|

|

Welcome back to Dry Powder.

|

|

Happy Wednesday. And thanks as always for supporting our work here at Puck. Today, my thoughts on Joe Biden’s meeting with Fed chairman Jay Powell—and why, in reality, their non-interference pact only runs one way.

|

|

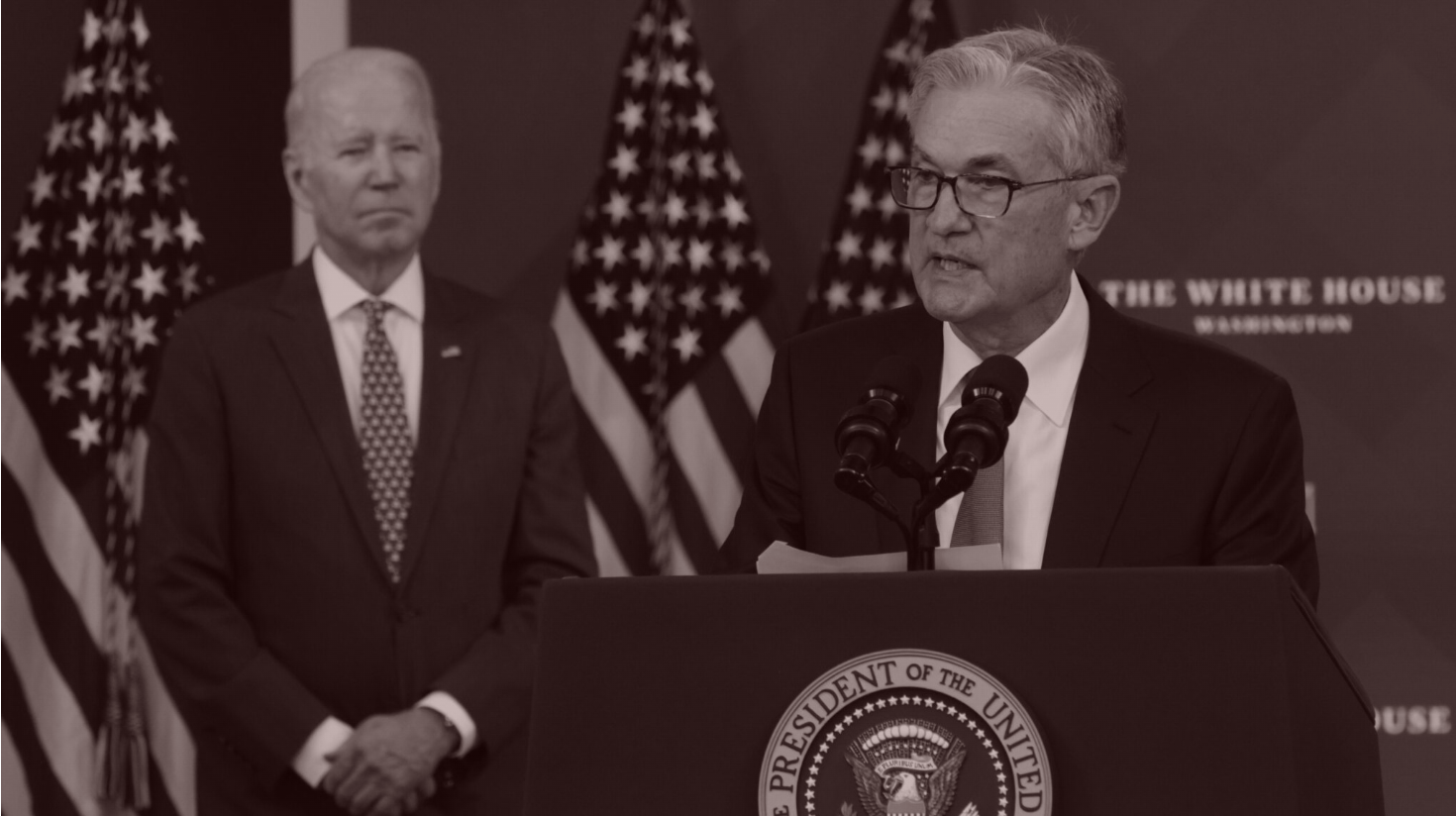

| Biden’s Fed Gamble |

| Biden has wholeheartedly endorsed Fed chairman Jerome Powell’s painful decision to take the punchbowl—ZIRP, Q.E., etc—away after 14 years. Does the political calculus suggest a short-term recession and midterm bloodbath followed by a rebound in ‘24? |

|

|

|

Of all the headaches that Joe Biden has faced during his two years in office—the pandemic, obviously; the collapse of his signature multi-trillion (and then trillion-plus) infrastructure package, Afghanistan, the war in Ukraine—the president has seemed particularly miffed about a recent domestic culprit: inflation. Insidiously rising prices, after all, are the sort of things voters feel in their wallets and their guts, especially when they become memorialized via gas prices during the summer vacation season. According to a recent Washington Post report, Biden has for a while been rousing his administration to do more to combat inflation, publicly and privately. During an Oval Office meeting with Treasury Secretary Janet Yellen and Fed Chairman Jerome Powell, Biden declared that addressing inflation remained his top priority. It was a powerful public statement amid a moment when more aid was being shipped to Ukraine, and the pandemic was surging once again.

But in an equally prominent opinion piece in The Journal, Biden also tried to straddle his position. He may be laser focused on curbing inflation, but he isn’t going to meddle with the Fed’s monetary policy. “My predecessor demeaned the Fed,” Biden wrote in the May 30 opinion column, “and past presidents have sought to influence its decisions inappropriately during periods of elevated inflation. I won’t do this.”

I presume that Biden thinks he’s being respectful by taking a hands-off approach to the Fed and by letting Powell try to tame on his own, with his Fed brethren, what seems like runaway inflation. But it’s the policies of the Fed since the 2008 financial crisis that have gotten us into our current economic fix, and I’m not convinced that the fox, now that he’s made his way into the hen house and ravaged it, should be free to continue to roam about without an escort. In the aftermath of the 2008 financial crisis, the Federal Reserve, then led by Ben Bernanke, implemented a variety of policies designed to reduce both short-term and long-term interest rates to get them to be as close to zero as possible for an extended period, which lasted nearly 14 years, until March 2022, when Powell started raising rates again. The various policies that Bernanke and his successors, Yellen and Powell (during his first term as Fed chairman), pursued—known as ZIRP (Zero Interest Rate Policy) and Q.E. (Quantitative Easing)—were plenty clever and, at least at first, helped pull the U.S. economy out of its financial doldrums by making money both plentiful and dirt cheap to borrow for both the short and long term.

Their thinking, which I don’t dispute, was to get America’s animal spirits ignited again after the shock of the financial crisis, which almost led to the complete meltdown of the Wall Street financial system and did claim as victims all of Bear Stearns, Lehman Brothers and Merrill Lynch, as well as big banks such as Citigroup, Wachovia and Washington Mutual. The Fed, the lender of last resort, had to do something, given the dire situation, and Bernanke, to his credit, decided that the something to do was to make money cheap and readily available so that companies would borrow plenty of it and jumpstart their business plans. It was a lesson he learned studying the mistakes the Federal Reserve made during the Great Depression and he was determined not to repeat them.

People who make money from money—hedge fund managers, private equity moguls, Wall Street bankers and traders—also saw the wisdom of Bernanke’s policies and went to town figuring out as many ways as they possibly could to make more money from the Fed’s largesse. In the end, through various iterations of the Q.E. program, the Fed’s balance sheet increased 10-fold, from $900 billion before the crisis to $9 trillion in assets today, as a result of the Fed going into the market and buying all sorts of debt securities, driving up their price and lowering their yields. Basically, between ZIRP and Q.E., the Fed was big-footing the debt markets, in effect single-handedly manipulating the price of money down to the lowest levels in recorded history.

Big things were bound to happen, and they did. The Dow Jones Industrial Average, which hit a low of around 6,500, in March 2009, fairly exploded under the Fed’s low interest-rate policies, hitting an all-time high of 36,585 in January, a spectacular increase of more than 450 percent in 13 years as investors pumped money into stocks, ratcheting up the risks they were willing to take along the way. Few complained, especially since the constituency for falling stock prices—aside from a few short-sellers—is very small indeed. Who doesn’t applaud a rising stock market? The Fed’s policies not only made a lot of people very, very, very rich, but were also politically popular, especially on Wall Street.

A similar dynamic occurred in the debt market, as you would expect when a gargantuan buyer—in this case the Fed—was determined to buy pretty much anything that looked like debt and stick it on its balance sheet. By increasing the demand for debt and debt securities, the Fed drove up the price of these securities and, because of the fact that bond prices are inversely correlated to bond yields, rising bond prices drove down bond yields to unprecedented low levels. One need look no further than the high yield bond index published by the Federal Reserve Bank of St. Louis.

Thanks to Bernanke, Yellen and Powell, the average yield on a junk bond (issued by companies with the poorest credit) fell to below 4 percent last July for the first time ever. Given that Mike Milken, the pioneer of junk bonds, used to price them to yield 10 percent or more, and that was before he also demanded warrants from many issuers to sweeten the pot, there is simply no disputing the longtime mispricing of risk in the bond markets that occurred between 2009 and the start of 2022.

|

|

|

Now, to extend the metaphor, the chickens have come home to roost. There’s little dispute that the Fed stayed with ZIRP and Q.E. for way too long. They were fine ideas to which the Fed and the financial markets became hopelessly addicted. It was obvious the addiction would be tough to break. Who doesn’t love high stock prices and low interest rates? Who doesn’t love high Bitcoin prices and high home prices? And who doesn’t love the political currency that comes from presiding over a booming, cheap-money economy? Many people thought Powell would start the weaning in 2019 until President Trump talked him out of it during a mysterious dinner at the White House in February 2019. Now the party seems to be over. And while Biden may be framing his decision to let Powell manage the situation, it’s become his political problem, especially if things don’t go smoothly.

Asset prices and inflation have gotten so far out of hand that it appears Powell & Co. will have little choice but to follow through on their pledge to raise short-term interest rates at each of their meetings this year and to finally curtail the Q.E. bond-buying program.

Powell is once again walking the tightrope. If he acts too aggressively—say, by raising interest rates more quickly than the markets expect—he can make a recession a self-fulfilling prophecy, as investors, C.E.O.s and others lose confidence. If Powell loses his nerve, as he did after Trump took him to the woodshed in 2019, then the animal spirits kick in again and the speculative cycle reignites. This is the moment for Powell to follow through on raising rates, to stay the course and show some backbone. In many respects, the health of the economy is highly correlated to how people feel about the economy. It’s a confidence game. And Powell is the one person who has to keep his resolve.

So far, the financial markets have reacted as if investors believe that this time will be different and that Powell will actually follow through on ending the years of easy money and low interest rates. Biden’s pledge to leave Powell alone reinforces the view. But the pain of withdrawal is real. The equity markets have tumbled. The D.J.I.A., now at around 32,700, is down some 10 percent since January. The Nasdaq is down 24 percent since the start of the year and the S&P 500 is down 14 percent. The yield on the average junk bond was nearly 7.7 percent last week, almost a doubling since its July 2021 low. Investors who thought that junk bonds were priced properly last summer have gotten crushed. (For reasons that are hard to fathom, since reaching the 7.7 yield last week, junk bonds have rallied to yield 7 percent these days, an impressive 10 percent decrease in yield in a few days. Perhaps junk bonds rallied in sympathy with the rally last week in the stock markets.) And Bitcoin, which is supposed to be digital gold—a store of value when all about you are losing their minds—has so far failed to live up to that promise. Bitcoin is down 34 percent so far in 2022. And I won’t even mention the fate of some of the other truly wacky cryptocurrencies.

Loyal readers will know where I think we’re heading now: I can’t speak specifically about inflation. Some say it has peaked and the retreat has started; others say that until real interest rates are positive, inflation won’t be tamed anytime soon. As for financial markets, the reckoning is long overdue, and although they may have hit the pause button last week after seven tough weeks, we’re heading for a rough but ultimately cleansing summer. At this point, since President Biden chose to renominate Powell for a second term and he has been confirmed by the Senate, Biden’s political fate, at least as it pertains to the midterm election in November, is now in Powell’s hands. Chances are he won’t be able to put enough foam on the runway by November 2022 to land this thing safely but Biden’s probably betting that Powell will have figured it out by 2024, and he just might.

Robert Wolf, the former head of UBS in the Americas and now the founder of 32 Advisers, his own advisory and investment firm, had the privilege, he says, of knowing and working with Paul Volcker, years after Volcker was the Fed chairman tasked with taming the runaway inflation of the 1970s. In a recent chat, Wolf told me that we are in a period of “heightened trepidation” in both the economy and in the financial markets and that inflation will likely remain greater than 4 percent, rather than the 2 percent rate that is the Fed’s stated target. He thinks Powell should use every arrow in his quiver to get inflation under control, including the idea that the Fed might raise short-term interest rates by 75 basis points or more.

Wolf says we’re not in a bear market, at least not yet. And he’s right about that, despite the Nasdaq’s swoon—admittedly after a long run-up. So, no, we may not be in a bear market yet but I’m pretty sure one is lurking nearby. At an investor conference today, Jamie Dimon, the chairman and C.E.O. of JPMorgan Chase, was blunter. He referred to what’s coming in the financial markets as “a hurricane,” before adding, “We just don’t know if it’s a minor one or Superstorm Sandy ... And you better brace yourself.” Whether Powell can land us in the eye of the storm will determine the fate of the U.S. economy as well as our political landscape.

|

|

|

|

| FOUR STORIES WE'RE TALKING ABOUT |

|

| The NBCU Deal Machine |

| In a special podcast, Dylan Byers and William D. Cohan inspect the values and virtues of the Comcast board room. |

| DYLAN BYERS & WILLIAM D. COHAN |

|

|

| Putin's Waiting Game |

| America's support of Ukraine has been a bipartisan issue, but an ebbing of financial support may be coming into sight. |

| JULIA IOFFE |

|

|

|

|

| Seth Green's Stolen Ape |

| Notes on a digital heist, and the enormous unresolved questions surrounding N.F.T. rights. |

| ERIQ GARDNER |

|

|

|

|

|

|

You received this message because you signed up to receive emails from Puck

Was this email forwarded to you?

Sign up for Puck here

Sent to

{{customer.email}}

Unsubscribe

Interested in exploring our newsletter offerings?

Manage your preferences

Puck is published by Heat Media LLC

64 Bank Street

New York, NY 10014

For support, just reply to this e-mail

For brand partnerships, email ads@puck.news |

|

|