|

|

Welcome back to a sweltering Wall Power, where we’re hunkered down at the pool to take stock of the last six months of the art market. Thankfully, our friends at ARTDAI were kind enough to run the numbers for us.

It’s no secret that 2024, at least thus far, has been one of the quieter years in recent memory. But the data suggests that we’re not seeing the worst market performance in a non-crisis year. More on all that below the fold.

But first…

- Christie’s 1H decline: Christie’s announced Tuesday during their regular semi-annual press call that the auction house had sold $2.1 billion in art in the first half of the year, down from $2.7 billion last year. But the sell-through rate remained very strong, with 87 percent of lots finding buyers, the same as last year. The overall hammer ratio, which measures the aggregate presale estimate of all lots against the total hammer price of those lots, rose from 1.07 last year to 1.11 this year. And 82 percent of the bids were placed online.

C.E.O. Guillaume Cerutti, who characterized those numbers as “resilient,” predicted that the art market will soon see a rebound to higher volume, either later this year or in 2025. Some important collections currently making the rounds—Mica Ertegun and Lily Safra are recently deceased collectors that come to mind—will need to be sold soon, depending on the guarantee and the seller’s market confidence.

Christie’s first-half numbers don’t include private sales, which the auction house only reports at the end of the year. But the house did break out auction sales per category: $1.3 billion came in 20th and 21st century art; $362 million in luxury; $217 million in Asian and World art; $132 million in so-called Classics; and $77 million in Old Masters. Notably, Asian/World art and Classics both saw double-digit gains in auction volume.

- Sotheby’s brings in $2.3 billion: Sotheby’s isn’t releasing half-year numbers, but I’m told the auction house was able to generate $2.3 billion in gross sales in the first six months of the year, including their classic car and real estate divisions (not to be confused with Sotheby’s International Realty, which is licensed to real estate conglomerate Anywhere). Since Christie’s doesn’t compete in either market, the figures are not direct comparisons. Sotheby’s total was down a similar percentage to Christie’s, too.

- A collectibles boom: Meanwhile, there’s no recession at Heritage Auctions, the Dallas-based collectibles powerhouse that’s often overlooked by the international media. It grossed $925 million in auction sales for the first half of 2024. Founded nearly 50 years ago as a coin auctioneer, the privately held Heritage generated $1.76 billion in sales in 2023, coming primarily from comics and comic art, popular culture and entertainment pieces, sports relics, and rare coin auctions. Assuming there’s no major setback in the collectibles market, Heritage, anticipates record sales for the fourth year in a row.

Heritage, with 1.75 million registered “bidder-members,” claims the highest online traffic and dollar volume of any auction house—the result of innovations such as creating grading agencies for coins and comic books and accepting pre-bids on auction lots. (Sotheby’s now deploys this tactic with some of its Day sales.)

The house’s escalating results also raise interesting counterarguments about the broader cultural property sector. The art market, after all, has been relatively stagnant in terms of spending volume over recent years in nominal terms, and declining when inflation is factored in. So the migration of money from fine art to collectibles provides an interesting window into future growth. What’s relevant to the next generation of buyers? Is art—in many ways the last redoubt of high culture—losing its relevance and appeal, even to the 1-percent? “Much has been made in the media about a slowdown in the auction world,” Heritage C.E.O. and co-chairman Steve Ivy said in the company’s release, “which has been news to us at Heritage.”

- More than just a summer gallery extension: The Campus, a collaborative art space co-owned by five partners who have six galleries between them, opened this spring in Columbia County, New York, to a great press reception, eager to play up the addition of a new summer art destination and the idea of a group of gallerists collaborating. “I always longed for community among my peers,” said James Cohan, one of the five partners and the co-founder of the VIP Art Fair, an adventure in the earliest days of online art selling. “I didn’t find it in Chelsea, but found that in Tribeca,” where the narrow streets keep galleries in closer proximity. Now, he’s re-created that feeling in the Hudson Valley.

A partnership between Cohan’s gallery, Andrew Kreps, Anton Kern, Bortolami, Kaufmann Repetto, and Kurimanzutto, The Campus has its own curator, Timo Keppler, who will organize an annual show forefronting the artists from the various gallery stables over the galleries who represent them. “It shows how big and diverse the art world is,” Cohan told me, “that we do business with very different people.” That sense of overlapping interest without internal competition extends beyond the goal of having a common, off-the-grid exhibition venue. The Campus is housed in a decommissioned school just outside boho-chic Hudson, some 120 miles north of New York City. When Kreps discovered the school during the pandemic, he was particularly intrigued by the 26,000 square feet of climate-controlled space (The Campus has an additional 52,000 square feet of exhibition space.) He’d been looking for storage space to reduce one of his gallery’s significant costs, and the building fit the bill.

That led to an Amazon-like business case for turning a cost that the six galleries share—storage—into a potential profit center. According to Cohan, places like Crozier, Uovo, and Mana—to name a few New York art-storage options—are priced for wealthy collectors, not Tribeca galleries who have to control their overhead costs. Already, the cooperative has created a business, Claver Crates, that will build custom shipping crates for art works. If that goes well, the group might expand into trucks to provide storage for other galleries. In this way, these midsized galleries are working on accruing the advantages of being a larger organization like a “mega” gallery without having to give up their independence or mom-and-pop appeal to collectors. To Cohan, the cooperation is both “generous and generative.”

|

|

| The Art Market’s Year of Magical Thinking |

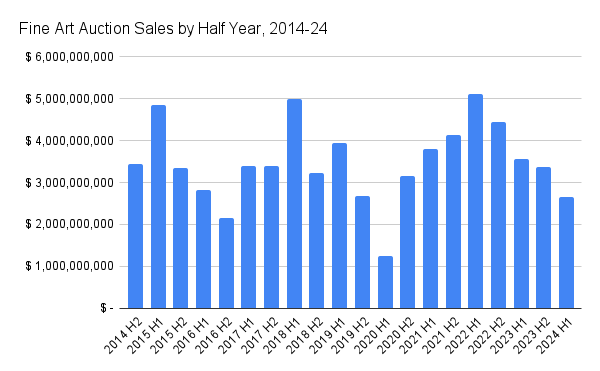

| Auction totals are down a jarring 25 percent from the first half of last year. But new data from ARTDAI, which contextualizes the results with sales from the past decade, suggests we’ve been here before—a couple times. |

|

|

|

| With much of the art world scattered for the summer, it was the perfect time to have our friends at ARTDAI perform a gut check on the market’s health over the first half of 2024. In short: These aren’t the glory days, but we’ve been here before. Fine art sales at Christie’s, Phillips, and Sotheby’s totaled $2.66 billion, according to ARTDAI—down 25 percent from the same period last year, and down 48 percent from the first half of 2022. One has to go back to the disastrous first half of 2020—you might remember a pandemic forcing everything to close down?—to find a lower number, at $1.24 billion. But that would hardly be a fair comparison.

The last time the auction market for fine art dipped this low without an external crisis was the second half of 2019, when all three houses posted nearly the same total ($2.67 billion). Or you can look back to 2016, when the first stirrings of Brexit, MAGA, and global populism spooked international markets. The auction total for the first half of that year was $2.83 billion—slightly higher than this current era, even if the vibe was similar—and $2.16 billion in the second half, which made 2016 a substantial reset after the strong market performance of 2013-15.

Does that augur a disappointing fall season this year? It’s hard to know. The market for fine art is highly dependent upon supply and external factors like interest rates, the overall health of the economy, and the amount of money the wealthy have to spend on art, as impacted by taxes and leverage. Right now, of course, the U.S. economy remains quite strong. Even with the inflation-fighting interest rate shock of the last 18 months, the Knight-Frank wealth report predicts a 28 percent rise over the next five years in the number of ultra-high-net-worth individuals, or those with more than $30 million in net assets. Nevertheless, stagnant art spending at auction suggests the world’s richest people have a surfeit of art, or would simply rather hold on to their cash. |

|

|

| A chart of the half-yearly totals reinforces that we’ve been here before. From the second half of 2015 through 2016, the market slid below the two-year moving average. From 2017 through the first half of 2019, spending at auction was remarkably consistent—in the $3.3 billion range—only interrupted by the large blip of the billion-dollar Rockefeller sale in the first half of 2018. Indeed, the Rockefeller sale was a market high from which spending slid 75 percent to the depths of the 2020 Covid closures. Even before that cataclysm, the fall from Rockefeller to the second half of 2019 was a full 47 percent. That puts the two-year 48 percent drop in spending from 1H2022 to 1H2024 in perspective. In other words, we’ve just seen the same drop from the Paul Allen auction in the second half of 2022 to the first half of 2024 that we saw from Rockefeller to two years later.

That market pattern should be reassuring to those in despair about the current state of spending. But the most recent period of auction sales doesn’t recapitulate what happened six years ago. The post-pandemic market has had a different, more orderly shape than previous market periods. From the second half of 2020—when the auction houses figured out how to attract large online audiences without bidders in the room—to the first half of 2023, auction totals rose steadily. In the second half of 2020, auction spending was $3.17 billion. By the first half of 2022, the market market had reached $5.1 billion.

Unlike earlier periods when sales rose and fell with the calendar (traditionally, the first half of the year is stronger than the second half) or the appearance of a rare super-collection, each semester rose steadily from the semester before. Then, defying past patterns, semester totals backed down on a steady basis for four semesters in a row. That’s how we got to where we are today. This orderly process was aided by the Macklowe family collection coming to market in two parts, spread between the second half of 2021 and the first half of 2022, and the Paul Allen collection in the second half of 2022. (These are not accidents; sellers make their decisions based on market conditions.) Nevertheless, the spending at auction in 2023 remained above the level of the second half of 2020 for both semesters and above levels seen in 2014, 2015, 2017, and 2018.

In other words, 2023 wasn’t so bad. It just felt bad after two straight years of exceptionally strong sales. We’ve only just now dipped below the average of the semester totals for the last decade. The auction market has had three solid years at or above the average volume for the auction season. The market is reverting to the mean, which puts the potential for a much-lower-volume autumn season—or even a bounce back—into perspective. There was a lot of spending to work through the system. |

|

|

| Over the past few months, I’ve been convening a secret group of fellow art data junkies—advisors, auction house data specialists, and market economists—to share ideas on what might help us better understand the current themes. When you think about it, the raw total figure really doesn’t say much about the health of the art market. The art press panics over falling gross auction receipts, but what does that really tell us? Art isn’t a necessity, like oil. It isn’t food or housing. Spending is entirely dependent upon enthusiasm. That’s what makes it so fascinating to me—and others. We look at the art data not to be excited by (or despondent about) the prices, but for indications about what’s important to people culturally.

One of the most promising turns in the last few years has been the continuing demand for a wider range of more diverse artists. That enthusiasm would show up in the numbers as lower dollar volume—the works are cheaper—but that wouldn’t necessarily be a bad thing.

With that in mind, ARTDAI ran these results but gave me the percentage of lots that were sold at prices above, within, and below the estimates. These numbers should give us a better sense of when the market is advancing (bidders are willing to pay more than sellers were asking) and when it is declining (the reverse). According to ARTDAI’s breakdown, aggressive bidding peaked in the first half of 2021, when slightly more than 50 percent of the lots at auction were sold for prices above the estimate. (ARTDAI had to do a little finessing of the data since they didn’t always have hammer prices going back nearly 11 years, but I’m confident they’ve got consistent numbers here. So don’t worry about the exact percentages. We’re just looking for the relative peaks.) That means half of the lots in that semester had aggressive bidding, a clear sign the market was underpriced.

Of course, when sellers see those kinds of results, they naturally want to get in on the action. Over time, more material comes to market and estimates begin to rise, choking off bidding. By the second half of 2023, the percentage of lots bid above the estimate range had fallen to its lowest level (35.2 percent) since the second half of 2019 (38.7 percent) and the first half of 2016 (38.1 percent.) That 35.2 percent figure was also the lowest level recorded for the entire decade. This first half of 2024 saw that number rise to 37.1 percent, suggesting that we may have already begun to see the market turn.

The concomitant measure—the percentage of lots that sell below the estimate or for a price that forced the seller to compromise on their initial hopes—peaked this first half of 2024, at 29.9 percent, which was slightly above the 29.7 percent rate for the second half of 2023. Previous peaks for this metric were in the second half of 2020, the second half of 2019, the second half of 2018, and the first half of 2016. But those peaks were a full 5 percent lower than the last two semesters’. Such high rates of works being sold at compromise prices tell us that too much property was priced far above the market. But they also tell us that sellers lost their nerve. They took what was offered at a higher rate than has been seen in the last decade, and they did it for two semesters in a row.

There’s a different market psychology at work now. Sellers who are willing to compromise are capitulating to the market’s price. In a strong market, sellers might prefer to take the work back and hope for another, better time to sell publicly or privately. In a weak market, sellers who need the cash are more likely to take whatever is offered. The high capitulation rates of the last two semesters—the highest of any period in the last 10 years—may be signaling a market washout. Sellers are losing hope of a better market within their ken and taking whatever price they are offered, no matter how disappointing. That’s a good thing. Markets renew themselves when the tide goes out. |

|

|

|

| FOUR STORIES WE’RE TALKING ABOUT |

|

|

|

| Burberry Blues |

| Charting the uphill battle for new C.E.O. Joshua Schulman. |

| LAUREN SHERMAN |

|

|

|

|

|

|

|

|

|

|

|

|

|

Need help? Review our FAQs

page or contact

us for assistance. For brand partnerships, email ads@puck.news.

|

|

You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with . To stop receiving this newsletter and/or manage all your email preferences, click here.

|

|

Puck is published by Heat Media LLC. 227 W 17th St New York, NY 10011.

|

|

|

|