cannot sell the work, but sometimes the work just keeps selling at the same price.

Twombly’s Crimes of Passion I, from 1960, which was once owned by the noted German collector Erich Marx, is a good example. The piece was first auctioned a dozen years ago for $5.8 million at Sotheby’s. Three years later, it sold for nearly $6.2 million. At Phillips last week, it sold for $6.1 million. That’s the same work selling at nearly the same price this season as nine and 12 years ago. Auction house fees eat away at the value, but so does inflation.

- About that Koons comeback…: One of the most interesting developments this season has been the number of early Jeff Koons works on offer. The gambit made sense: The market needs leadership, and price growth usually comes from historically important, recognized artists. Koons fits the bill, of course, but the results have been mixed. And it isn’t quite clear if that was a function of the sequencing and tactics or the reality of an indifferent market.

The first work to sell was Two Ball Total Equilibrium Tank, from 1985, which made a little more than $3.5 million—way short of the $4 million estimate, even with the fees added. The work, which was one of an edition of two, was bought in 1995. So the consignor still made plenty of money. That is some consolation, because the other work in the edition was sold a decade ago for nearly $6.9 million.

The next work offered may have been the tactical mistake. Sotheby’s had guaranteed Woman in Tub, from the Barbier-Mueller estate, with a $10 million estimate—a number that may have been determined by the work’s provenance. In retrospect, $6 million would have been more attractive and gotten the bidding close enough to cover the guarantee. It’s also not clear if the house did not want an irrevocable bid, or just couldn’t find a backer. In the end, no one bid. (I’d be surprised if Sotheby’s didn’t sell the work privately, afterward—but they probably took a loss.) This was as much a disappointment for the Koons market as it was for Sotheby’s.

The next night, at Christie’s, Koons’ historically important New Hoover Celebrity IV…, from 1985, estimated at $3.5 million, sold for $5.1 million with fees. Another edition of the same work sold for $6.4 million in 2017. It’s not the kind of piece that’s easy to display in a collector’s home, so that’s got to count as a win. Large Vase of Flowers, estimated at $6 million, was bid to a $6.8 million hammer, or $8.2 million with fees. Another example from this edition sold for $5.6 million in 2009. Taken together, this isn’t entirely bad news for the Koons market. It's a sign that there are buyers, and they will pay for the right works—if they’re offered at the right price.

|

| Now, let’s get into the data for last week… |

|

| Ken Griffin’s Magritte & Other Auction War Stories |

| There were heroes amid the $1.3 billion in sales during last week’s New York auctions, and a couple humbling moments, too. But a closer inspection reveals something less flashy: steady, systematic gains for an art market that’s finally recovering from its post-pandemic malaise. |

|

|

|

| The Trump Bump will have to wait. Right now, the art market is in no position to capitalize on any presumed election euphoria among the rich. Indeed, much of the commentary around town during last week’s November sales, especially from the Europeans, was tinged with gallows humor about the positive impact of the election on the art market… eventually. After all, I don’t think anyone believes that Ken Griffin, an uneasy Trump supporter, bought Mica Ertegun’s Magritte for $121 million because the president-elect was heading back to Washington.

The art market does respond to macroeconomic factors, but it takes a while. Art buyers usually spend money they’ve already earned, six months to a year ago (and then some), not gains they anticipate in a coming financial climate. Pandemic liquidity injected into the economy in 2020, for instance, showed up in the art market in late 2021 and 2022. Indeed, the down cycle we’ve experienced since early 2023 stems from the aftershocks of this post-ZIRP, inflation-taming micro-economy.

It also comes down to changing tastes. Beginning in 2018 and cresting after the upheavals of 2020, there was a wave of interest in identity artists—first figurative painters, later abstract artists—that has run its course. The end of this era doesn’t mean those painters won’t last. Rather, the marginal buyers of these works have either already acquired them or no longer feel they’re missing out. |

|

|

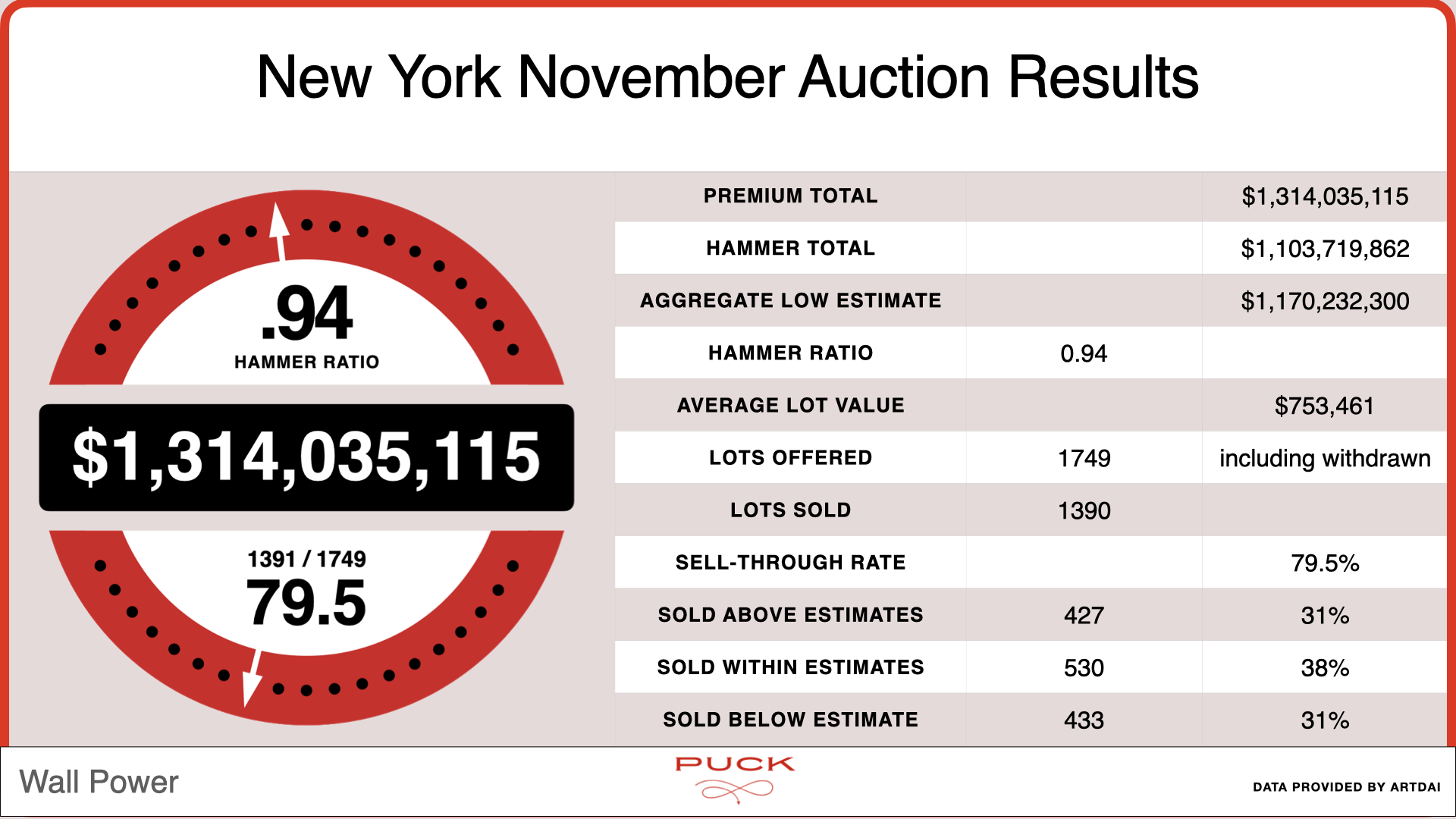

| The market’s current challenge is to rebuild momentum. According to data from ARTDAI, the total amount of money spent this season was just over $1.3 billion. There were 1,749 lots offered and 1,390 sold, a sell-through rate of 79.5 percent. That’s slightly below the industry average of around 82 percent for the entire year. The hammer ratio, which is the aggregate hammer price of all lots divided by the aggregate low estimate, was a weak .94.

And while headline numbers for the November sales might not look strong, the internal dynamics are quite positive. For instance, 31 percent of the lots sold for prices above the estimate range, 38 percent sold within estimates, and another 31 percent sold at prices below the estimate level. That’s a pretty balanced market.

Looking at these same metrics, but switching from the number of lots to percentage of value, it gets more interesting and more positive. Only 21 percent of the value was sold for prices above the estimates, 51 percent of the value was sold within estimates, and 28 percent of the value went at a price below the estimate. A year ago, by comparison, nearly 51 percent of the value sold below the estimate. In May, that number had fallen to just under 40 percent. Now, it’s less than 30 percent. |

|

|

|

|

| Switching to the top lots by price and hammer ratio, we can see the beginnings of a “masterpiece market.” That’s when buyers, who are agnostic about the economic cycle, respond to works that are perceived to be the best of the best. Ertegun’s Magritte was universally acclaimed as one such work. Ed Ruscha’s Standard Station was another, as was the Monet waterlilies that sold for a strong price. Had the work been signed and in pristine condition, it would have sold for a price much closer to the Magritte.

Christie’s tried to address the dearth of masterpieces coming to market by creating a value proposition around works on paper by big names like Basquiat and Lichtenstein. It didn’t quite work out. The Basquiat was bought at just below the $20 million estimate by Jose Mugrabi, who came out for the evening sale. It was interesting to see him bid on—and win—Peter Brant’s consignment. Brant and Mugrabi have done a lot of business together over the years. And this isn’t the first time we’ve seen one defend an artist’s market against the other. |

|

|

| Turning to works with the highest hammer ratio, a record price of $864,000 was set for Gertrude Abercrombie, on a work estimated at a mere $100,000, at Bonhams. Abercrombie is one of a group of female surrealist painters whose work has become increasingly valuable in recent years. At Sotheby’s, three of her works, all quite small, were sold for huge prices, ranging from $192,000 to $264,000. The remaining works on the list of lots with the most dynamic bidding were all estimated at $20,000 or below. The art market continues to trawl through the day sales for historic works that are perceived to be undervalued. This season, John Ritchie, Emilio Baz Viaud, Raymond Barker, Herbert Bayer, Judith Rothschild, Alfredo Castañeda, Emmanuel Mané-Katz, and John Opper were all in the spotlight.

The top artists by market share were a familiar group in an unfamiliar order. Magritte was by far the most appealing artist, with more than 13 percent of the dollars spent going to work by the Belgian surrealist. Ruscha was second, with 7.5 percent. The former market leaders, Claude Monet and Pablo Picasso, slid to third and fourth position. Alberto Giacometti and David Hockney followed. Roy Lichtenstein posted a strong showing with nearly 3 percent of spending. Basquiat came in just behind him. Joan Mitchell, François-Xavier Lalanne, Willem de Kooning, and Wassily Kandinsky rounded out the top 12. |

|

|

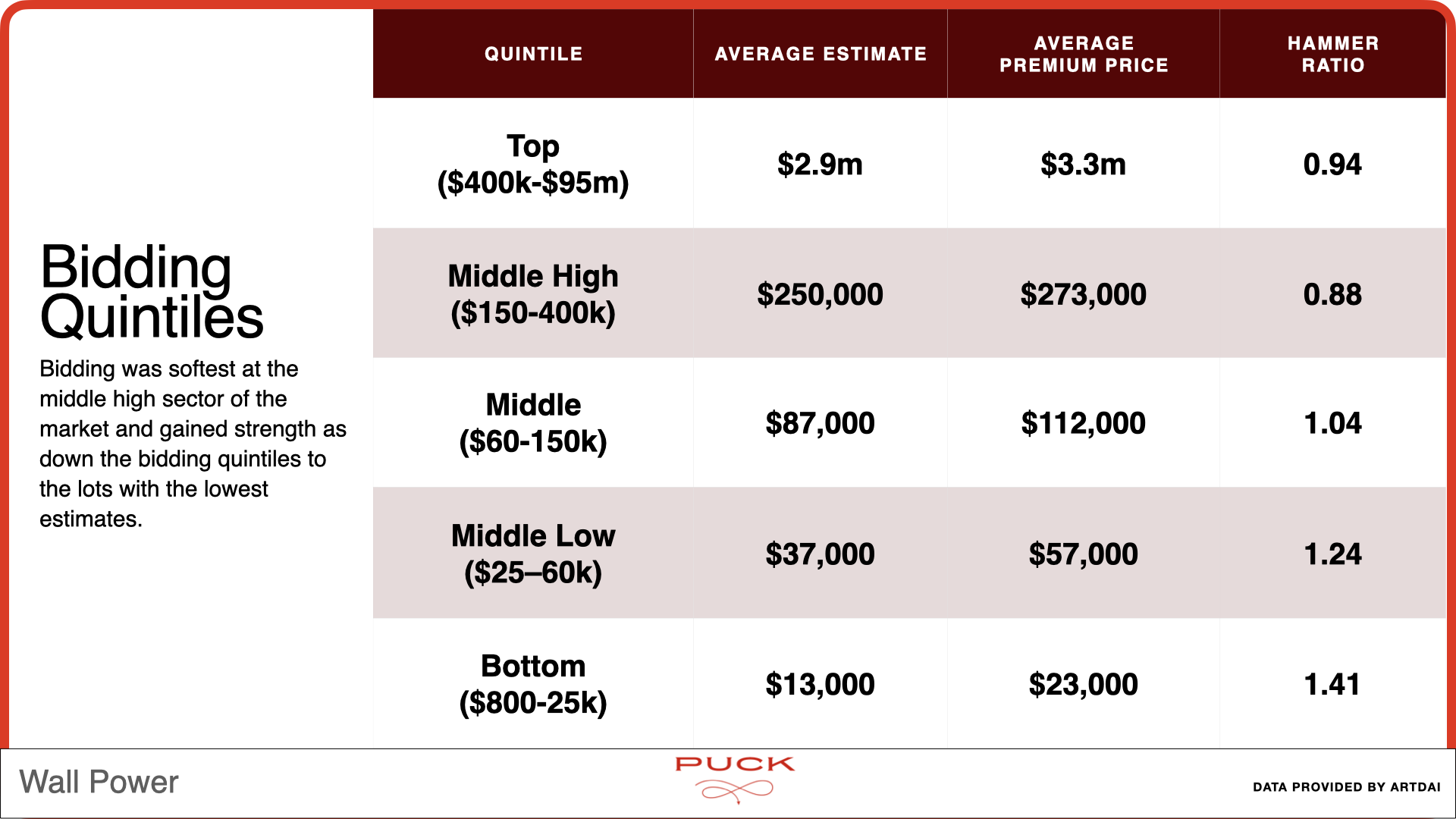

| Finally, and perhaps most importantly, the bidding quintiles show that the very top of the market is regaining some dynamism. Works estimated from $400,000 to $95 million had a hammer ratio of .94. Their average estimate was $2.9 million, and the average premium price was $3.3 million. So, if you’re in the market for a work of art in the low millions, expect to face some competition. In the $150,000–$400,000 estimate range, works were easier to come by. The hammer ratio was a weak .88, and the average estimate was $250,000 against a selling price averaging $273,000. So if you knew what you were doing and could recognize good value, there wasn’t much bidding against you in this price range.

Lower down, things got much more competitive. The middle bracket of estimates, from $60,000 to $150,000, had a positive hammer ratio of 1.04. The average estimate in this range was $87,000, and the average work sold for $112,000. In the middle-low price bracket, with estimates of $25,000 to $60,000, the hammer ratio was higher, at 1.24, which is quite competitive. The average work was estimated at $37,000 and sold at an average price of $57,000. The bottom quintile saw the most bidding, with works estimated from $800 to $25,000 seeing a blistering 1.41 hammer ratio. That means the average work estimated at $13,000 was likely to sell for an average price of $23,000. Don’t let anyone tell you these buyers are “bottom feeders.” They are the health and vibrancy of the art market, proof that there’s still plenty of appetite out there. |

|

|

| That’s enough for today. I hope I’ve demonstrated that the overall health of the market is pretty robust, even if the big numbers are not there yet. In fact, these sales represent the first step toward the return of those big numbers.

I’ve got at least one more really good story from last week to share with you. I’m hoping we’ll have the right place for it next week. In the meantime, enjoy your Thanksgiving (for those of you in the United States, at least).

I’ll speak to you Sunday as we all prepare for Miami.

Yours,

M |

|

|

|

| FOUR STORIES WE’RE TALKING ABOUT |

|

|

|

| Elon’s Overreach |

| Plus, uncovering Boris Epshteyn’s impact on Trumpworld. |

| TARA PALMERI |

|

|

|

|

|

|

|

|

|

|

|

|

|

Need help? Review our FAQs

page or contact

us for assistance. For brand partnerships, email ads@puck.news.

|

|

You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with . To stop receiving this newsletter and/or manage all your email preferences, click here.

|

|

Puck is published by Heat Media LLC. 227 W 17th St New York, NY 10011.

|

|

|

|