{{ 'now' | timezone: 'America/New_York' | date: '%b %d, %Y' }} |

|

|

|

Welcome back to Wall Power, and happy Tax Day to all who celebrate. I’m Marion

Maneker.

Today, I’m pleased to announce that Clare McAndrew is starting what I hope will be a series of discussions with Wall Power about the data she generates in her benchmark reports for Art Basel and UBS—particularly her newsmaking annual report measuring the art market, the latest edition of which came out just last month. We plan to focus each conversation on a chart from her research, which Clare will explain and analyze

in even greater detail. In this inaugural conversation, we’re looking at the top line, the total number of works sold, and her method for arriving at those numbers.

Up top, I have some news and notes on two interesting auction consignments: one from Adele and Enrico Donati, and another from George Condo’s ex-wife, Anna.

Also mentioned in this newsletter: Jeff Yin,

Andrew Wolff, the Neuendorf family, Jacob Pabst, Pablo Picasso, Wassily Kandinsky, Yves Tanguy, Alexander Calder, Michael Baptist, Roy Lichtenstein, Keith Haring, Ed Ruscha, and more… |

|

|

|

A MESSAGE FROM OUR SPONSOR |

A MASTERPIECE IN MOTION Unmistakable style. Undeniable attention to detail. Experience composition and craftsmanship at their finest in a Range Rover.

EXPLORE

|

|

|

|

-

Artsy x Artnet: In news that’s not news, the newish owner of Artsy and Artnet has decided to have Jeff Yin, Artsy’s current C.E.O., combine operations and manage both companies. That said, Artsy and Artnet will continue to operate as distinct brands.

It’s been a year since former Goldman Sachs partner Andrew Wolff, now head of Beowolff Capital, broke the Neuendorf family’s control over Artnet, and six months since

Jacob Pabst removed himself without warning from the role of C.E.O. Quietly, Wolff also obtained control of Artsy, though some of the original investors I spoke to in the past year said they had no idea what was going on over there. Now they know. - Donati’s $40 million Picasso: Sotheby’s announced earlier this week that it will sell the estate of Adele and Enrico Donati, featuring a 1909

Pablo Picasso cubist work, Arlequin (Buste), estimated at $40 million. Enrico was a prominent surrealist artist of the 20th century who died in 2008; Adele—who, according to Sotheby’s, was the creative director of the French perfume house Houbigant—died last September. Also included in the consignment are

Wassily Kandinsky’s Rote Tiefe (Red Depth), from 1925, estimated at $12 million; a nice Yves Tanguy, Aux Aguets le jour, from 1939, estimated

at $800,000; and an untitled tabletop Alexander Calder work from 1950, estimated at $700,000.

- Jump-starting the Condo market: Christie’s will be selling 27 works by George Condo in a single-owner session in the postwar and contemporary art day sale on May 21. The works—a mixture of paintings, sculptures, and works on paper—come from the holdings of Anna Condo, who was married to the artist for 28 years

until they divorced in 2017, whereupon she received art and other assets in the settlement. (She has previously sold work at auction.) The most valuable object in the collection is a painting from 2001, estimated at $500,000.

The Condo market has been cycling down since its peak, in 2021, when nearly $74 million worth of the artist’s work was sold at auction. Last year, auction sales reached only $26 million, and they’ve hit $5 million so far this year. That doesn’t mean, however, that

demand for Condo’s art has waned—there’s reason to believe that primary and secondary prices for his work have risen to a point that limits both supply and demand.

With these sales, Christie’s Michael Baptist is hoping to replicate some recent successes in which new supply and that holy trinity of auction success—low estimates, strong provenance, and being fresh to the market—have broken a down cycle in an artist’s market. It’s similar to what’s been happening

with Lichtenstein recently as the family has held a series of sales. Baptist also referenced recent sales of Keith Haring’s subway drawings and a large cache of Ed Ruscha works that came to market in the past few years.

|

If you like data, you’re going to love this conversation… |

|

|

|

Clare McAndrew, the author of Art Basel and UBS’s influential annual report,

discusses calculating transactions in mixed years, the risk of surveying dealers to death, and how she compiles the art market’s most dependable and authoritative assessment. |

|

|

|

Clare McAndrew should need no introduction to readers of Wall Power.

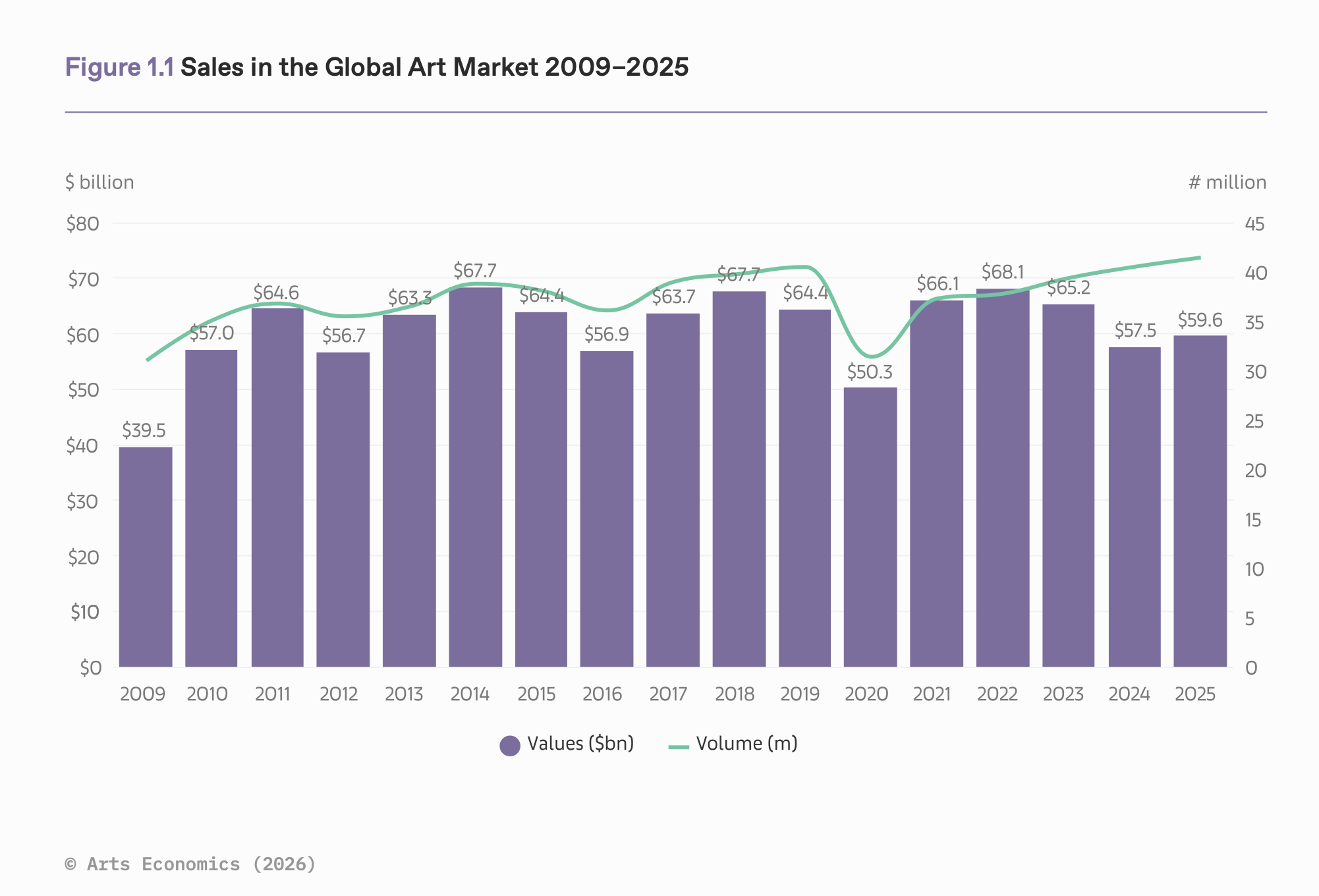

Her report measuring the art market is an annual event, and the total sales number she produces is cited around the world. But the value of McAndrew’s work goes beyond that marquee figure ($59.6 billion last year), and the report contains a lot more interesting data and insights into how the art market, dealers, and collectors function. |

|

|

|

A MESSAGE FROM OUR SPONSOR |

A MASTERPIECE IN MOTION Unmistakable style. Undeniable attention to detail. Experience composition and craftsmanship at their finest in a Range Rover.

EXPLORE

|

|

|

|

In an effort to surface many of those insights, I’m kicking off a series of

conversations with McAndrew in which we’ll unpack some of the charts she produces and tell the stories behind the bars and meandering lines. For today, we discussed the “mixed bag” of 2025 results, the growth of online sales, the challenges of quantifying the China market, and much more. |

|

|

|

Marion Maneker: Your

latest report says the art market rose 4 percent in 2025, to $59.6 billion in overall sales. Where does that number stand relative to previous years over your 20-plus years of doing this report?

Clare McAndrew: This was a step-up, rather than any kind of massive boom. I had to qualify this when I wrote about the positive recovery in the first paragraph of the report, and the first chart showing sales over the last decade makes it clear

that the market was still down about 7 percent compared to where it was 10 years ago. That is a really interesting dynamic: It hasn’t really grown from that point.

Dealers made up about 58 percent of sales, but their aggregate sales growth was sluggish, at around 2 percent in 2025. The largest dealers saw a small improvement, but even in that $10 million-plus segment, around 48 percent of dealers improved while 43 percent went down. It was a really mixed bag. The lower-end dealers did

well, but they don’t shape the big picture that much. Then there was a stagnant segment from $1 million–$10 million dealers, which is a big portion of my survey respondents and an important part of the overall market when you consider the distribution of sales.

Auctions did better. Public auctions make up around 35 percent of sales and were up 9 percent. The smaller private sales segment—about 7 percent of total value—was down 5 percent. Performance was proportional to price level:

Sub-$250,000 segments at auction were stagnant while segments above that grew, with the best annual growth at the very top, which is what really turned the auction sector around.

So it was an improvement, but in context, the market is still not where it was at the post-Covid peak in 2022—and still not where it was 10 years ago.

One of the reasons these numbers are hard to understand is the sheer number of factors involved. There are the internal dynamics of how the art

market works, and within that, global liquidity and other macroeconomic considerations.

Right, and although you can find relationships between parts of the art market with, say, financial markets, or the direction and spread of wealth in different periods, there are no perfect and consistent correlations. It’s an ebb and flow with art sales because this is such a supply-driven marketplace. When the market is low, it takes a while to build

confidence and encourage vendors. When dealers and auction houses can get the right supply onto the market, that turns the cycle positive. But although a positive market can have a good run, it inevitably also creates scarcity in the pipeline, which eventually tapers, and then you’re on the down slide again.

I’ve always believed that if you can get the right material onto the market, there are always people waiting in the wings to buy it, no matter what’s happening in the broader economy.

I think that’s what happened at the end of last year. It’s about feeding that supply pipeline—and the outlook coming into this year is still positive in that regard. There are some big collections coming on to the market.

One really interesting thing in your chart is the way the number of objects sold has gone up and to the right since 2020. It was steady for a long time, and then suddenly it’s moving in one direction. What’s driving

that?

I think some of this growth in the volume of transactions is tied to the growth in online sales, which remain dominant at the lower end of the market. We saw a spike in sales through online channels from 2020 onward—and they’re still running at much higher levels than they were pre-Covid—but because they still are mainly focused at lower prices, they don’t have as much effect on what’s happening in terms of overall sales. That segment is

still very much concentrated under $50,000, so you need a lot of transactions to shift meaningful value.

There are also a lot of auction houses and dealers operating at that lower end who are thriving—at least in terms of volume. Many categories that the big auction houses have moved away from still sell well through other channels.

I think that’s where most of the business in the art market is. If you look at the auction sector in

any given year, over 90 percent of lots sold are in the sub-$50,000 segment, with a large portion actually under $10,000. That’s really where most of the day-to-day business of the art market takes place. |

The

Madness in the Method

|

Can you describe your methodology?

For

the annual art market report, I cover dealer and auction sales. Everyone assumes the auction sector is the easy part, but it’s not that straightforward. There’s a lot of cleaning, correcting, and assembly, especially in certain regions. China is always particularly complex and challenging every year, and it takes a lot of work that has to be done as it is such an important auction market. The great thing about auctions, though, is that you do get transaction-level data, so you can track sales

and prices in detail by segment or sector or artist.

For dealers, as with any industry that has private sales, there’s limited public records and official statistics, so surveys are necessary. These have improved over the years, and I’ve worked more closely with gallery associations. Coverage is still only ever going to be a sample of the total number of businesses. I’ve always said that I cover a fairly representative sample of the mid-to-high-level businesses in the sector, but there’s

a very long tail of small businesses that don’t get picked up in the survey as they are harder to reach, and for which I use conservative estimates. I’m aware that may mean underestimating some smaller markets, and this year I’m focusing a bit more on markets outside the traditional core in Asia Pacific and other regions, where there isn’t such a strong network of galleries. |

|

|

|

How often do you do the

surveys?

We survey dealers once a year now. I was doing it a couple of times a year, but I [only] do it once a year now, mainly at the request of dealers who get surveyed to death every time they participate in an event or go to a fair. I try to focus on response quality rather than only worrying about the quantity, and I incorporate whatever official statistics exist, alongside qualitative interviews and conversations with businesses all year

round.

I’m also very aware that there’s probably a significant amount of transacting I’m not capturing at all that goes on outside of dealers and auction houses. Our survey of global collecting that I’ve been doing in conjunction with UBS for the last few years, for instance, showed a large increase in artist-direct sales last year to high-net-worth collectors. So I’m covering the core of the market and tracking how that shifts and expands—but there’s growing activity happening outside

that realm.

I think other people would be tempted to try to quantify that. And as important as it probably is in the overall health of the market, I think there’s just no way to get it right.

I have done it before on a smaller national scale, and I’m trying to put together something more collaborative to do it again internationally. But it’s difficult. If you want to look at artists and how much they are selling directly, you have

to ring-fence them in some way to be able to corral them into a surveyable and researchable group. That generally involves working with arts councils and artists’ associations, so it has to be approached at a national level, and it would be a big project to put together. I’m trying to work with academic colleagues to assemble a conglomerate of people who might be interested in engaging with a project like this, because it’s too much to take on alone.

Everyone has opinions about

your work, which is itself a testament to how widely it’s referenced and used. The one thing that’s clear is you have a consistent methodology, and you’ve applied it over a long period of time. So if nothing else, we’re getting your estimation of how to measure this market longitudinally.

The range of criticism I’ve gotten over the years is interesting—some say the numbers are too small, others say too big, and these are usually critiques based

on an opinion or a best guess. I try to take all constructive feedback on board. I don’t rally against it like I used to when I was younger. I’m continuously trying to improve the research every year, so I’m genuinely interested to hear feedback—especially from people actually in the art trade itself. In the dealer sector, we’re always pushing for more responses and better coverage, while being aware that there’s no way to fully cover the dealer segment without a better mechanism for dealers to

input data on a more continual basis—which is something I’m hoping to figure out for the future.

Apart from getting better coverage, I’m continuously improving the survey instruments—what questions I ask and how I ask them. Sometimes it’s as simple as not just asking for a single number, but developing a series of questions around an issue to make the estimates more reliable. But it’s always a balance of trying to make things easy and efficient for the key suppliers of the information

with the limitless range of questions that are interesting to ask. Coming out of Covid, when everyone was going down, or in 2021, when everyone was on the up—those are the years where you feel very confident about the figures you’re putting together. It’s the mixed years—where pluses and minuses make for modest growth or modest decline—where you have to sense-test the results more carefully to make sure you’re on the right track. There will always be a human element to this work—some of the

biggest insights I get are from talking to people in the dealer and auction sector. |

Thanks to Curtis Rowser for doing the heavy lifting on turning this

conversation into a tight interview. I will be back on Friday.

Speak to you then,

M |

|

|

|

Puck founding partner Matt Belloni takes you inside the business of Hollywood, using exclusive reporting and insight to explain

the backstories on everything from Marvel movies to the streaming wars. |

|

|

|

Ace media reporter Dylan Byers brings readers into the C-suite as he chronicles the biggest stories in the industry: the future

of cable news in the streaming era, the transformation of legacy publishers, the tech giants remaking the market, and all the egos involved. |

|

|

|

Need help? Review our

FAQ page or contact us for assistance. For brand partnerships, email ads@puck.news.

You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with {{customer.email}}. To stop receiving this newsletter and/or manage all your email preferences, click here. |

Puck is published by Heat Media LLC. 107 Greenwich St., New York, NY 10006 |

|

|

|

|