|

Welcome back to Wall Power, midweek Inner Circle edition. I’m Marion Maneker. Tonight, we’re looking at the results from London’s sales, which were down from the previous year. Nevertheless, market dynamics are pointing in the right direction. I’ll get into much greater detail below.

But first, Julie has a word on single-owner collections…

|

|

|

|

Julie Brener Davich |

|

|

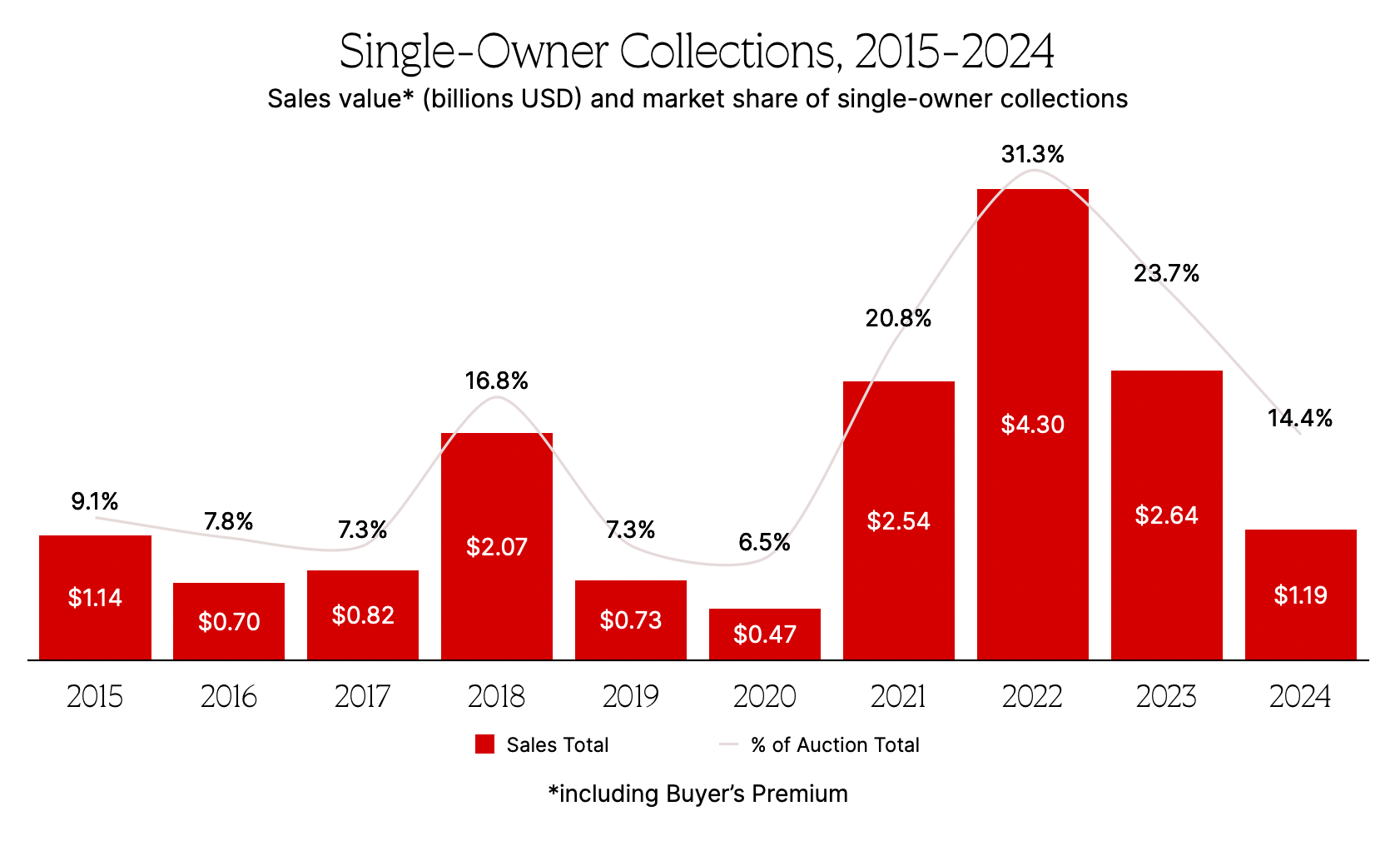

There are plenty of art data companies that publish market reports—pick your poison. I’m currently most intrigued by ArtTactic’s single-owner collections report, which shows collection sales totals as a portion of the larger auction market over the past 10 years at Christie’s, Sotheby’s, and Phillips.

|

|

For starters, if you look at the 2015–2020 range versus 2021–2024, you’ll see a big jump in the value of single-owner collections. That’s partially because of the oft-referenced “Great Wealth Transfer”—the passage of wealth from the Greatest Generation to their heirs. The 2018 total, for example, includes the $835 million Rockefeller estate at Christie’s. But the numbers are also impacted by some giant tentpoles. The 2021 total includes the $676 million Macklowe collection (Part I) at Sotheby’s, which featured an $82.5 million Rothko, a $78.4 million Giacometti, and a $61.2 million Pollock. Of course, the 2022 number includes not only the historic $1.6 billion Paul Allen collection at Christie’s, but also the Anne H. Bass, Ammann, Getty, Lalanne, Solinger, and Hotung collections. These contributed to the record $4.3 billion in single-owner collection sales that year, or an astounding 31.3 percent of global auction sales overall. As for the sell-through rates on collections, they are reliably and consistently high—between 88.5 percent and 91.5 percent over the past four years—which is one reason why the auction houses like them.

Overall, the value and number of single-owner collections that hit the block in any given year is a huge factor in determining the size of the art market, writ large. If executors don’t have to sell off assets in a given year—because, say, a daunting tax bill or personal crisis forces their hand—they sometimes prefer to time the market, and avoid periods where prices are depressed. In that way, a down market can reinforce a down market—which is exactly what happened last year. There were no big collections in the May season; in November, the Ertegun collection brought in $196 million, the bulk of which was the $121.6 million Magritte, and the Miller collection sold for $216 million. Both were solid, but not historic.

Collection sales, of course, have a significant impact on the houses’ top lines as well. The fight for single-owner collections is about bulking up total sales figures and market share—as well as bringing additional property to auction tied to the fame or renown of a premier collector. Blockbuster collections draw more sellers and buyers (and press attention) to the season. If a collection is too big, however, a house risks sending consignors running to the other houses for fear that their own property will get lost in the commotion.

Most of the highest-value collection sales have been dominated by impressionist and modern works, given the tastes of that generation, but there are certainly also big-ticket collections of postwar and contemporary art, such as the Macklowe collection—which the ex-couple sold sooner than they would have liked, thanks to a New York court ruling in a very expensive divorce.

In other words, you never know what’s coming around the bend. Keep all this in mind when the Riggio collection—estimated to be worth more than $250 million, making it potentially one of the 10 most valuable collection sales ever—hits the block in May at Christie’s.

|

|

|

Christie’s Hong Kong Sale Takes Shape with $13M Basquiat

|

|

Jean-Michel Basquiat, Sabado por la Noche (Saturday Night) (1984).

|

|

Thanks to Christie’s new Hong Kong headquarters at the Henderson building, the auction house will hold a sale in conjunction with Art Basel Hong Kong in two weeks. To stir excitement, Christie’s announced a 1984 Jean-Michel Basquiat painting, Sabado por la Noche (Saturday Night), estimated at HK$95 million ($13 million). The work was previously featured in the Heads On: Basquiat & Warhol exhibition, which Christie’s held in Seoul in September 2023.

Alongside the Basquiat in the Hong Kong evening sale are René Magritte’s Reverie de Monsieur James (1943), estimated at HK$42 million ($5.4 million); a Zao Wou-Ki abstract from 1967, estimated HK$40 million ($5.2 million); a Pierre-Auguste Renoir landscape from 1892, estimated at HK$18 million ($2.4 million); a Zhang Enli triptych from 2002, Intimacy, estimated HK$18 million ($2.4 million); and, Christine Ay Tjoe’s Layers as a Hiding Place #2, estimated at HK$12 million ($1.5 million).

Ay Tjoe and Zhang both have the opportunity to set new record prices at auction. The Zhang is already estimated above his previous auction high, and earlier this year, Ay Tjoe’s Lights for the Layer achieved a record $2.1 million price at Sotheby’s in Singapore.

|

|

Now let’s get to the data from London…

|

|

A lack of high-value lots, and some misplaced optimism, led to a 56 percent sales plunge since 2022, but a solid hammer ratio and strong sell-through rate point to underlying health.

|

|

|

The London market continued its four-year slide in sales this year, but the real story is a fair bit more complicated. A number of secular forces have reduced the volume of sales, including the decline of European spending power in the art market and the reduction of London’s importance as the market power shifts toward Paris. And then there’s London’s real problem: the loss of high-value lots. But if you dig through the horse manure of bad numbers, I promise there’s a pony in there somewhere.

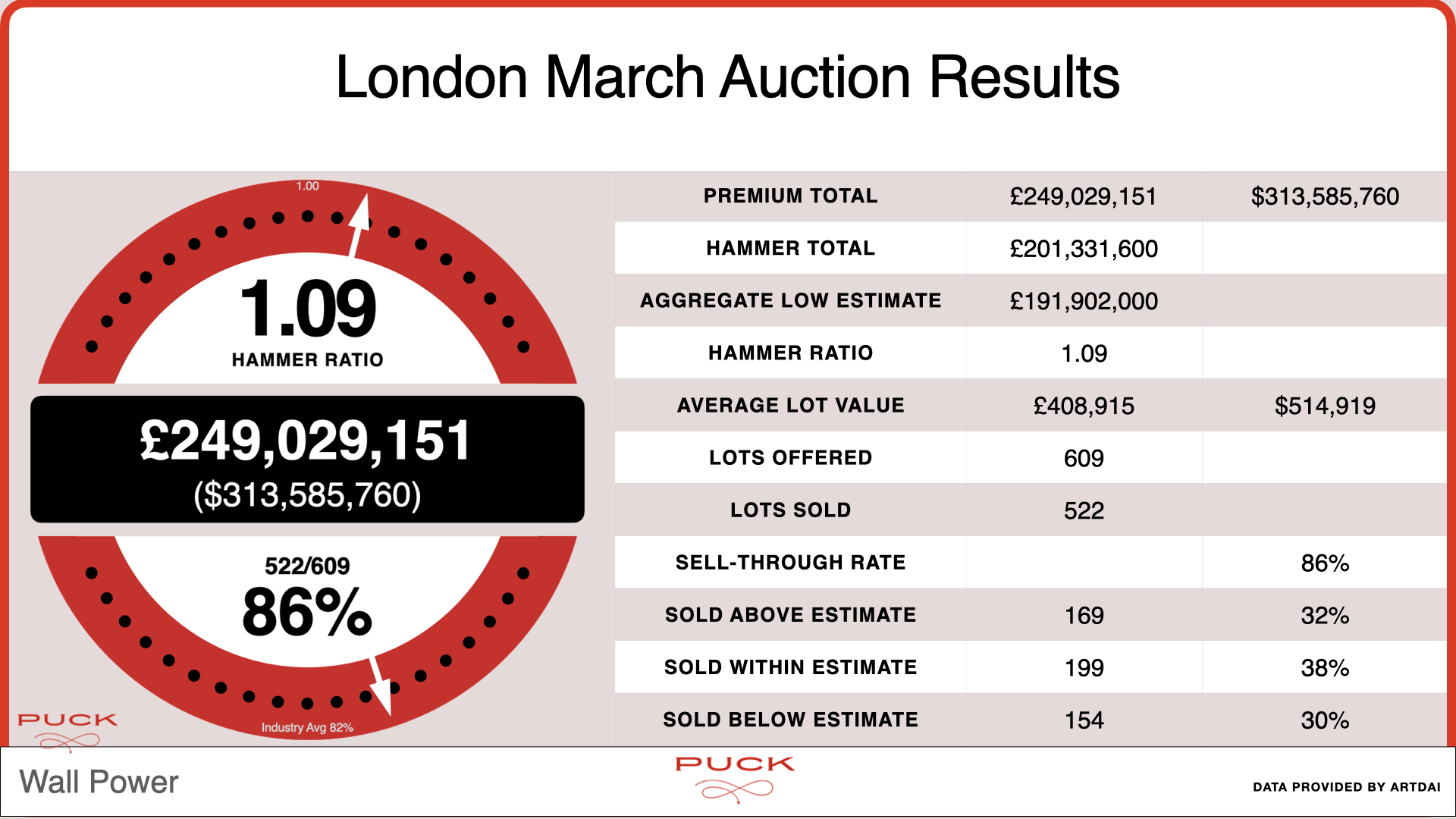

Let’s get the bad news out of the way. The top lots this year were nowhere near as valuable as in previous seasons, which goes a long way toward explaining some of the grim statistics that follow. Since the London sales’ most recent peak of $718 million in 2022, ARTDAI’s data shows a contraction of 56 percent overall, to $313 million (or £249 million) as of last week. It’s been a series of steps downward: The market declined 30 percent between 2022 and 2023; 8 percent from 2023 to 2024; and then another 32 percent from 2024 to this year. Meanwhile, the average price per lot in London has also been steadily falling: by 23 percent from 2022 to 2023; by 17 percent from 2023 to 2024; and again by 16 percent this past year. I have a feeling that average lot value may be the key metric in tracking the health of this market.

There’s an important proviso, however. As recently as 2023, the London sales were evenly split between Christie’s and Sotheby’s, with Phillips having a much smaller market share. In 2024 and 2025, Sotheby’s sales totals lagged behind Christie’s substantially, shifting market share while also reducing overall totals. Is last year’s drop an overall market problem or a Sotheby’s problem, given the auction house’s double whammy of changing their fee structure and staff reductions? It’s impossible to know.

Whatever the case, the auction houses did their best. The aggregate low estimate— i.e., the value of all property gathered for the sales—dropped by 30 percent from 2022 to 2023. That’s pretty close to the decline in overall results after the hammer dropped. But in 2024, the auction houses brought an estimated value to market that was 8 percent greater year over year. The initial optimism was misplaced, however: The sales total was actually lower than the previous year’s. Clearly, the specialists learned their lesson for this year, when the estimated value was down 36 percent from 2024, but the sales total only fell by 32 percent. That should be a good signal.

Another promising sign: The overall hammer ratio for these sales was 1.21 in 2022 and 1.19 in 2023 before falling to 1.01 in 2024. This season, the hammer ratio ticked up to a solid 1.09. One way to interpret these numbers: The London market hit bottom, found its footing, and is beginning to make progress. So while London’s sales did fall substantially this season from the previous year, the market actually seems to be in far better shape than it was—especially since the hammer ratio numbers have been better than what I’ve seen in other market centers. The London sales have generally been well managed, maybe even better managed than the rest of the market through this long contraction, even accounting for the secular forces mentioned above.

|

|

Now, some moderately good news: London’s sell-through rate was a healthy 86 percent this past week, with 522 lots sold out of a total of 609 offered. Moreover, only 30 percent of the lots sold at compromise prices (i.e., below what the consignors hoped to achieve)—still a bit high to say there’s solid market momentum, but not a bad number. The remainder of the lots achieved prices that were fairly evenly distributed above and within the estimates: A full 38 percent of the lots sold for prices that met expectations, and another 32 percent saw competitive bidding.

|

|

The real issue—the loss of high-value lots—shows up in the statistics for the top 10 lots by price. This season’s most expensive lot was a Magritte, sold for nearly $13 million. But in the previous two years, the top lot was more than three times that value (a $45 million Kandinsky and a $42 million Magritte, respectively; in 2022, it was $79 million for another Magritte). This has an important impact on the overall results, which previous years’ numbers make clear. The top 10 lots were 45 percent of total sales in 2022, 38 percent in 2023, and 37 percent in 2024. This year, the top 10 only accounted for 25 percent of sales.

Still, the bidding was strong for the top lots this year. Only one, the Francis Bacon, failed to get bids to the estimate level. Four of the top 10 were bid above the estimate range, and two of those were the subject of real bidding battles, which resulted in hammer ratios above 4.0. Moreover, we can also see in this chart a wide range of artists who worked in very different

styles, in different eras and geographies, with French, Japanese, Irish, Belgian, British, and Italian artists all represented, and a century between the earliest work and the latest. So when we say we want to democratize the art market, with a greater variety of artists collected, lower values might be the end result—or at least a temporary, transitional phase.

|

|

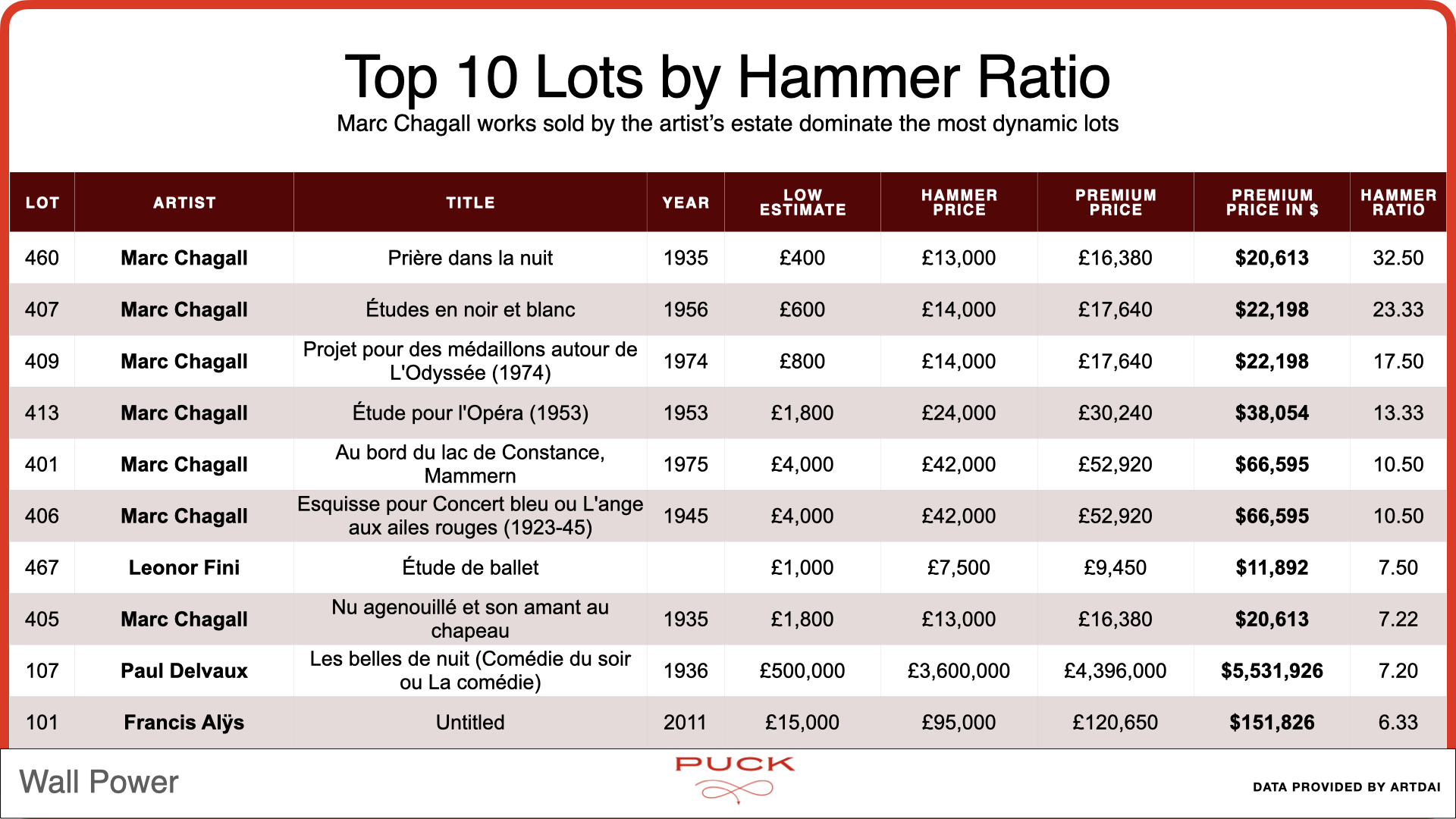

Marc Chagall dominates the list of works with the highest hammer ratios, for the fairly prosaic reason that the estate has been selling through Christie’s for some time. Not all 33 of the Chagall lots in these sales were from the estate, but 21 of them sold for prices above the estimate range. The estate’s ability to offer the works at very attractive estimates is what results in these huge hammer ratios for the low-value works (the top of which was £8,000). There was also a very strong price for a very low-value Leonor Fini.

Elsewhere in eye-popping hammer ratios, three Francis Alÿs paintings sold well, with the two at Sotheby’s hitting hammer ratios six times the estimate. These were from the collection of John Kaldor, the Hungary-born Australian collector, and were estimated at £15,000 each; one sold for £114,000 and the other for £120,000, with fees. I got a text from a private dealer asking what I knew about this, but I confess I’m still not sure what the story is. (If you think you know, please hit reply and let me in on the secret.) Regardless, the results once again underscore that confident consignors willing to accept a low estimate have real upside in this market.

|

|

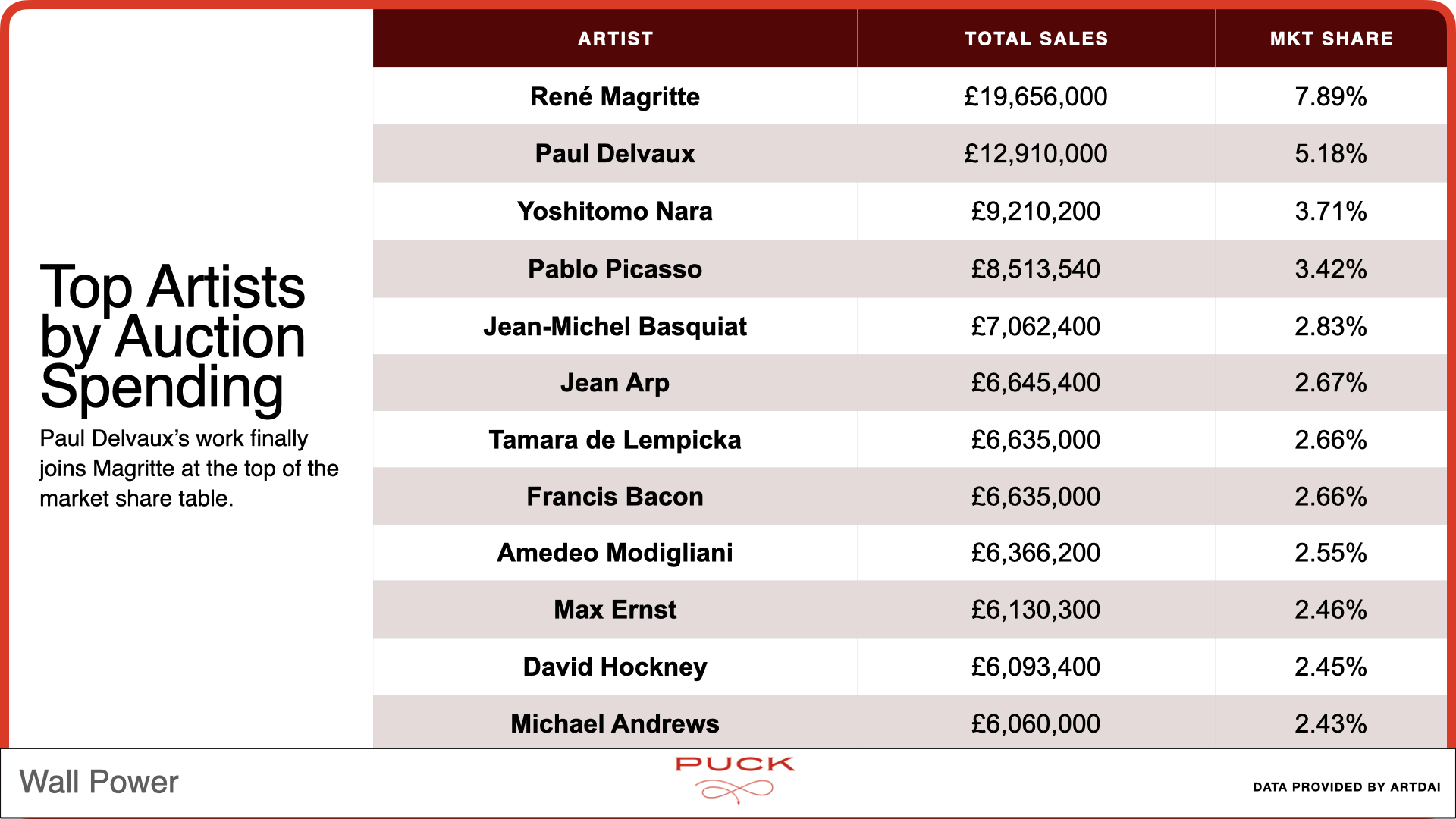

Finally, we can see the effect of the loss of high-value works in the overall market share by artist. This was, in many ways, a big week for Max Ernst, who hit a 2.5 percent share on the strength of five works that all sold within or above estimates, and another work jointly made with Leonora Carrington that sold for more than 3.5 times the estimate. Some of the giants, meanwhile, saw their shares slip—there’s that democratization again. Magritte was again the top seller, with nearly $25 million—but that translated to just below 8 percent market share. Pablo Picasso once dominated these sales, with market share of nearly 25 percent. But the master was down to 3.42 percent after anemic sales last week—a quarter of his 28 works offered failed to find buyers, including one 1964 work estimated at £1.5 million. Nine works sold for prices below the estimate, and only two were bid above the estimates.

While the three Paul Delvaux works were a spectacular success, they only accounted for about 5 percent of the money spent in London. Yoshitomo Nara had three works in these sales, only one of which really generated any spending, but his work got nearly 4 percent market share. Modigliani, Tamara de Lempicka, Bacon, Michael Andrews, and even David Hockney performed in the same manner. The art market needs rotation and the emergence of new artists to chase, to generate excitement. Believe it or not, that’s beginning to happen.

|

The data in these posts is provided by ARTDAI. If you want access to their data for yourself, or your firm, you can learn more about the service here. Puck will receive an affiliate fee from any subscription.

I know these numbers can seem dense. But it’s important to get some reference points on the market after these big sales events. Next week, we’ll be back to our regular programming.

Until then,

M

|

|

|

|

Puck founding partner Matt Belloni takes you inside the business of Hollywood, using exclusive reporting and insight to explain the backstories on everything from Marvel movies to the streaming wars.

|

|

|

|

The ultimate fashion industry bible, offering incisive reportage on all aspects of the business and its biggest players. Anchored by preeminent fashion journalist Lauren Sherman, Line Sheet also features veteran reporter Rachel Strugatz, who delivers unparalleled intel on what’s happening in the beauty industry, and Sarah Shapiro, a longtime retail strategist who writes about e-commerce, brick-and-mortar, D.T.C., and more.

|

|

|

Need help? Review our FAQ page or contact us for assistance. For brand partnerships, email ads@puck.news.

You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with . To stop receiving this newsletter and/or manage all your email preferences, click here.

|

|

Puck is published by Heat Media LLC. 107 Greenwich St, New York, NY 10006

|

|

|

|