Welcome back to Wall Power’s Inner Circle. I’m Marion

Maneker.

Miami has been surprisingly upbeat. Thank you to everyone who introduced themselves, I really do appreciate it. And I’ll say it again: This newsletter works best when I’m able to channel your interests and concerns. Don’t ever feel you can’t tell me when I’ve gotten it wrong. You can always reach me by responding to these emails, or texting +1 (917) 825-1391 on WhatsApp, Signal, or SMS.

Tonight, I’m running through the numbers from the New York sales some two

weeks ago. The $2.2 billion total is well above last year’s dismal results but still well below the post-Covid peaks of 2021 and 2022. That’s a good thing. The last thing the art market needs is to swing from one extreme to the other. Now it’s in something of a Goldilocks moment—not too hot, not too cold—but the numbers are more interesting than simply a recovery at the top of the market. Will this moment last? I’ll provide more details below the fold.

But first…

|

- It’s all about the collections, baby: If you want a sense of how important large estates are to the auction market, this chart that Pi-eX’s Christine Bourron posted on LinkedIn lays it out in great detail. Removing the estates

from the November results leaves the market still looking pretty good, but the total falls below the results for each season from November 2021 to 2023 (albeit above last year’s difficult season).

Perhaps most interesting: Among discretionary sellers, the results in 2023 were higher than in 2021 and ’22, when the sales were dominated by Paul Allen’s collection and one of the Macklowe sales. But to reach the peak sales volume for discretionary sellers, we

have to go back to 2017. In short: Although the art market perked up significantly two weeks ago, we’re just back to the middle—whether you measure it by overall volume, or exclude the collections and just look at discretionary sales.

|

|

|

The Breguet Classique Souscription 2025 represents a reinvention of a timeless icon

– paying tribute to the original aesthetic, elevated by a contemporary perspective. Join Breguet in celebrating 250 years of horological excellence. |

The Breguet Classique

Souscription 2025 represents a reinvention of a timeless icon – paying tribute to the original aesthetic, elevated by a contemporary perspective. Join Breguet in celebrating 250 years of horological excellence. |

|

|

- Guillaume’s history lesson: While we’re looking at historical data, I wanted to draw your attention to Guillaume Cerutti’s recent post displaying charts of Christie’s results during the

last 10 New York seasons. Using his own proprietary performance index (calculated from the hammer ratio multiplied by the sell-through rate), Cerutti tracked the last market peak to precisely November 2021. There was a slight recovery in November 2022, but after that it was a long slide to a fairly unprecedented (in recent years) fallow period of five seasons. (Down cycles normally last only 18 months or three seasons.)

Cerutti’s chart shows that the recovery is still below the low-water

mark of the previous cycles of 2021 and 2022. You should also notice the lot numbers remain well below what they were in the two November seasons of those years—Christie’s has been more cautious about what it brings to market during this fallow period. - Death and taxes: An art advisor told New York’s Rachel Corbett that last month’s art market bounce-back stemmed mostly from the dumb luck of having four major estates

come to market during the same season. It might have seemed that way, but selling this November was definitely a choice. The federal government does want to be paid estate taxes within nine months of a person’s death, but there is a six-month extension easily available. Patricia Weis died last October, and the Weis collection was committed to Christie’s in April, but the auction house and the estate’s advisors chose to sell during this season. Selma

Ertegun died in December of 2024. Joan Saltzman, Elaine Wynn, Cindy Pritzker, and Leonard Lauder all died this year, but Lauder’s death in June meant his heirs could easily have waited until May, if they thought that was a better time to sell. It’s hard to argue with the choice to sell this season. What looks like luck is often the product of hard work behind the scenes.

|

Now, let’s get to the main event… |

|

|

A deep data-driven dive into the November sales and what they tell us

about the art market’s “just right” moment. |

|

|

November’s New York sales prompted a huge sigh of relief from the art

market. Even though the last three years have seen strong sales in the price bands below six figures, the market cannot generate enough volume, momentum, or word-of-mouth urgency without significant transactions in the eight- and nine-figure range. That opportunity arrived this season, with the sales of collections from Leonard Lauder, Joan Saltzman, Cindy and Jay Pritzker, and Robert and

Patricia Weis, among others. The boost in volume also seemed to help bring in discretionary sellers hoping to draft on the estate-generated enthusiasm. All told, there were 40 lots that sold for prices above $10 million.

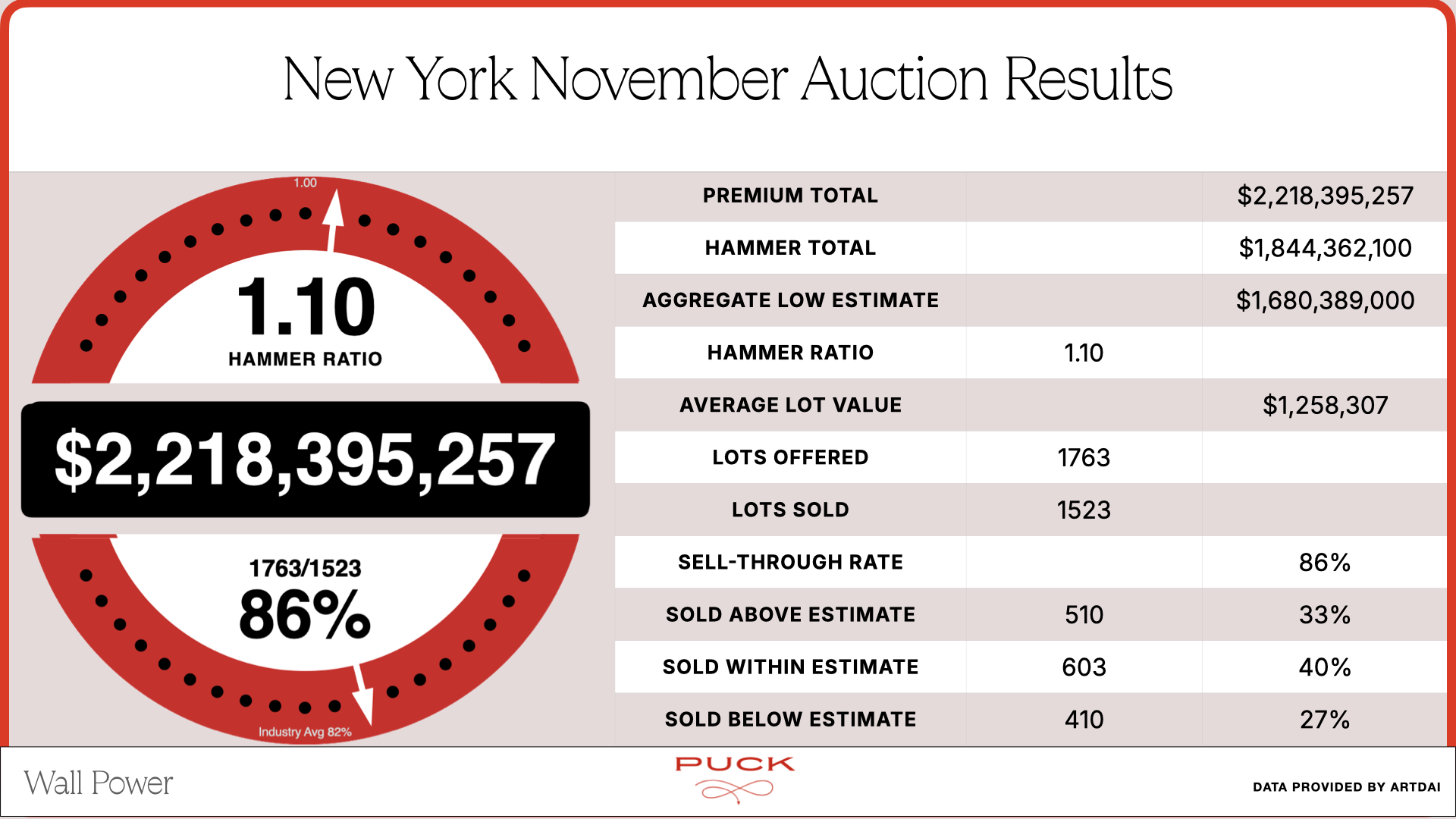

The result from Christie’s, Phillips, and Sotheby’s was $2.2 billion in sales, from 1,523 lots of a total offering of 1,763 lots—an 86 percent sell-through rate that’s an unmistakable sign of strength. Another indicator of an advancing market is the

overall hammer ratio—the aggregate hammer price of all lots divided by their aggregate estimates—which was a not-too-hot, not-too-cold 1.10. The estimate level has finally reached a point that is inviting for both bidders and buyers.

There has been a lot of loose talk the last few years about a buyer’s market, and I’ve often tried to slightly correct the discourse. Commodities become cheap due to low demand, but the world still needs them to flow. Not so with art, which has no

use value—when the art market goes cold, art just doesn’t come to market. It remains to be seen whether estimate levels will come down far enough in nominal terms, or inflation makes them more attractive. This season’s results, though, indicate that the appetite for spending money on art is also attracting art to the market. |

|

|

The Breguet Classique Souscription 2025 represents a reinvention of a timeless icon

– paying tribute to the original aesthetic, elevated by a contemporary perspective. Join Breguet in celebrating 250 years of horological excellence. |

The Breguet Classique

Souscription 2025 represents a reinvention of a timeless icon – paying tribute to the original aesthetic, elevated by a contemporary perspective. Join Breguet in celebrating 250 years of horological excellence. |

|

|

If anyone needs further assurance of momentum: Only 27 percent of the sold lots were

sacrificed at prices below the estimate; 40 percent of the lots sold within expectations; and a solid 33 percent of lots saw aggressive bidding over the estimate range. At the last peak of the market, earlier in the decade, we saw as much as 50 percent of the lots subject to dynamic bidding. The current numbers suggest we’re in a building—but not yet overheated—market.

Here’s another way to look at those numbers. A full 56 percent of the value of these sales, or $1.25 billion worth of

art, sold within the estimate range. The overall hammer ratio for those lots was a quite strong 1.20. In other words, a majority of the value was subject to healthy bidding. (That includes lots like the Klimt portrait that sold for $236 million—which was, believe it or not, still within the standard estimate range.) Another 18 percent of the value of these sales, or $395 million, was bid well above the estimates for a hammer ratio of 2.17. The sector at the very top of

the market is on fire.

Now for the cautionary part: 26 percent of the value of these sales, a total of $570 million, was sold below the estimates, which means a substantial portion of the market’s value still isn’t meeting sellers’ expectations. Too many of them, it seems, remain unrealistic about the value of their property. There’s no hard and fast rule about these statistics, but my guess is that we’ll know we’re in a bull market when the value of the marquee sales cycle sold above the

estimates exceeds the value sold below. It appears we’re not there yet. |

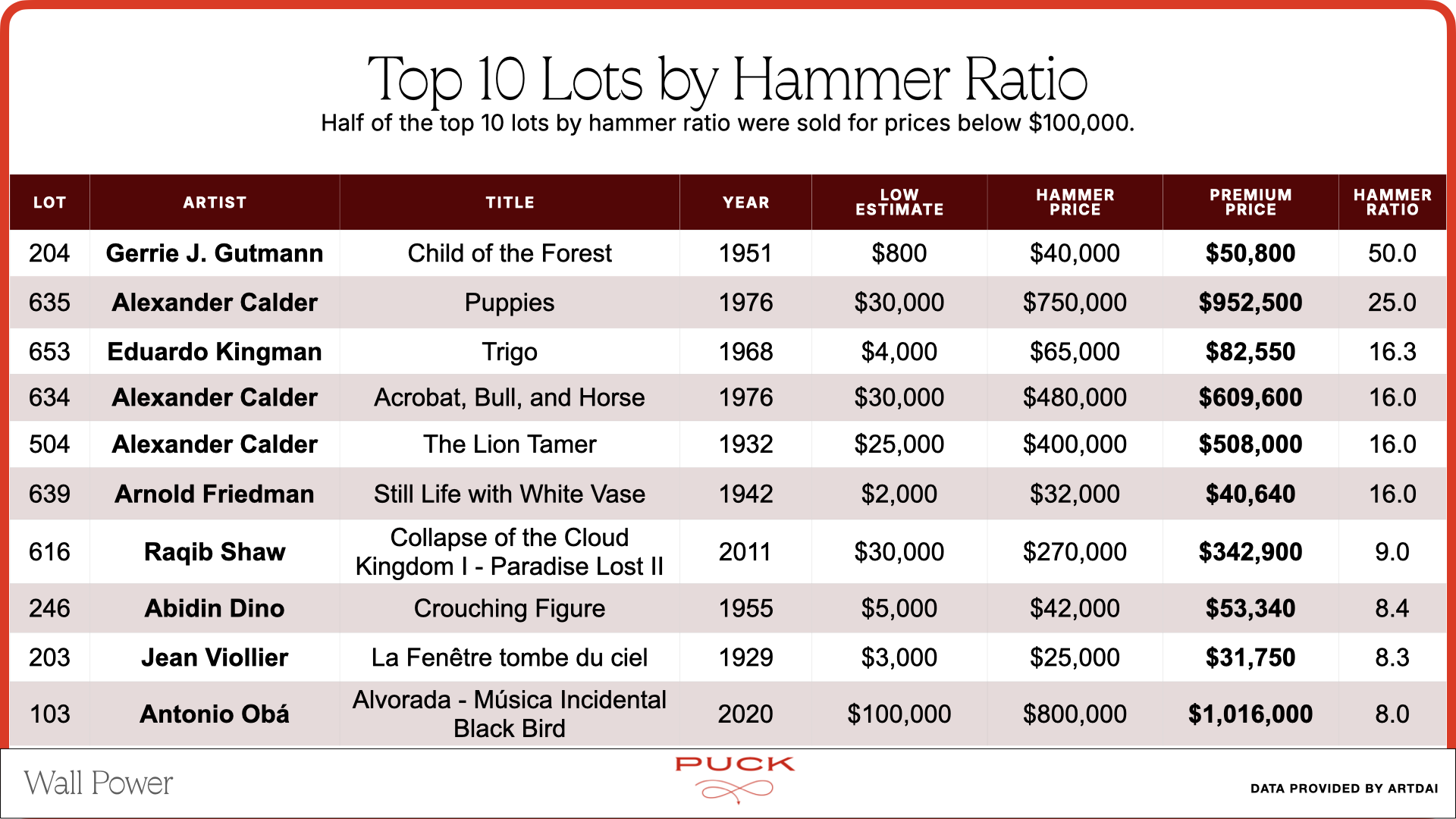

The top 10 lots by price and hammer ratio tell two conflicting stories. Obviously, with

so much high-value art on offer, lots from the major collections dominate this list. The three Klimts from the Lauder collection were the top lots, followed by the Pritzkers’ van Gogh and the Weises’ Rothko. Then came Selma Ertegun’s Frida Kahlo painting, the Claude Monet Water Lilies piece deaccessioned by the Kawamura Memorial Museum, and the Weises’ Picasso painting

of Marie-Thérèse Walter. Finally, we had two discretionary sales: the David Hockney double portrait that was sold to the guarantor, and a 1981 Basquiat that saw some bidding. |

On the far opposite end of the spectrum, the lot with the most astonishing bidding was a

painting by Gerrie J. Gutmann from the Exquisite Corpus collection that hammered at 50 times its estimate. That’s aggressive bidding! Other unexpected artists on the list include Eduardo Kingman, Arnold Friedman, Raqib Shaw, Abidin Dino, and Jean Viollier. Meanwhile, half of the 10 top works by hammer ratio sold for below $100,000. And the Antonio Obá work on the list was the

only one sold in an evening sale. |

Three Alexander Calder works made the list of top 10 by hammer ratio,

but that hardly describes the full scale of bidding on Calder’s 24 lots, 14 of which achieved prices above the estimate range, collectively posting a strong hammer ratio of 1.43. The prices that Calder achieved prompted one European collector to declare, “Calder is the Nvidia of art.” |

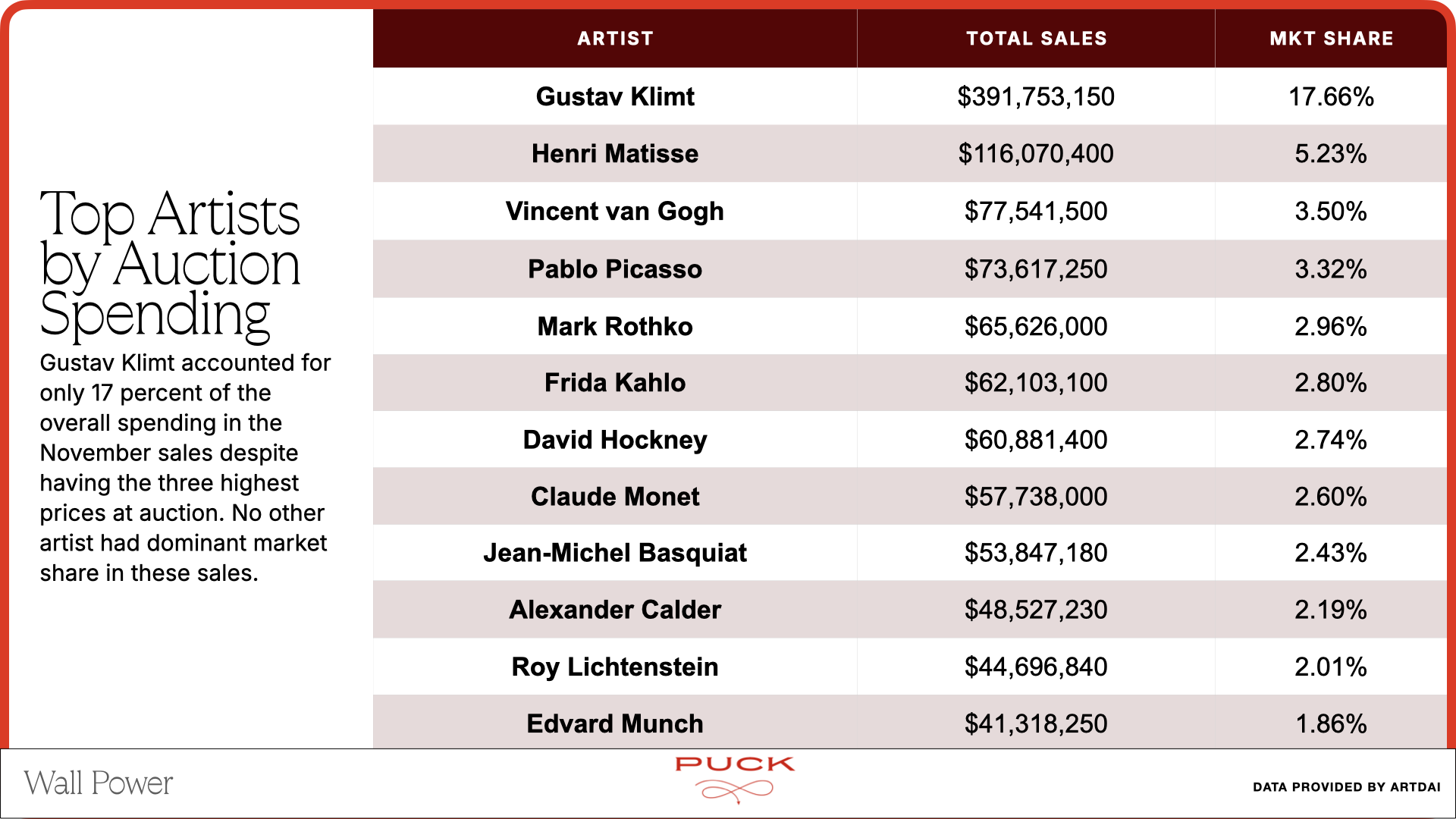

It isn’t a surprise that Gustav Klimt topped the market share chart, with nearly 18

percent of the dollars spent in the November sales. The art market used to be dominated by a few names—Picasso, Monet, Warhol—that accounted for the bulk of the spending. But this season Klimt held the position, and it was a substantial drop to the next biggest artist by dollar volume, Henri Matisse. The latter’s work garnered a little more than 5 percent market share. |

|

|

Vincent van Gogh was next with 3.5 percent, and Picasso also had a more than 3

percent share. Frida Kahlo was just under 3 percent, right next to David Hockney. Monet finally appears at a little over 2.5 percent, with Jean-Michel Basquiat trailing by only a bit. Calder accounted for more than 2 percent of sales, as did Roy Lichtenstein. Edvard Munch, surprisingly, was close behind, at just below 2 percent. |

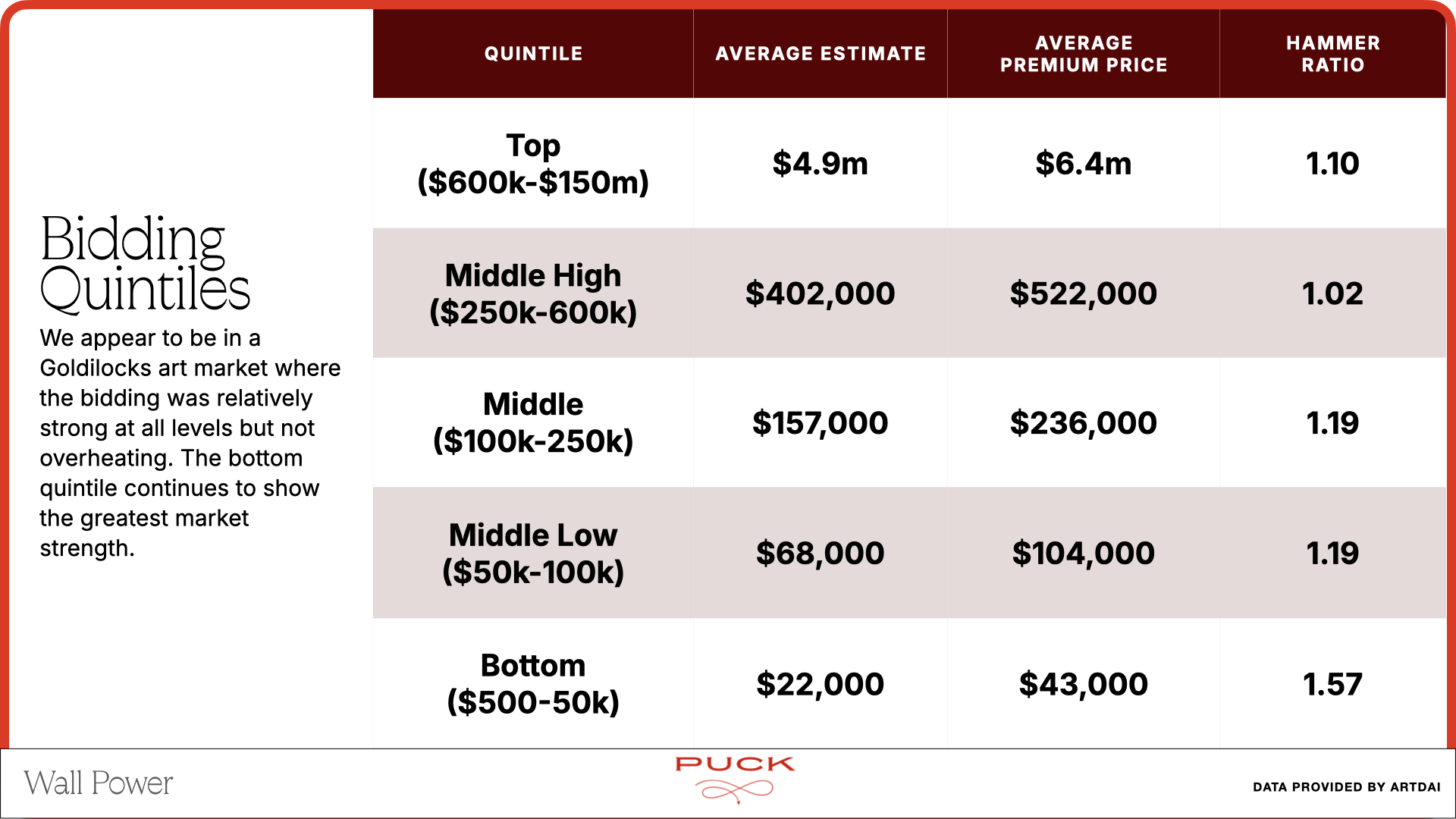

But the statistics that most interest me are the bidding quintiles. By separating the

offered lots into five bands and then measuring the estimate range, average estimate, average premium price, and hammer ratio for each one, I believe we can see which sector of the market has the most strength. In previous seasons, we have seen pronounced weakness in the upper three quintiles and persistent strength in the lower two.

This season we can see that the recovery has been across the board, a rarity in the art market. None of the quintiles has a hammer ratio below 1.02. The top

quintile came in at 1.10, with an average premium price of $6.4 million against an average estimate of $4.9 million. The middle high quintile, of works offered at estimates between $250,000 and $600,000, saw them sell at an average premium price of $522,000. In the middle of the market, where works are offered with estimates ranging from $100,000 to $250,000, the hammer ratio is a solid 1.19, with an average selling price of $236,000. In the middle low band, where works are offered between

$50,000 and $100,000, the hammer ratio was the same, and the average premium price was $104,000. (Buying art at auction isn’t cheap!) Finally—and here was a surprise—the bottom quintile actually increased from May. Works estimated between $500 and $50,000 had a hammer ratio of 1.57 and an average premium price of $43,000. With estimates being met or exceeded across every price range, it’s impossible not to give the market a clean bill of health.

That’s the final word on the

November sales. The top of the market came back without diminishing demand and interest in the lower price bands. The overall hammer ratio and the hammer ratios for each band are neither too hot nor too cold. It’s truly a Goldilocks art market. |

I hope that helps you better understand where we are in the art market. I’m having a

good time in Miami. I’ll send you a report on Friday.

M |

|

|

The ultimate fashion industry bible, offering incisive reportage on all aspects of the business and its biggest

players. Anchored by preeminent fashion journalist Lauren Sherman, Line Sheet also features veteran reporter Rachel Strugatz, who delivers unparalleled intel on what’s happening in the beauty industry, and Sarah Shapiro, a longtime retail strategist who writes about e-commerce, brick-and-mortar, D.T.C., and more. |

|

|

Finally, a media podcast about what’s actually happening in the media—not the oversanitized,

legal-and-standards-approved version you read online. Join Dylan Byers, Puck’s veteran media reporter, and Julia Alexander, a longtime media analyst, as they sit down with TV personalities, moguls, pundits, and industry executives for raw, honest, sometimes salacious conversations about the business of media and its biggest egos. New episodes publish every Tuesday and Friday. |

|

|

Need help? Review our

FAQ page or contact us for assistance. For brand partnerships, email ads@puck.news.

You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with {{customer.email}}. To stop receiving this newsletter and/or manage all your email preferences, click here. |

Puck is published by Heat Media LLC. 107 Greenwich St., New York, NY 10006 |

|

|

|